$EDEN: An Assymmetric Call Option into RWA Meta

Date: January 11, 2026

Asset: OpenEden ($EDEN)

Sector: Real-World Assets (RWA) / Tokenized Securities

Verdict: Asymmetric Buy / High Conviction Value

1. TL;DR: Executive Summary

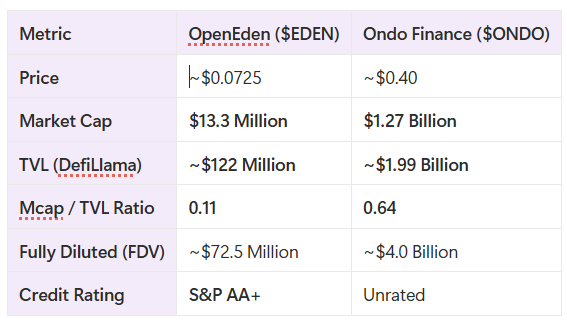

- ◆Extreme Valuation Dislocation: OpenEden currently trades at a Market Cap to Total Value Locked (TVL) ratio of roughly 0.11. In stark contrast, its primary competitor Ondo Finance trades at a premium (>0.64) - a factor of 5-6x relative to its closest peer.

- ◆Strategic & Capital Backing: In December 2025, OpenEden closed a pivotal strategic financing round participated by Ripple and Anchorage Digital. While the exact figure remains undisclosed, the caliber of backers signals a pipeline into the XRP Ledger’s institutional DeFi ecosystem that could materially improve Eden’s distribution.

- ◆The "Governance" Discount: The market has over-indexed on the "governance token with no yield" narrative, irrationally punishing $EDEN while ignoring its new utility roadmap. The token is priced as if the protocol will never activate the value accrual, creating a "deep OTM option" on future revenue for buyers at these levels.

- ◆Superior Institutional Setup: Unlike competitors that often use "Fund of Funds" wrappers (like wrapping an iShares ETF), OpenEden operates a vertically integrated BVI Professional Fund where assets are custodied directly by BNY Mellon. This setup offers superior bankruptcy remoteness and direct ownership, a critical requirement for the next wave of conservative institutional capital.

- ◆2026 RWA Meta: The "flight to quality" is the dominant trend for 2026. As yields compress and regulation tightens, capital will rotate from "gray market" RWA wrappers to rated, compliant infrastructure. OpenEden is the first/only tokenized U.S. Treasury fund with with Moody’s "A" and S&P "AA+" ratings, positioning it to capture this specific capital flight.

2. Introduction: The Asymmetry of Boring

In the world of cryptocurrency, "safety" is rarely priced correctly until it is the only thing that matters. OpenEden ($EDEN) represents the epitome of this inefficiency. As of January 2026, OpenEden has established itself as the "adult in the room" for tokenized Real-World Assets (RWAs), offering on-chain U.S. Treasury Bills (TBILL) and a yield-bearing stablecoin (USDO) custodied by BNY Mellon, one of the oldest U.S. banks and the world’s largest custodian bank.

Yet, the market treats $EDEN like a dead asset. Trading at approximately $0.07 with a circulating market cap of just $13.3 million, the token has seemingly been left behind despite the hype around the RWA meta. However, a look under the hood reveals a protocol managing nearly ~$122 million in assets (+70Mn in stablecoin), backed by the largest custodian in the world, and integrated with giants like Binance and Ripple.

The Thesis:We believe $EDEN is severely undervalued. The market is pricing it for obsolescence, failing to recognize that the 2026 RWA "Meta" is shifting from access (who can get me T-Bills?) to solvency (who can I trust with $100M?). OpenEden’s conservative, rated infrastructure makes it the superior choice for the institutional inflows that characterize this cycle.

3. Deep Dive A: The 2026 RWA Industry Narrative

To understand the bull case, one must accept that the "Wild West" era of RWAs is over. In 2024, any protocol that wrapped a T-Bill could attract capital. In 2026, the differentiator is trust architecture. The "RWA Supercycle" is no longer a prediction; it is an operational reality. The Total Value Locked (TVL) in RWA protocols has surpassed $17 billion (DefiLlama), flipping decentralized exchanges (DEXs) in importance. This shift is driven by a singular force: Institutional Mandates.

Hedge funds, corporate treasuries, and family offices are moving on-chain, but they are legally barred from holding unrated, self-custodied tokens. They require:

- ◆Bankruptcy Remoteness: Assurance that if the crypto issuer (OpenEden) dissolves, their assets are safe.

- ◆ISINs and Credit Ratings: Standardized identifiers and third-party risk assessments.

OpenEden anticipated this shift years ago. While competitors focused on retail marketing, OpenEden spent 2025 securing Moody’s "A" and S&P Global "AA+" ratings. This effectively "whitelists" their TBILL product for institutional allocators who cannot touch unrated competitors.

The market has not yet priced in this exclusivity; it is pricing $EDEN as a retail DeFi coin, not an institutional rail.

4. Deep Dive B: The "Ferrari Engine" Setup (Custody Moat)

When analyzing RWA protocols, the legal wrapper is the product. This is where OpenEden’s setup proves superior to the market leader, Ondo Finance.

The Competitor's Model (Ondo Finance): Ondo’s flagship OUSG product primarily utilizes a "Fund of Funds" model. It wraps the BlackRock BUIDL fund or ETFs like SHV. While efficient, this introduces a double-layer of fees and counterparty risk. You are trusting Ondo’s SPV, which in turn holds BlackRock’s token/ETF, which looks like a derivative of a derivative.

