YieldBasis: Curve Founder’s Solution to Impermanent Loss and BTC Yield

TLDR on the protocol:

- ◆YieldBasis lets you earn yield on your BTC by providing liquidity to an AMM pool without suffering from impermanent loss

- ◆Protocol is live with organic (unsubsidized), scalable BTC yield – ETH, SOL, BNB support coming soon

- ◆Native $YB token captures fees generated by the protocol, works as a next-gen CRV model with a reinvented emission algorithm

TLDR on the bet:

- ◆Massively oversubscribed (195x from public USDC deposits from 67k participants) on the Legion x Kraken launchpad

- ◆Massively oversubscribed (237x from 212k participants) premier sale at Binance Wallet

- ◆Huge demand on premarket Binance perps, holding between $1.3-2 even during the flashcrash

- ◆Strong value accrual to the token – long term locks, protocol fees, governance power

- ◆No free tokens: all emissions are bought by LPs who must forgo their BTC yield to get tokens

The Problem of Impermanent Loss

In traditional AMMs, your position’s value grows with the sqrt(BTC price) because of the x*y = k formula (for CPAMM invariant provided here; however, other AMMs also have similar high-level properties and have the same issue that LPs face)

- ◆Say you deposit 1 BTC (assuming price is $100k) and $100k of USDC into a pool

- ◆If BTC doubles in price to $200k, your position would be rebalanced to maintain equal value in each token so you’ll end up with ~.7 BTC and $141k USDC, worth $282.8k

- ◆If you had just held your BTC and USDC outside the pool, they’d be worth $300k

- ◆That ~$17.2k difference is impermanent loss

This is one of the reasons why the majority of BTC in defi is deposited to lending markets. Nobody wants to miss out on $BTC gains during growth cycles due to IL. While there are some hedging strategies to account for IL, there aren’t any real solutions that just work without active management.

Yield Basis Solves Impermanent Loss

The position value in a typical AMM is proportional to the sqrt(price) of the volatile asset, but Yield Basis makes it possible for the position to linearly track the asset’s price using a specifically designed leveraged position.

Each pool consists of three components

- ◆The pool proper (a TwoCrypto pool holding collateral vs. crvUSD)

- ◆The Releverage AMM (pool holding TwoCrypto LP tokens vs. crvUSD)

- ◆The Virtual Pool (a wrapper over the Releverage AMM that exposes crvUSD/collateral trades to the arbitrageurs who play a role in rebalancing the pool debt-to-value ratio). Detailed explanation here.

The chosen compounding leverage value is maintained by the special releverage AMM ensuring 2x leverage using crvUSD credit line to the protocol.

When a user deposits collateral, presently wrapped BTC, the equivalent amount of crvUSD is borrowed and deposited. The LP token is then used as collateral for the position.

For every dollar of collateral value, the position is priced at two dollars, making the dollar amount of crvUSD debt precisely half the collateral for the loan.

When the pool is balanced, this generates twice the fees that the collateral alone would generate, and the strategy is equivalent to regular leverage.

However, when the pool becomes imbalanced due to a price shift, a pointwise leveraged position would incur impermanent loss.

Yield Basis prevents this by deliberately skewing the LP/crvUSD prices in the Releverage AMM.

This exposes a small spread to arbitrageurs, who can restore the pool's debt-to-value ratio and earn a premium without any need for centralized action.

This consumes half of the generated fees, but the generated fees are doubled compared to the unleveraged position, meaning that stakeholders do not experience a decrease in income.

(Note that this mechanism applies to the rebalancing of the CDP, not the underlying TwoCrypto pool. The TwoCrypto pool uses the standard Cryptoswap mechanism for rebalancing.)

You can review the full math in the original whitepaper here, but here’s a short summary and example:

- ◆Say you start with 1 BTC at $100k

- ◆The protocol borrows $100k of crvUSD against your BTC, using the soon to be created LP token as collateral

- ◆Both your BTC and the crvUSD are deposited into the Curve pool, minting a $200k, 50:50 LP position

- ◆The $200k LP token backs the $100k crvUSD debt, giving a 2:1 debt ratio which is continuously maintained through automatic rebalancing

The key idea:

- ◆Whenever BTC price shifts, the releverage AMM reprices LP tokens to create a profitable arb opportunity

- ◆Arbitrageurs are incentivised to step in to restore the protocol’s leverage ratio, keeping your position in sync with the underlying asset

If BTC price goes down:

- ◆The value of the LP depreciates, debt stays constant, leverage rises above 2x

- ◆Re-leverage AMM offers LP tokens at a small discount, and arbitrageurs supply crvUSD to reduce debt and position size proportionately

YieldBasis in Action Today

The protocol is currently live on mainnet with a capped $30m TVL in wrapped BTC. This will soon be expanded up to $150m (subject to CurveDAO voting).

