AERO: The MetaDEX Expansion Thesis

Aerodrome will announce new planned changes to the project on November 12. After piecing together public hints, I believe AERO offers an asymmetric long opportunity ahead of what the team will likely try to turn into a dominant DEX across a majority of EVM chains—positioning AERO as an index on the growth of decentralized exchanges.

TLDR – Why AERO offers an asymmetric opportunity

- ◆The Aerodrome-style DEX model is demonstrably more efficient than earlier AMM DEXs like Uniswap—where they appear, they tend to dominate.

- ◆On November 12, 2025, there will be a major announcement; in this thesis I speculate on what it might contain.

- ◆I think the Aerodrome team will want to fully leverage its advantage and expand to additional blockchains, bringing more economic activity to the DEX and more revenue to AERO.

- ◆It’s very likely they will aim to make Aerodrome the dominant DEX across most EVM chains and turn the AERO token into an index for the growth of decentralized exchanges.

- ◆The entire effort will be backed by a company, ****** Labs, which in my view will be financed along the lines of DATcompanies—outside investors comfortable with a DAT that holds AERO long-term, generates income from it, and feeds value back to AERO via new products.

- ◆If I’m right, AERO offers roughly a 2–3× trade here. The main risk is the current lack of information: there isn’t enough to say with certainty this is their plan, and after the announcement we’ll need to reassess whether the thesis remains relevant.

What is Aerodrome?

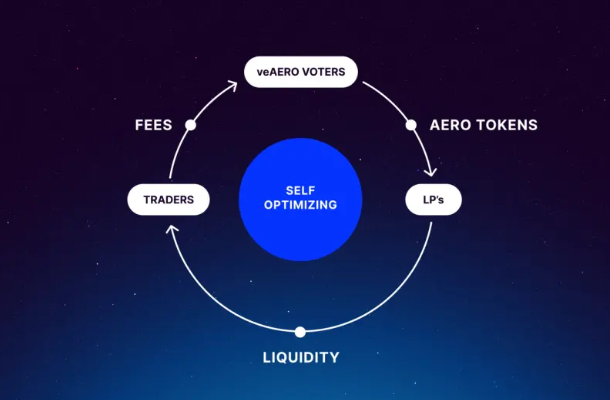

Aerodrome is a DEX that maximizes value distribution toward users—traders, liquidity providers (LPs), and token holders. It currently runs exclusively on the Base chain.

It works as follows:

- ◆LPs are the key. Without liquidity, traders don’t come. Each week Aerodrome mints new AERO tokens and directs them to liquidity providers—not uniformly, but based on votes by veAERO holders.

- ◆veAERO holders decide where inflation goes. Each week a certain amount of AERO is “printed.” veAERO holders vote which pools receive incentives. In return, they receive a proportional share of the fees from the pools they vote for. They thus have an economic incentive to vote as efficiently as possible—where liquidity is needed, rewards are highest.

- ◆Traders - In most cases, traders use aggregators that search for the best price—and that’s typically where the most liquidity is. Thanks to veAERO voting, the deepest liquidity often ends up on Aerodrome, and a large share of Base volume routes through it.

The team refers to this model as aMetaDEX.

Note: Aerodrome is a fork of Velodrome by the same team. While Aerodrome runs on Base, Velodrome is deployed on about a dozen chains within the Optimism Superchain.

