Is Lighter going to be $LIT?

This report reflects my own views and not necessarily the views of Kronos Ventures or WOO. The following analysis reflects my personal conviction and is provided solely for educational context, it should not be construed as financial advice. I am writing this of my own volition, and it is important to state that I have received no compensation, incentives, or advisory fees from the Lighter team or any affiliated parties. While I earned a small points allocation approximately ten months ago, my current exposure is driven by my own capital. As of December 16, 2025, I am long on both Lighter and Extended points.

Over the last two weeks, I have concentrated on strategic secondary accumulation, primarily acquiring whole wallets through private OTC deals. By leveraging established relationships within my network, I’ve been able to facilitate these transfers on a reputation-based, non-collateralized basis. This approach has allowed me to secure a cost basis that currently sits at a 20% discount to prevailing market speculation.

This thesis serves as a breakdown of my internal investment framework as it applies to Lighter’s fundamental value proposition. My focus here is on the underlying mechanics of the platform and the specific demand sinks for the

token that I believe the broader market is currently mispricing. While certain proprietary details remain shielded from the public, my outlook is informed by a combination of on-chain forensics and high-level discussions with participants deep within the project. In the following sections, I will outline the structural catalysts that support my bullish stance, alongside the specific risk thresholds that would trigger a total divestment of my holdings. Special thank you to Derteil, who helped me with some resources and Mitchell who suggested that I should publish one of my reports.

*all sources are highlighted in the end

My Liquid Token Investment Framework

My framework is a product of two worlds: an institutional foundation at WOO and Kronos Ventures, and the "on-chain opportunism" that defined my transition from a career in construction to crypto full-time. I prioritize selective execution over chasing, moving capital only when a project’s structural advantage is fundamentally mispriced.

1. Market Regime & Macro Overlay

I am a liquidity "maxi." First step is defining in what mode the market is:

- ◆Risk-Off: I hunt for "alpha" in rare outliers. I stick to high-conviction scalps with tight invalidations and asymmetric upside.

- ◆Risk-On: I pivot to pure momentum. I am comfortable trading assets with zero fundamental value if the framework permits; in mania, capturing velocity is the only path to outsized returns.

2. Narrative Velocity & Sentiment

On-chain performance is driven by the "Next Meta." I view storytelling not as fluff, but as a marketing engine designed to drive valuation. I never marry a bag. If a token shows relative weakness during its own meta, holding it is a "midcurve" move. I prioritize strength and velocity above all else. The Filter: Is this the next meta, or a candidate for an existing one? Once identified, the game shifts to storytelling and momentum.

3. The Trinity: Idea, Execution, and Product

Crypto is a graveyard of "solutions looking for problems." To filter the noise, I apply venture-level rigor to liquid positions. I move beyond pitch decks to conduct granular background verification. The founder is the ultimate variable; they must be capable of navigating the pivot when the initial plan meets reality. UX/GTM Synergy: A product must be intuitive. Comparing the seamlessness of Hyperliquid to the archaic nature of traditional platforms highlights where the real value lies.

4. Tokenomics & Supply Dynamics

Most assets fail to capture genuine value. In the absence of real yield, I measure Speculative Premiums. I avoid highly inflationary assets and monitor granular unlock schedules. Holding a token which goes through unlocks is a suisade.

5. The Chart: The Final Filter

The chart is the ultimate aggregator of information. If the data provides the "why," the price action provides the "when." It reflects shifts in sentiment and fundamentals before they hit the headlines. As Jesse Livermore said: "The tape never lies."

Market Regime: Selective Conviction in a Risk-Off Environment

The prevailing sentiment is currently one of caution, with many market participants convinced we have already entered a structural bear market. I remain unconvinced. I am a macro and liquidity "maxi", my framework is built on the flow of global capital rather than a 4-year cycle, which I consider "astrology for men". I believe global liquidity trends suggest 2026 could provide a significantly stronger tailwind than the consensus currently anticipates. Most of the money is being made close to the top.

However, a constructive liquidity environment does not guarantee a crypto moon-mission. We have to be honest about the structural break we are seeing: even if 2026 is a "good" year for global markets, crypto could easily continue to underperform traditional risk assets. The industry has lost much of its "sexy" premium, and the risk-adjusted returns compared to equities, robotics, or AI-driven tech have compressed. The era of the "universal alt season" is over; liquidity is too fragmented to lift every project in the space.