You can find live stats on Valueverse ybBTC tracking here.

YieldBasis successfully passed the recent flashcrash test, with 2 hours of volatility bringing $12.7m of trading volume and 0.6 BTC + $60k crvUSD in fees per pool.

The $YB Token

YieldBasis’s native token $YB is the next version of the CRV -> veCRV model pioneered by Michael Egorov, the founder of both Curve and YieldBasis.

This model has become popular amongst many defi protocols, but after 5 years of mainnet CRV, notable improvements have been made, and I see $YB as a CRV v2 with improved distribution.

As with CRV, the YB token has no utility in its unlocked form and must be locked in the veYB contract to activate token utility and accrue value.

When locked, the veYB position owner receives a corresponding share of protocol fees and voting power.

You can also stake your YieldBasis LP token (ybBTC) in the special contract (with no unstake period) and receive YB emissions instead of native BTC yield.

While you might be familiar with CRV style utility, YB’s emissions are a bit different:

- ◆The token are earned through LPs forgoing yield for them (we can imagine here that tokens are bought from the protocol using the LP position yield)

- ◆As a result, there are two prices for $YB – an internal price (for LPs who forgo yield) and an external market price

- ◆Emissions are dynamic and depend on the share of LPs staking their tokens, so it’s dynamically adjusted accordingly to the share of LPs willing to receive YB

- ◆Therefore, a share of LP yield goes to LPs that don’t receive YB, and the rest go to veYB. This means that the new token emissions are not a protocol expense, but rather an additional cashflow stream for token stakers.

A concrete example of $YB value accrual might look like:

- ◆Protocol generates yield for wrapped BTC (without IL risk) – users deposit BTC and receive ybBTC

- ◆Some LPs decide to receive YB instead organic BTC yield (if nobody takes this, a minimal admin fee of 10% is applied to all fees generated)

- ◆veYB token holders receive fees (and governance rights that can be possibly monetized via bribes in the future)

This means that for 50% of LPs receiving emissions, 36% of all trading fees captured in YieldBasis pools are going to veYB.