Success of the MetaDEX model

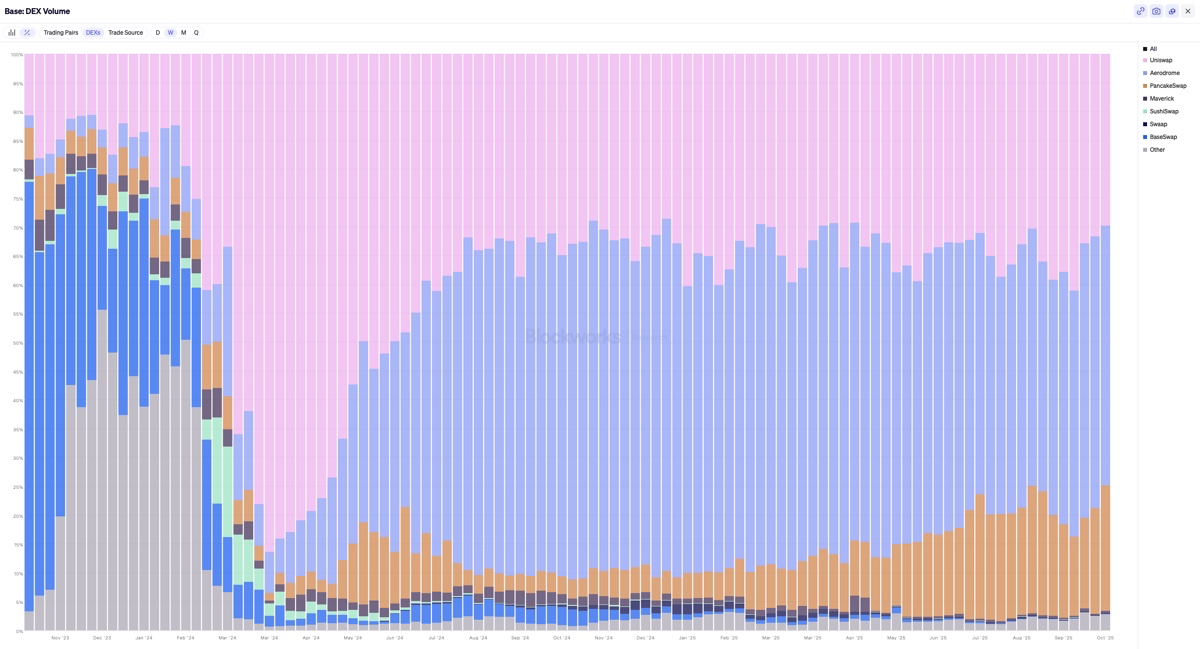

Over the long run, Aerodrome holds roughly 50–60% of volumes on Base in both bull and bear phases. In recent months PancakeSwap has been biting into its market share thanks to the Binance Alpha campaign, which incentivizes on-chain trading via the Binance interface (often new volume, and sometimes even wash trading). Even so, Aerodrome keeps >40% market share.

Source: Blockworks

Aerodrome has therefore succeeded on the largest L2 for Ethereum—even against Uniswap, which has the strongest brand among DEXs. But can this success be generalized?