Consequently, we are in a risk-off regime where the market is no longer "hot." In this environment, I am being extremely selective. If there is no risk premium to be found in the "beta" of the market, I must find it in the "alpha" of specific assets. I am not chasing noise; I am looking for the rare outliers that can deliver results regardless of the broader market's sluggishness.

Team and Execution: The Paradox of Institutional Pedigree

While I am generally skeptical of the "Harvard Halo", as elite credentials often come with inflated valuations and even larger egos. The underlying metrics here are impossible to ignore. In an industry plagued by anonymous teams and short-termism, I look for "institutional-grade" leadership. The founder of Lighter offers a rare intersection of High-Frequency Trading (HFT) expertise and hyper-scale engineering leadership, providing an execution certainty that is nearly unmatched in the decentralized space.

I. Technical Foundation and Speed of Execution

The protocol’s foundation is built on raw technical talent that prioritizes speed. Graduating from Harvard with a B.A. in Economics at age 18, completing a four-year degree in just five semesters, is a significant signal of a high "rate of learning". When combined with a 9th-place global finish at the ACM ICPC World Finals and a Top 15 national ranking in the Putnam Mathematical Competition, it becomes clear that the team possesses the mathematical depth required to solve the complex hurdles of decentralized derivatives.

II. High-Frequency Trading as a Structural Prerequisite

Perpetual DEXs live and die by their liquidation engines and order-book efficiency. Having led HFT teams at Graham Capital and served at Citadel, the founder understands market dynamics at a granular level. Applying "Citadel-tier" logic is crucial for protocol solvency, HFT experience allows for the design of intelligent liquidation oracles that protect against bad debt during extreme volatility. By understanding low-latency connections and co-location, the team can build matching engines that compete directly with centralized exchanges, naturally compressing spreads and enhancing market efficiency.

III. Scaling Architecture for $200B+

Technical brilliance is a liability if a system "chokes" during market surges. As VP of Engineering at Addepar, the founder managed the re-architecture of backends to be 5-10x faster while overseeing assets surpassing $200 Billion. This experience in building fault-tolerant architectures is vital for long-term resilience. Coupled with his tenure as Head of Machine Learning at Quora, where he drove a 10x increase in core metrics, he has proven an ability to scale user-centric systems effectively.

The Counter-Argument: Network, Ego, and Attention Games

The "Harvard" label often leads to overpricing, and I remain cautious of assuming a "great network" justifies a premium. However, the evidence suggests a genuine institutional reach, reflected in the ability to secure partnerships with the likes of Robinhood, Coinbase, and Dragonfly.

Regarding the "ego" factor: while his persona on Crypto Twitter can be polarizing, my conviction is tempered by direct feedback from trusted sources who vouch for his character behind the scenes. I am not a fan of the "dogfight" marketing style, but in a market where attention is the only real currency, it is a pragmatic, albeit harsh, reality. Most importantly, the founder has demonstrated the ability to take accountability, showing his true colors by owning mistakes during the 10/10 event. The primary risk remains the post-TGE ego; how a founder handles a successful launch is often the ultimate test of long-term protocol health.

Rest of the team

The technical caliber of Lighter is not merely concentrated at the executive level. Out of the 28 engineers currently building the protocol, 23 are winners of international mathematics or physics Olympiads. This level of talent density is rare even by Silicon Valley standards.

Furthermore, there is a distinct "Founder Factory" pattern emerging from Vlad’s previous leadership roles. A significant number of founders leading current Unicorn and Decacorn companies are former employees who operated under his management. I must state that I wasn’t able to confirm this news with full certainty, but to the best of my knowledge it’s true.

I would also like to highlight that the go-to-market strategy of Lighter’s team is extremely impressive.