The OpenEden Model (Vertical Integration): OpenEden does not wrap an ETF. Its TBILL token represents a direct share in a BVI Professional Fund. Crucially, the underlying assets (U.S. Treasury Bills) are custodied directly by BNY Mellon.

- ◆Why this matters: BNY Mellon is a Global Systemically Important Bank (G-SIB) with $57 trillion under custody. By partnering directly, OpenEden removes the "crypto middleman" risk.

- ◆The Benefit: For a TradFi CFO, this structure is recognizable. It mirrors a standard money market fund. For a Crypto Native, it offers the highest form of "Bankruptcy Remoteness." If OpenEden Labs disappears tomorrow, the BVI fund (run by independent directors) and the assets at BNY Mellon remain intact for token holders.

This "Ferrari Engine" infrastructure is currently being sold for the price of a Honda Civic because retail investors find legal structuring boring. But in the 2026 institutional game,"boring" is what may attracts billions.

5. Deep Dive C: The "Utility" Roadmap

The primary criticism of $EDEN is that it is a "do-nothing" governance token. The new business roadmap for 2026 directly addresses this, positioning the protocol to capture value from the "Meta" of payment networks.

- ◆Cross-Border Payments (The Lightnet Partnership): OpenEden is not just a savings account; it is building a payment rail. By partnering with fintechs like Lightnet in the ASEAN region, OpenEden aims to use USDO (their yield-bearing stablecoin) as a settlement currency. This transforms USDO from a passive collateral asset into a medium of exchange for remittances, generating organic velocity and fees that act as a distinct value stream from simple T-Bill yields.

- ◆The "High-Yield" Pivot (Tokenized Bond Funds): As interest rates stabilize, T-Bill yields (risk-free rates) become less attractive compared to corporate debt. OpenEden is launching a Tokenized Bond Fund in 2026 focusing on high-yield corporate bonds. This diversification will allow them to compete with players like Maple Finance on yield (targeting 6-9%) while retaining their regulated "rated" wrapper.

- ◆Multichain Ubiquity: The December 2025 launch of cUSDO on Solana was a strategic masterstroke. Solana is the home of retail liquidity. By bridging the "institutional safety" of OpenEden’s BNY-backed assets to the "degen speed" of Solana, they are effectively becoming the backend liquidity provider for Solana’s DeFi ecosystem.

6. Deep Dive D: The Valuation Dislocation

This is the quantitative backbone of the thesis. Using data from DefiLlama (January 2026), the valuation gap is mathematically indefensible.

The Underlying Logic: The market is paying $0.64 for every dollar of TVL managed by Ondo. It is paying only $0.11 for every dollar managed by OpenEden.

- ◆Mean Reversion: If OpenEden were to simply reprice half of ONDO multiple of its peers (let's say 0.32 of Ondo’s 0.64), the token price would need to triple (~300% upside) to $0.20.

- ◆The Ondo Parity: If it were to match Ondo’s premium multiple (0.64), implying the market values its BNY custody as equal to Ondo’s brand, the token would trade at $0.42 (~700% upside).

So at a $13M market cap, the market is effectively saying this BNY-custodied, S&P-rated protocol has the same value as a generic memecoin.

7. Key Risks: The Bear Case

To ensure a balanced evaluation, we must identify why the discount exists.

- ◆Value Accrual Uncertainty: $EDEN is currently a governance token. The "Buyback and Burn" mechanism is listed as a "Potential Planned Future Use Case" subject to regulatory approval. If the team remains too conservative to switch on the fee toggle, the token has no DCF (Discounted Cash Flow) value.

- ◆The "TBD Locked" Supply: Tokenomics data reveals a large tranche (~348M tokens) designated as "TBD Locked." While currently frozen, the lack of clarity on how these tokens will be distributed creates a dilution over the price.

- ◆Vesting Overhang: With only ~18% of the supply circulating, early investors (VCs) are still in their vesting periods. Regular unlocks will create structural sell pressure throughout 2026, requiring substantial demand (buybacks or new investors) to absorb.

8. Conclusion: The Verdict

OpenEden is a classic Deep Value play. It is an unsexy, highly compliant infrastructure project trading at a distressed valuation because it lacks clear retail hype and "ponzi-nomics."

Bullish If:

- ◆TVL Expansion: The Ripple/Solana integrations drive TVL past $300M, making the 0.07 valuation ratio statistically absurd.

- ◆Governance Action: The DAO proposes any form of revenue share or buyback program, instantly validating the token's economic model.

- ◆Ripple Integration: We see RLUSD (Ripple's stablecoin) utilizing OpenEden products for reserves.

Bearish If:

- ◆Stagnation: TVL remains flat at around $120-130M for another quarter, indicating the product has hit a ceiling and faced clear distribution issue.

- ◆Regulatory Paralysis: The team refuses to turn on value accrual due to fear of the SEC, leaving the token as a "pet rock."

Final Thought:

EDEN is a low-float, high-dilution governance token attached to genuinely institutional-grade RWA rails, priced at a deep discount to ONDO, its closest competitor. Though the discount is partially justified until token value accrual + dilution management are demonstrated - this setup provides an “out-of-money call options” like assymmetric bet into the RWA meta.

If you believe that RWA will remain a dominant sector in 2026, $EDEN offers an interesting risk-adjusted entry in the market. You are buying a Ferrari engine (BNY/S&P setup) for the price of a Honda Civic, simply because the market hasn't recognized the importance of it yet.

Notes & Disclaimer: This article is for informational purposes only and does not constitute financial advice. Cryptocurrency investments, especially in small-cap assets like $EDEN, carry high risk.

No disrespect to Honda Civic - still my favorite grab/uber choice of car, since I know the driver will be an old uncle that may not be able to read Google Map, but knows his way inside-out.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.