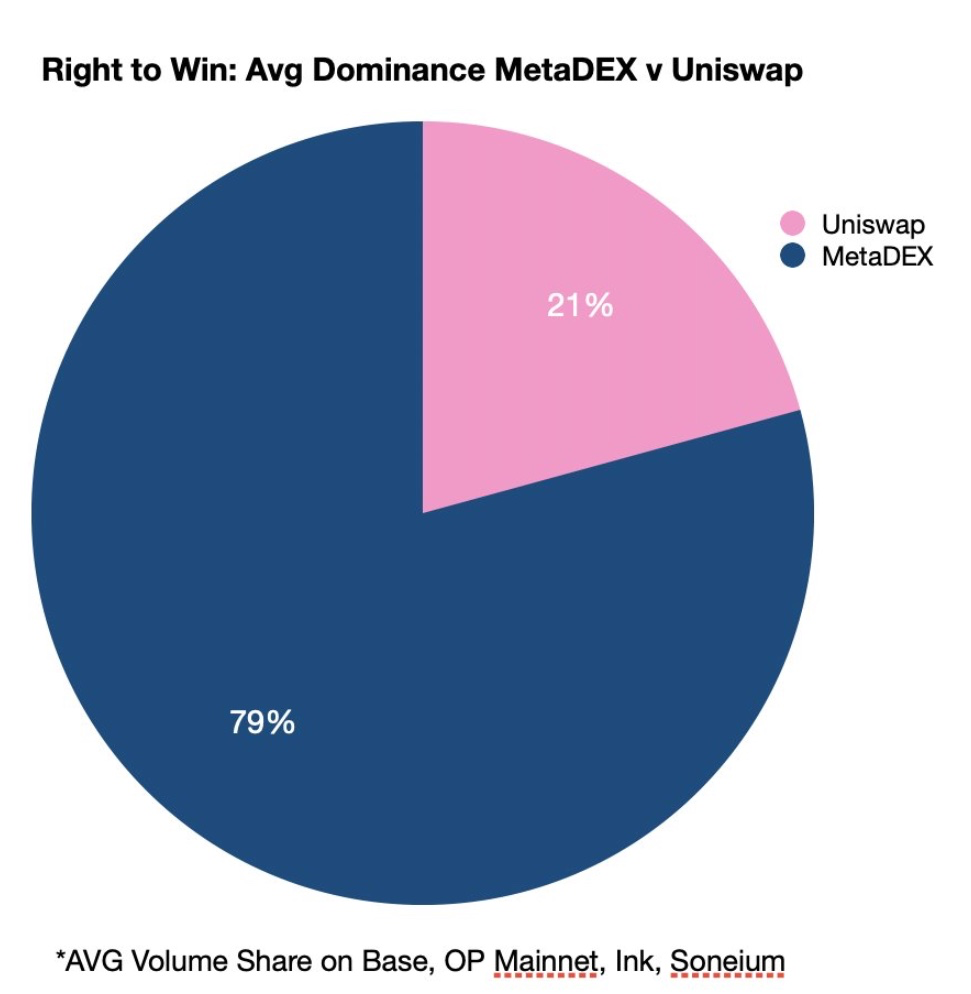

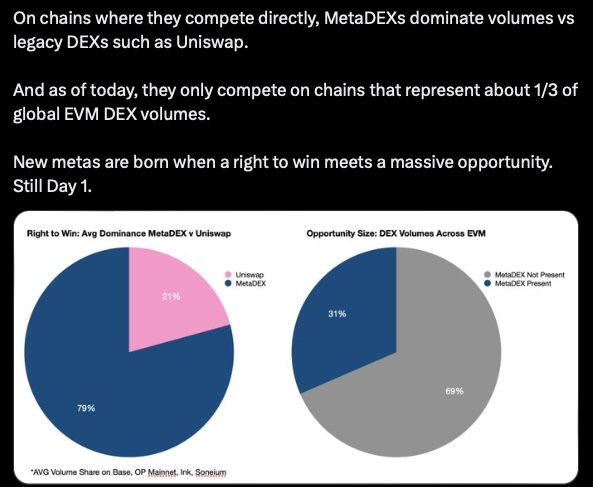

Alexander (co-founder of Aero/Velodrome) shows a comparison of average market share by volume on Base, OP Mainnet, Ink, and Soneium vs Uniswapś volume on these chains.