Narrative Velocity: The Perp DEX Wars

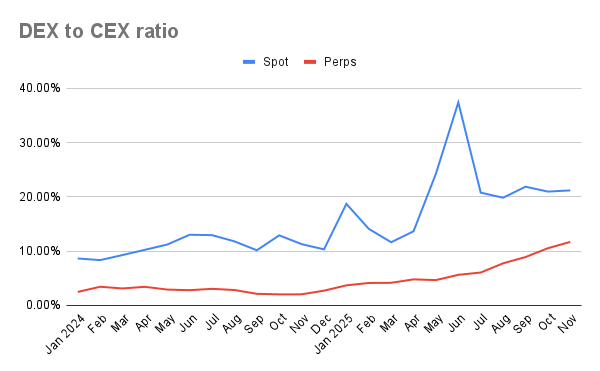

The Perp DEX meta has entered a phase of aggressive evolution. Following the explosive performance of $HYPE, the market is currently in a "copycat" cycle where everyone is attempting to replicate the Hyperliquid playbook. The thesis is simple: CEX trading volume is a massive, trillion-dollar pie, and decentralized alternatives are finally becoming performant enough to eat it. Between the lack of KYC, custody security, and the ability to move capital seamlessly across on-chain assets, the structural advantages are undeniable. I expect the DEX-to-CEX volume ratio to continue its upward trajectory as the primary trend of 2025.

according to coingecko research the perp DEX to CEX ratio is ~12%

While many credit Hyperliquid with creating this meta, my take is that dYdX built the foundation. Credit where it’s due: dYdX was the initial spark that proved the leverage trading could work on-chain; $HYPEsimply provided the fuel for the mania. We then saw the "CZ effect", a prime example of how even in a sideways market, the industry is starved for runners and capital will rotate aggressively into whichever narrative feels "sexy."

This brings us to Lighter. While a wave of Perp DEXs has launched across every chain with bloated, "nuts" valuations, Lighter was early to the table. They’ve built a high-performance product with a top-tier GTM strategy that is now arriving just as the initial meta was beginning to feel stale.

I view the recent "CZ effect" as a strategic necessity; he essentially gave the meta a second leg because he simply cannot afford to cede market share to Hyperliquid. That competitive tension creates an opening. A successful TGE and strong secondary performance for $LIT could act as the third leg for this entire sector. If $LITruns, we’ll see a massive extension in beta plays as capital rotates down the risk curve.

However, we must be realistic. If the TGE flops, the meta likely dies here. CT is already starting to feel like a ghost town, and the market is desperate for a new runner to prove there is still life in the industry. Study $PEPE: in a world of fragmented liquidity and compressed risk premiums, attention is the only real currency.

Competition, valuations and math

Competition:

A few ratios that will be needed:

