Upside optionality in $SIGN if nations can be onboarded via 2G efforts while maintaining 20-30 mm ARR amidst tough-comp

TL;DR

- ◆Profitable Core Business: Sign Protocol’s TokenTable platform earned ~$15 M in 2024 revenue from token distribution fees (airdrop claims and OTC unlock trades) (Sign Protocol 2024 Revenue Data).

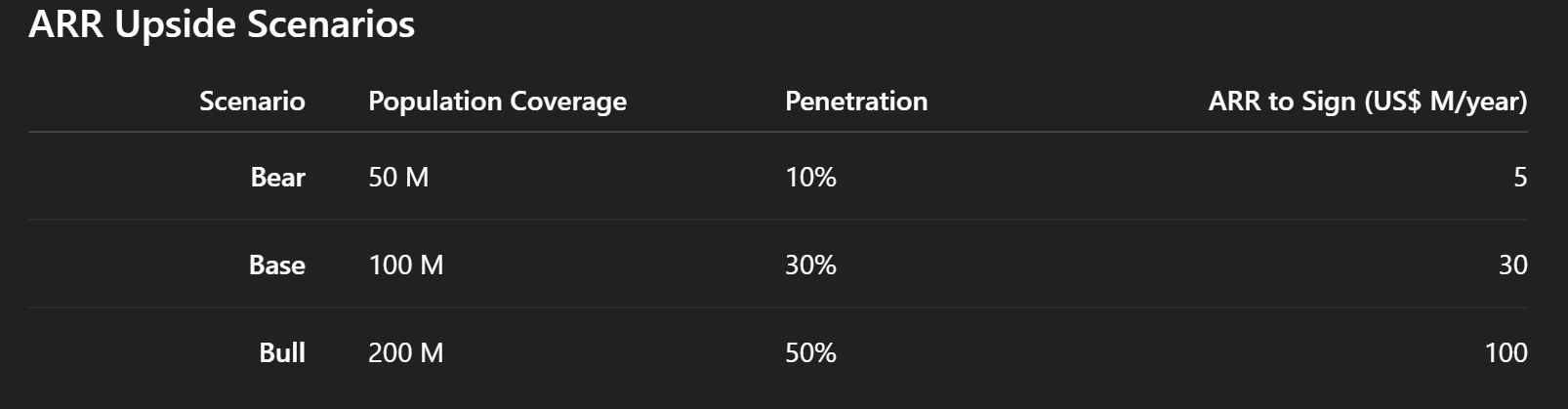

- ◆Government Contract Upside: Early pilots in Sierra Leone and Ras Al Khaimah demonstrate blockchain‐based ID and e-government infrastructure (Sierra Leone Case Study; RAK Case Study). Scaling to crypto-friendly nations at $1 per citizen/year could add $5 M–$100 M+ ARR depending on penetration.

- ◆Token Value Catalysts: High-margin profits (>$20 M net income run-rate), ongoing token buybacks, a 50k-strong community flywheel, and new distribution channels (SignPass identity, wrapped-stock integrations) underpin potential re-rating of the $SIGN token.

1. Revenue Base and Growth Outlook

Sign Protocol’s TokenTable is the go-to platform for automated token distributions, covering over 40 M users and investors to date (Usage Statistics). In 2024, it generated $15 M purely from claim fees and OTC unlock service fees, with minimal incremental cost due to its SaaS model (Sign Protocol 2024 Revenue Data).

Key growth drivers toward $20–30 M/year:

- ◆Expanded Airdrop Claims: As new token projects proliferate (projected millions annually, per the Tiger Research Web3 Growth Report), TokenTable’s claim-fee business should scale nearly linearly with project count and user adoption.

- ◆Launchpad & Exchange Mandates: Major exchanges now require transparent vesting and distribution frameworks. TokenTable’s smart-contract–backed solution addresses this compliance gap, positioning it as an industry standard.

- ◆New Feature Monetization: Innovations like locked-token derivatives, advanced analytics, and “TokenTable Lite” for smaller projects can unlock fresh fee streams without significant ops expense.

Conservative modeling yields low-$20 M revenue; broader adoption could approach $30 M+ within 12–18 months.

2. Government Contract Optionality

Sign’s move into sovereign infrastructure has produced two high-visibility pilots:

- ◆Sierra Leone: Blockchain-verifiable digital ID cards issued via Sign’s protocol, validating on-chain resident data (Sierra Leone Case Study).

- ◆Ras Al Khaimah (UAE): On-chain residency visas for Web3 entrepreneurs in RAK’s free zone, integrated into SignPass (RAK Case Study).

Target markets include Thailand (70 M pop., top-10 global crypto adoption), Turkey (85 M), Indonesia (273 M), and Nigeria (219 M) per Chainalysis’ 2023 index (Chainalysis 2023 Crypto Adoption Index).

Assumes $1 per citizen/year contract value.

Even a single large‐country deal (100 M people at 30% usage) adds $30 M to ARR—doubling Sign’s current business. Multi-year (3–4 Y) contracts provide revenue visibility and high margins.

3. Token Valuation Implications

Profitability & Buybacks

With >$20 M net income run-rate and lean ~$350 K/month opex, Sign resembles a high-margin SaaS. Management’s use of surplus cash to buy back early tokens reduces float and mitigates sell-pressure, effectively redistributing value to holders.

Community Flywheel

Sign’s 50k+ member community drives organic adoption. High engagement (fans even tattoo the Sign logo) powers word-of-mouth growth, amplifying TokenTable uptake and brand mindshare without costly marketing.

New Distribution Channels

- ◆SignPass Identity: On-chain credentials for nationals and entrepreneurs bolster Sign’s institutional footprint.

- ◆Wrapped-Stock Integrations: Partnering with tokenized-equity platforms (e.g., Backed.fi) to offer U.S. stocks to underserved retail markets creates new fee pools (Backed.fi Tokenized Stocks Report).

Mindshare & Re-Rating

As Sign consolidates its revenue lead in Web3 infrastructure and lands government contracts, the market may repriced $SIGN higher. A profitable, buyback-backed token with expanding use cases and decreasing supply supports a significant upside from current levels.

Conclusion:

Sign Protocol uniquely combines a profitable Web3 SaaS with a credible path to real-world sovereignty infrastructure. The dual streams—TokenTable growth and government contracts—plus robust tokenomics and community dynamics, make $SIGN a compelling long-term holding. Execution on pilots and feature rollouts over the next 12–24 months will be key catalysts for token re-rating and sustained value creation.

This article is being AI-generated based on the May 15th, 2025 BidCast Episode on $SIGN and may contain mistakes. It does not constitute as investment or any advice and does not represent the view of the BidClub.io platform.

Generated by grok.com and chatgpt.com

BidCast Source: https://www.bidclub.io/posts/cmaw6ghrg0001v8272jwdgnvu

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

0

0