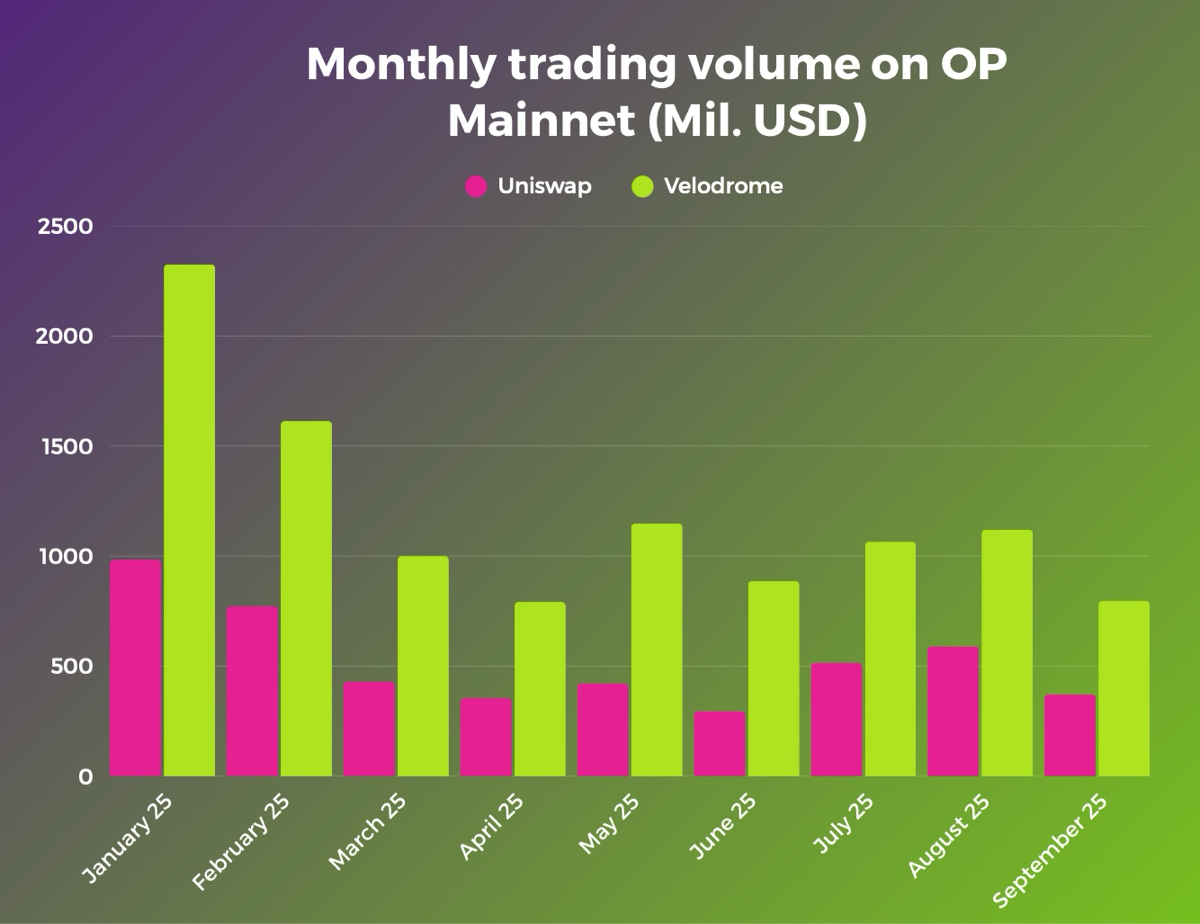

Because Base (with much higher volumes) strongly influences the data, it’s useful to look separately at OP Mainnet—the second-largest market where these two models compete. Based on DeFiLlama monthly volumes since early 2025, Uniswap on OP Mainnet captures <50% of Velodrome’s volumes in every single month.

From these three data sets it follows that the MetaDEX model not only looks good “on paper,” but has been winning long-term against Uniswap and other DEXs on most chains where they operate side by side.

The future of MetaDEXs

The team announced that on November 12, 2025 there will be a major announcement regarding the future of Aerodrome and Velodrome. This thesis therefore doesn’t describe just “what a MetaDEX is,” but “what it could become.” From the available hints (posts and podcasts by Alexander—co-founder of both DEXs and CEO of a new company, see below), I’ll try to piece together what they’re cooking.

My expectation is that the announcement will consist of three important parts:

- ◆Every dollar extracted is a bounty

- ◆AERO = index for decentralized exchanges

- ◆The first ****** Labs that grows the pie

1) Every dollar extracted is a bounty

At ETHcc, Alex said that DeFi has not yet fulfilled the promise of removing middlemen and lowering fees. On the contrary, protocols like Uniswap add fees (front-end, etc.), while LPs get less, and UNI token holders haven’t seen a penny of profits in five years.

The competition therefore extracts value away from LPs and token holders, which Aerodrome/Velodrome view as their competitive advantage—and one of the reasons why MetaDEXs bite into Uniswap’s market share.

If they have identified their edge and Uniswap still dominates on some chains, then the next logical step is expansion—gradually taking share where less competitive players like Uniswap are entrenched. Alex himself mentions that roughly two-thirds of the market by volume still don’t have their MetaDEX and hints this will change.

On Discord, he states plainly that the aim is to surpass Uniswap — and he outlines several paths to get there.

My conclusions from these hints:

- ◆Aerodrome/Velodrome will expand to additional EVM chains.

- ◆The competition extracts too much, weakening its position; the MetaDEX model doesn’t, and therefore wins where it competes.

- ◆The logical move is to go after the largest remaining EVM markets that don’t yet have their MetaDEX.

Candidates:

- ◆Ethereum mainnet – the largest liquidity (2–3× Base), Uniswap >50% share. Cons: higher fees and more conservative LPs (harder to persuade big players to migrate). The weekly rhythm of voting/claims in the MetaDEX model can be costlier on mainnet due to gas.

- ◆Arbitrum + Orbit – roughly one-third the volumes vs. Base, but Uniswap dominates 60–70%; for a MetaDEX that could be an “easier” win. Also, a Robinhood chain is planned on the Arbitrum stack—having a DEX ready would make sense similar to earlier Base land-grab.

My estimate: expansion is almost certain. As a first step, Arbitrum makes more sense to me as mainnet is more complex and expensive—though I trust the team that even if it is mainnet, the move will be well thought out.

How would that scale the project?

If Aerodrome expanded to ETH Mainnet and Arbitrum and became the #2–3 DEX on both, here are the rough numbers (to be discussed later in detail):

- ◆ETH Mainnet – about $110B monthly volumes. At 20% market share, that’s $22B monthly volume for Aerodrome.