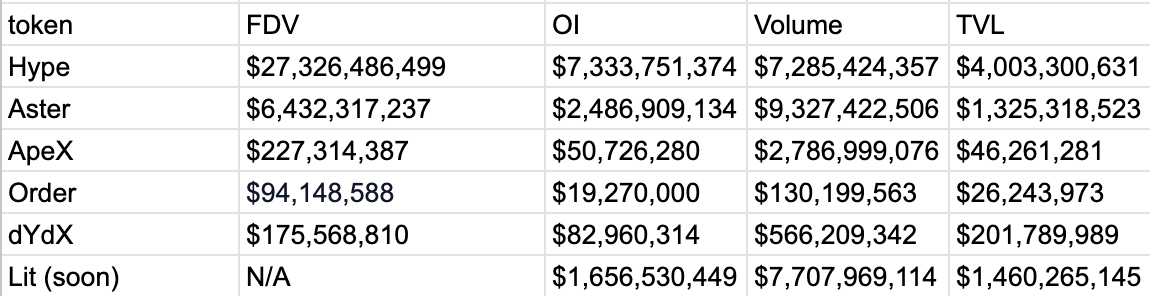

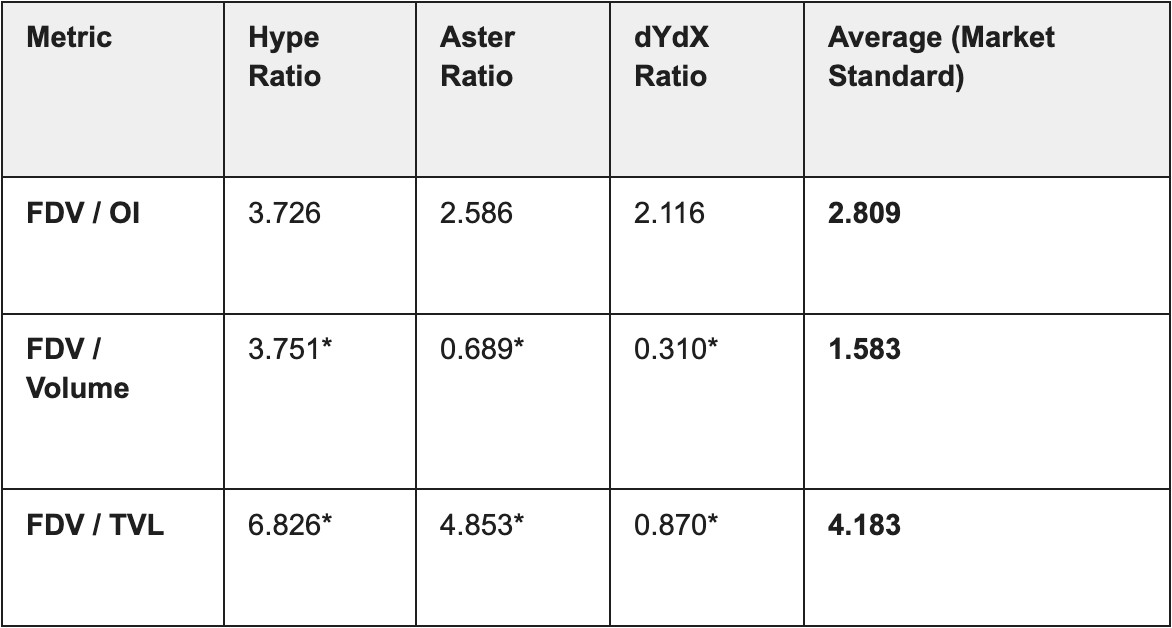

To evaluate Lighter ($LIT) professionally, I created a "Market-Multiple" model. In the world of Perp DEXs, valuation isn't just about how much money is locked (TVL), but how "hard" that capital is working (Capital Efficiency). Many perp DEXs are full of wash trading that’s why I decided to use only Hyperliquid, Aster and dYdX.

Post-TGE Adjusted Valuation

To find a realistic valuation, we must apply a "post-TGE haircut." It is standard for protocols to see a dip in activity once the initial airdrop/incentive period ends. Even with a conservative 30% reduction in Open Interest (OI) and Volume, Lighter remains a formidable player in the Perp DEX landscape. On 18th December (moments before publishing), I decided to add a version (without a haircut), because there are chances that the points program is over.

Formula for the FDV

I’ve decided not to use other metrics since the more I try to make it accurate the bigger the mess becomes. Following results:

Fair FDV (Haircutted) = $5.36 Billion

Fair FDV = $7.64 Billion

The Product Architecture

Lighter has discarded the conventional fee-first approach in favor of a zero-fee model that aggressively captures market share. This strategy drove daily volumes to an average of $3 billion by mid-September 2025 and has recently propelled the protocol past the $7 billion mark, an impressive feat for a platform that not far away was just in invite only mode.

The backbone of this trading activity is the Lighter Liquidity Pool (LLP), a decentralized, community-driven market-making vault that provides the necessary depth for Lighter’s order book. Since early 2025, the LLP has delivered an average 60% APY, successfully merging high-yield incentives with robust liquidity provision.

Dual-Tier Infrastructure: Performance vs. Cost

Lighter’s technical edge is most apparent in its specialized account tiers, which allow users to choose their optimal balance between execution speed and transaction expense:

- ◆Standard Account (Default): This tier is built for retail and latency-insensitive participants, offering a pure 0% maker and taker fee environment. While this removes immediate cost barriers, it introduces a deliberate 200–300ms taker latency.

- ◆Premium Account (Opt-in): Tailored for institutional flow and High-Frequency Trading (HFT), this tier prioritizes absolute speed. It features 0ms maker/cancel latency and a reduced 150ms taker latency. To maintain this "speed moat," users opt into a nominal fee structure of 0.002% for Makers and 0.02% for Takers, alongside access to specialized volume quota programs.

The Market Reality: Strategic Trade-offs

Public sentiment on the zero-fee system is polarized. Many retail users value the lack of upfront costs, while some advanced traders argue that the higher latency on Standard accounts makes them "more expensive" due to slippage during volatile periods. For a retail trader, a 300ms delay can lead to adverse execution, effectively costing 6–12 basis points per trade.

My perspective is that this tiered solution is a significant advancement in product design. Most retail traders prioritize fee-free entries, while those who truly require institutional-grade execution have a clear, simple path to eliminate latency by switching to a Premium account. It is a pragmatic framework that caters to both the "attention-driven" retail base and the "performance-driven" professional market.