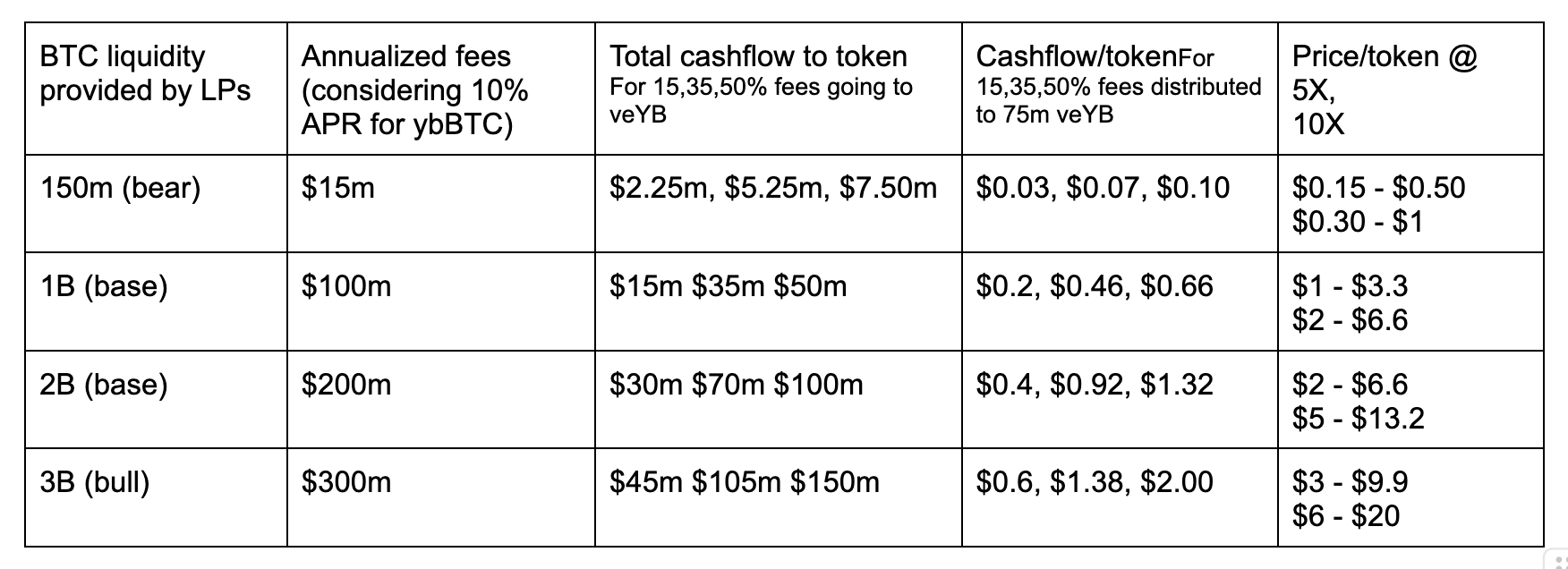

Extrapolating fees and token price scenarios out to March 2026:

- ◆A maximum of 109-150m YB tokens will be in circulation, so no more than 150m tokens can be locked in veYB

- ◆Let’s estimate 75m YB tokens are locked in veYB (likely to be lower since veToken lockup rates are typically 33-50%)

- ◆We can conservatively assume that tokens accruing fees to the holder can be valued at at least 5-10x annual revenue per token

Base, Bear, Bull Cases

These numbers paint a clear picture as to why the project was massively oversubscribed at $0.20 per token, and why the pre-market price of $1.25-1.80 holds up so well, even after the marketwide flush.

YieldBasis is a cashflowing machine for veYB holders, capturing a significant share of fees from all pools. This is without accounting for the governance value through bribes a la Curve Wars that we expect to be introduced later when more pools are created and competition picks up for YB emissions.

Comparing with other veTokens – $CRV, $AERO

- ◆$54m of cashflow to 1veCRV (fees + bribes)

- ◆$0.067 per 1veCRV drives $726m market cap/$1.2B FDV, $CRV price $0.51 [CRV metrics]

- ◆$296m of cashflow to veAERO (fees + bribes + rebase)

- ◆$0.20 per 1veAERO drives $775m market cap/$1.5B FDV, $AERO price $0.85 [AERO metrics]

$CRV is priced at 7.6X, $AERO priced ~4X.

Even for the bear case of $150m TVL (meaning that Yield Basis adds zero additional TVL in the next 3-4 months) fundamentally-driven token price is $0.5-$1.00. For base and bull cases, TVL and fees are an order of magnitude higher.

All numbers are presented as an estimate from fundamental cashflow metrics and does not take into account a narrative premium and other market sentiment around BTC yield.

Upcoming Catalysts

- ◆TVL cap expansion from $30m to $150m (should be live by the time this piece goes out): TVL growth directly brings more fees for veYB

- ◆High BTC Volatility: More trading volumes = more fees captured

- ◆ybBTC LP token approved as collateral on lending markets: enables new strategies and drives BTC TVL into YieldBasis

- ◆ETH, BNB, SOL as supported assets: brings additional fees from new pools

Risks

- ◆Smart contract risk: YieldBasis has had 6 security audits, as well as a Sherlock bounty. Regardless, this is still a brand new protocol and mechanism that must be battle tested

- ◆CurveDAO governance: if the DAO doesn’t approve limits for TVL increases, it becomes difficult to grow revenue. Highly unlikely given DAO receptiveness so far.

- ◆Low volatility risk: YB generates fees from trading volume, and trading volume depends on market volatility. If BTC and broader market flips bearish, fees may reduce and valuation may get compressed

- ◆Other sources of BTC yield: if BTCfi picks up and there are higher sources of BTC yield elsewhere, TVL may migrate there instead

Big thanks to Llama for helping me understand the protocol, and even bigger thanks to Vasily and Valueverse for the patience in helping me draft this piece and work through the math.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.