- ◆Arbitrum – about $21B monthly volumes → if Aerodrome takes one-third, that’s another $7B added.

With these fairly conservative figures, Aerodrome would more than double its average monthly volumes—and thus fees for veAERO holders (assuming a fee rate similar to Base).

2) AERO = index for EVM chains

The first MetaDEX instance was Velodrome. With the launch of Base, the team forked the code, launched Aerodrome, and airdropped corresponding veAERO positions to everyone who had veVELO (community secured). But because Aerodrome captured the most attractive market, VELO’s price gradually faded.

A world where each expansion means a new token is unsustainable: it fragments demand and liquidity for ve-positions, as well as team/community attention. It therefore makes sense to consolidate Aerodrome and Velodrome into one DEX and one token, with branches across chains.

Alex essentially spelled this out on a recent Seed Club podcast:

“If you want to bet on the growth of lending on EVM, you buy Aave. To bet that CEXs will integrate DEXs, there isn’t a token that would be an index on EVM DEXs with real on-chain utility. That’s the direction we’re looking at.”

Message: Turn AERO (or the merged token) into an index on EVM DEX growth. And by the way—to really be an index, it needs a branch on every major chain, much like Aave—another confirmation that expansion to Mainnet and Arbitrum is needed.

Alex also openly discussed in Discord the possibility of merging VELO and AERO

In practice this would mean: one MetaDEX (multi-deployment on Ethereum mainnet, Base, Arbitrum, Arbitrum Orbit, and within the Optimism Superchain), one token (AERO) incentivizing all integrations, and veAERO holders receiving fees across chains according to where they direct incentives.

Key condition: On new chains, Aerodrome needs to build a dominant (or at least Top-2/3) position in volumes.

With multiple deployments + a solid position + one token, AERO would become an index on EVM DEX growth.

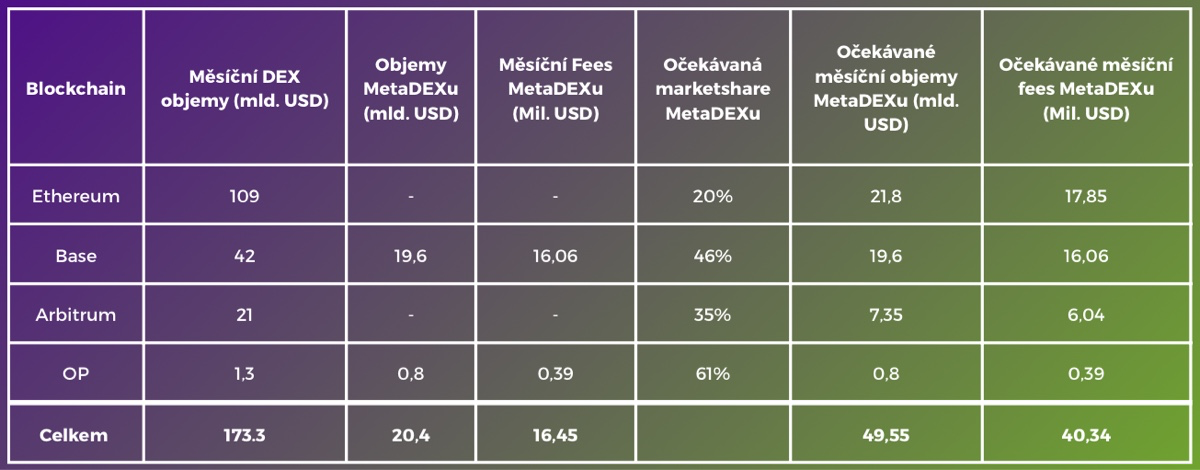

Addressable market

The table (below) compares the current state (total volumes, MetaDEX share, selected fees) with expectations after expansion (target market share on Ethereum/Arbitrum and implied volumes/fees). These are my estimates based on the model’s track record and a discount for the difficulty of entering a new market.

Assuming 35% market share on Arbitrum and 20% on Ethereum, we get about 2.5× current volumes and fees (if fee rates are roughly the same as on Base).

Valuation and market position

Combined FDV for AERO + VELO is now ~$1.6B, with about 50% of tokens locked in ve-positions, implying a circulating market cap ~ $800M. Annual inflation is ~13%. With a one-year horizon (if tokenomics don’t change) you can assume FDV ~ $1.81B and market cap ~ $905M.