The Spot Meta: The Trojan Horse for Retail Onboarding

While perpetuals drive the "whale" volume, Spot Markets are the real battlefield for retail dominance. The shift we’re seeing, pioneered by Hyperliquid’s collaboration with Unit, has proven that an on-chain spot order book is the final nail in the coffin for Centralized Exchanges. For a decentralized ecosystem, spot trading isn't just a feature; it's a statement of sovereign custody. As we’ve seen with the MEXC withdrawal issues, the ability to trade with CEX-level speed without surrendering your keys is no longer a luxury. I am not worried much about ‘Jelly Jelly’ situations. Such attacks happen on CEXes too. We just don’t know about them.

Lighter’s Spot Strategy: More Than Just a "Ding"

Lighter has officially entered the arena with the launch of its ETH spot market, signaling its transition from a niche derivatives venue to a full-spectrum financial hub. The vision here is simple: eliminate the friction of multiple platforms. By integrating spot directly into its zk-rollup architecture, Lighter allows users to manage their foundational assets and their high-leverage perps in a single, unified environment.

The "Email login and trade" UX is the ultimate Trojan Horse. If Lighter can combine the simplicity of a Web2 interface with the security of a zk-L2, it effectively removes every remaining reason to keep capital on a CEX. The accessibility will be there (no KYC makes onboarding much easier).

The Points Disconnect: Organic Growth vs. Farming Noise

There has been mixed sentiment regarding Lighter's spot rewards. While market expectations fueled by the Hyperliquid model anticipated immediate point accrual for spot volume, the reality has been different. For the first week, ETH spot activity didn't move the needle on the leaderboard. Although the team was suggesting that the distribution of points would look similar to the HL model.

My take on this is a bit more nuanced than the "lack of points" frustration:

- ◆Bot Mitigation: By delaying rewards, the team likely prioritized organic users over wash-trading bots that typically swarm zero-fee spot launches.

- ◆Collateral Roadmap: The real value of spot on Lighter isn't just the trade; it’s the upcoming Cross-Margin integration. The team has signaled that spot assets will eventually be usable as collateral for perps, allowing you to hold ETH while margining a BTC position all within one zk-account.

Speculation: The Memecoin and TGE Timeline

There was significant chatter about a potential team-led memecoin to bootstrap spot liquidity (similar to $PURR), but that idea appears to have been sidelined. From an investment perspective, this makes sense. With a $1.5 billion valuation (last round) and a TGE looming, launching a "distraction" token could dilute the primary narrative.

Thesis Note: Spot markets are the bridge to the next 10 million users. While the "hardcore" traders care about taker latency, the average retail user just wants to buy ETH without worrying about MEXC freezing their account. Lighter’s spot market is the play for that "Retail Resurgence."

The Final Frontier: Tokenized Equities

The most significant catalyst for Lighter isn't just about decentralizing what already exists,it’s about pioneering what doesn’t. Vlad has signaled that he is in active discussions with Robinhood to launch tokenized stocks, a move I believe is the next major innovation in DeFi. Hyperliquid is a clear leader in this niche building ultimate financial hub with Unit, Felix and Redstone. Worth mentioning, the main oracle behind this infrastructure and clear leader. Lighter is trying to take a different approach.

The Strategic Pipeline: Lighter as the Proving Ground

This is where the "Institutional Pedigree" meets the product roadmap. Robinhood has already begun rolling out tokenized versions of over 200 US-listed equities (like Apple and Nvidia) and private company shares (OpenAI, SpaceX) to its European users via a custom zk-powered Layer 2. To the best of my knowledge, and though I cannot confirm the exact technical integration with full certainty, Lighter is positioned as the high-performance execution layer for this shift. The main risks for users to trade stocks in DeFi are:

-liquidity and its manipulation (oracle problem)

-security (what happens to stocks if platform goes south)

This is just my speculation, but Robinhood is a regulated platform within TradFi. If Vlad cuts a deal with them, then even a better UX on HL won’t matter. One of the main reasons why people would like to buy stocks in DeFi is tax. Not every system is like the US one, in many countries there’s a simple in and out system. It matters how much fiat you put in and out. It does not matter that you sold crypto to stablecoin. It’s recognised as crypto. Instant premia is the whole tax amount. The risk? What happens if a protocol collapses..

If Lighter becomes the venue where these tokenized assets are traded, leveraging its 0ms maker latency and zk-solvency, it moves from being a "Perp DEX" to becoming the primary infrastructure for Real World Assets (RWAs). Imagine a world where you can hold tokenized Tesla stock and use it as a cross-margin for your BTC perpetuals, all while benefiting from Robinhood's massive retail distribution and all of these risk free of losing your stocks.

By expanding from perps into spot, and eventually into tokenized equities, Lighter is targeting an addressable market worth tens of trillions of dollars, rather than just the low-single-digit trillions of the current crypto space.

Risks

Lighter’s path to dominance is not without significant structural hurdles that warrant caution. Operationally, the protocol has struggled with multiple outages, most notably failing to handle the extreme volatility of October 10th effectively. This raises questions about system resilience that extend to the liquidity layer; the Lighter Liquidity Pool (LLP) remains largely unproven compared to battle-tested models like HLP or Jelly, leaving it unclear how the vault would respond under a coordinated malicious attack. Finally, there is a looming transparency risk regarding the cap table; the split of value accrual between equity holders and token stakers is still unknown, and any model that doesn't prioritize 100% value flow to the token (similar to Hyperliquid) could represent a major structural headwind for $LITholders.

The Final Math: Valuing Points and the TGE Scenarios

The final component of this thesis is the conversion of "abstract points" into a concrete dollar value. Based on the current leaderboard, there are approximately 12 million points in circulation and one point is being traded at a price of $90-$100. By modeling the TGE across several supply and valuation scenarios, we can estimate the market’s current expectations for $LIT.

1. The Airdrop Allocation Scenarios

The team has publicly signaled an airdrop will be 25-30% of total supply. To ensure a margin of safety, I have modeled a "Low" (20%) and "High" (35%) scenario to account for potential tokenomic pivots.

2. Point Valuation Matrix (12M Total Points)

Using a baseline $1.5 Billion FDV from the latest funding round as our floor, and a high of $6 Billion FDV we can derive the following values per point.

Market anticipates $4 billion FDV at the TGE

Summary: The Play

The central risk for Lighter ($LIT) and the primary concern for any serious investor is the "Capital Cliff." We must follow how much Open Interest (OI), Volume, and TVL will remain once the points program ends.

My investment thesis addresses this by applying a cynical 30% haircut to current metrics, effectively "un-farming" the data to find the organic protocol floor. Even after this reduction, the math reveals a significant opportunity: the points are currently undervalued by roughly 30% relative to Lighter's peer-group valuation.

My Final Take

The current OTC price of $90–$100 per point is effectively pricing in a $4B FDV for $LIT. My average entry is at $80, and I aim to buy more at TGE during the inevitable volatility caused by airdrop farmers dumping if price is below $4 FDV and the platform remains the key metric. With the Coinbase roadmap and Robinhood it looks promising. Market consensus undervalues Lighter by at least 30%.

Trading Strategy: Execution

To navigate the transition from points to a liquid market, I am adhering to a strict valuation-based entry and exit plan:

- ◆Entry: I am bidding below $4b FDV on the liquid market or via OTC points. My current average entry is $80. I will bid heavily on any dips below $2.5b FDV, specifically targeting the volatility caused by airdrop farmers dumping at TGE.

- ◆Exit: I will begin DCA sells once market euphoria is evident or the valuation climbs above $8/9b FDV.

Summary Risk Note: My main concern remains the retention of OI, Volume, and TVL once the points program ends. I will be monitoring the post-TGE data closely. This plan assumes no major shifts in market share or "black swan" events. I will adjust my position if anything changes.

Sources:

- ◆https://www.21shares.com/en-ae/research/the-perpetual-dex-wars-hyperliquid-aster-and-lighter-in-focus?utm_source=chatgpt.com

- ◆https://www.coingecko.com/research/publications/dex-to-cex-ratio?utm_source=chatgpt.com

- ◆https://www.perpetualpulse.xyz/

- ◆https://www.linkedin.com/in/vnovakovski/

- ◆https://x.com/derteil00

- ◆https://x.com/ruslan55x/status/2001630944059339258?s=20

- ◆https://x.com/vnovakovski/status/1996591002182705367?s=20

- ◆https://x.com/hosseeb/status/2001317251962831295?s=20

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.