After annualizing expected fees, I get ~$480M paid out to veAERO holders.

Assuming a 50% lock/circulation, the average APR on veAERO comes out about ~53% (payback from current prices < 2 years)

Note: These results rest on assumptions—expansion + consolidation, achieving decent market share on mainnet/Arbitrum, and September 2025 volumes staying stable (a bear market would lower them). On the other hand, I don’t factor in growth of the addressable market, which may be conservative.

Growth of the addressable market

Beyond the four main chains (current + logical branches), there are several ways to grow further:

- ◆New chains: e.g., Robinhood chain, Plasma, Converge…

- ◆Launchpad: Aerodrome launched a launchpad; the first project Syndicate incentivized liquidity with about $20M extra in SYND tokens within a single week. Other projects like Lit Protocol have been announced to launch soon.

- ◆New services:relayers, a marketplace for veAERO NFTs, front-end fees rebated to veAERO holders, etc.

- ◆

Even if the market-share estimates above are overstated, market expansion alone can comfortably get to $40M monthly / $480M annually in fees + external incentives.

3) The first ****** Labs that grows the pie

A newly forming Labs is a joint-stock company meant to stand behind Aerodrome (name/function not fully revealed). This is interesting because Alex has long insisted on alignment of incentives between the team and token holders—something that often clashes with having a separate company behind a project, as that pushes incentives for the team to care about the company, not the token—as we know from Uniswap and Uniswap Labs.

Why Labs? It enables what wasn’t previously possible:

- ◆BD and legal framework for deals with large exchanges/companies.

- ◆Team expansion and faster shipping.

- ◆Possible products: official relayers (managing veAERO locks and voting for a fee), mobile app, better front-end, a veAERO marketplace directly in the app, perhaps prediction markets later, etc.

To keep incentives aligned with veAERO, profits from new products must flow to veAERO holders, not to an off-chain corporation. Howto finance the Labs then?

My hypothesis: Labs will leverage the fact that the AERO token carries great yield (30–60% annually), become a large veAERO NFT holder, and finance operations from these yields.

A second layer of speculation: to raise initial capital, Labs becomes a DAT (Digital Asset Treasury)—sell equity to investors, use the proceeds to buy AERO, lock it, and finance product development and protocol growth from the yield.

My base case for ***** Labs:

- ◆Raise funds from investors to buy AERO.

- ◆Lock into veAERO and actively manage voting.

- ◆Finance product development and expansion from the yield.

- ◆Goal of all products: increase yield to veAERO, which raises AERO value → larger incentives for LPs → better liquidity → higher market share.

- ◆Use surplus profits to buy more veAERO

This is the only realistic scenario I can think of for operating sustainably while keeping incentives aligned as they are now—i.e., all cash flowing to veAERO.

I couldn’t come up with any other scenario in which this Labs isn’t net extractive, so even though I don’t have as many “proof points” here as in the first two parts, I don’t see another way to finance it.

Opportunity

Valuation based on revenue

If the market values AERO+VELO today at ~$1.6B and DEX fees rise on average by ~140% (see table), then fair value could also be ~140% higher, i.e., ~$3.8B.

After accounting for 13% annual inflation, that implies a ~$1.9 price within <12 months.

Relative valuation

If Aerodrome bites into mainnet and Arbitrum and maintains leadership on Base and OP Mainnet, it will no longer be obvious whether Uniswap remains the dominant DEX.

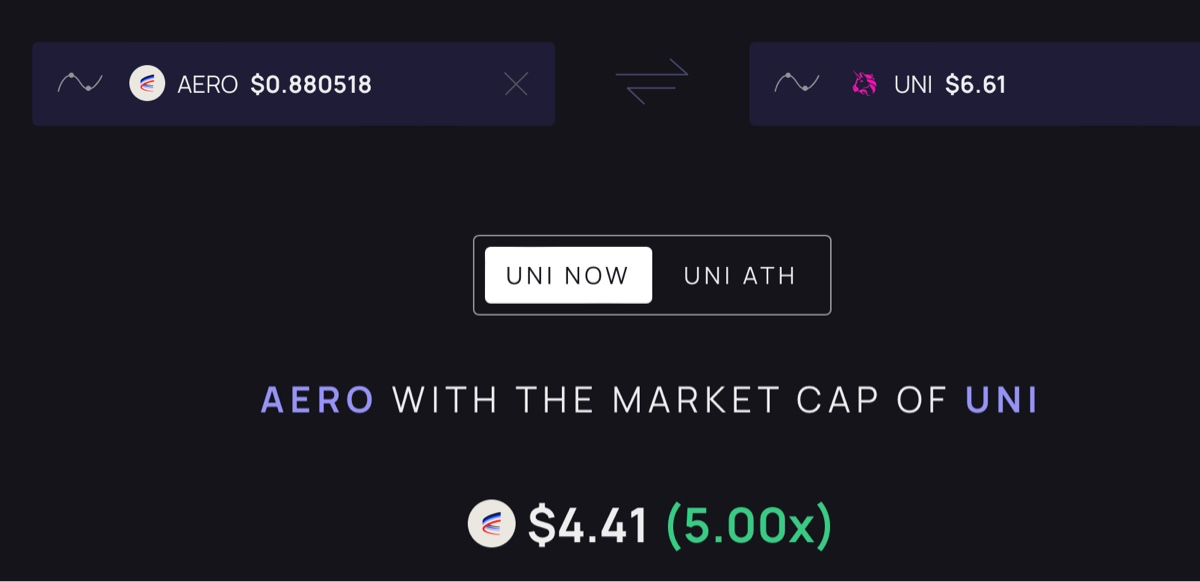

Also, because AERO has a direct claim on protocol success (unlike UNI), it may gain an index premium. A realistic comparison target is UNI’s value (currently ~5× above Aerodrome). If Labs also delivers “off-chain” value comparable to Uniswap Labs (a 2022 round at ~$1.7B), AERO’s comparative value could be even higher.

Scenarios

- ◆Bear case: expansion/merge only partially succeeds, low share on mainnet/Arbitrum, fees +30%, market values purely on revenue, Labs without DAT. Target: $1.0–1.2.

- ◆Base case: expansion to mainnet + Arbitrum and consolidation under one DEX; at least 15% market share on mainnet and 30% on Arbitrum; Labs as DAT but without large veAERO accumulation. Target: $2–3.

- ◆Bull case: consolidation + expansion to Ethereum and Arbitrum with solid share; Aerodrome consistently surpasses Uniswap in volumes; AERO is treated as a DEX index; Labs raises >$50M to accumulate veAERO and ships products that return value to veAERO. Target: $5–10.

Risks

- ◆Incomplete information: this is a speculative thesis based on public breadcrumbs; the November announcement may be different. Due to this “fog of information,” the asymmetry exists if it plays out as expected.

- ◆Mainnet risk: high gas and a different participant mix can make it harder to win liquidity/volumes; it would undermine the current “we win where we play” positioning.

- ◆Migration risk: any potential Aero + Velodrome merge must be handled sensitively so the community doesn’t feel harmed. The team historically executes to a high standard, but it’s still a difficult task.

- ◆Inflation risk: with migration to new chains, more incentives may be needed to attract liquidity. The current 13% annual inflation may therefore change—but it would still be offset by higher fees paid to veAERO.

Time horizon

This thesis should be confirmed or rejected by roughly the end of 2025.

If the November announcement confirms the thesis, the time to visible market impact should extend (~6 months).

Invalidation of the thesis

I would consider this thesis invalidated if:

- ◆The November announcement is about something else, or doesn’t include at least two of these three parts.

- ◆They truly launch, for example, on mainnet and after the first ~month have a negligible market share (<5%).

Conclusion

Aerodrome and Velodrome are leading DEXs on most chains where they compete with Uniswap, even after three years of operation. This confirms their structurally superior model.

The Aerodrome team is aware of this competitive advantage and will want to press it. From the available information, I conclude they will expand Aerodrome to additional chains, which will increase volumes traded on it and bring more fees.

I expect that this time they won’t do a new fork; instead they will merge the two existing projects and make one big DEX that will try to dethrone Uniswap as the current king of decentralized exchanges.

To enable moves that were not previously possible, they will set up their own company to build products for Aerodrome. My expectation is that this company raised money from investors, is accumulating veAERO, and will finance its operations from protocol income in this way, which keeps incentives aligned with token holders → maximizes AERO’s value.

If I’m right with this thesis, I think AERO offers an asymmetric buying opportunity at the current $0.88 price. The base case is 100–200% appreciation over the next half-year.

The main risk is that I’m wrong about what to expect from the November announcement, because nothing has been publicly announced and I’m working only with terse information from the team on X, Discord, and in podcasts

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.