Maple: On-Chain Lending Powerhouse

Publish Date: April 21, 2025

Thesis Summary

Maple offers institutionally underwritten credit products delivered through on-chain infrastructure. Their core business today is offering fixed-rate, overcollateralized loans to borrowers like market makers, trading firms, and crypto-native funds.

This is a very sizable market as lending remains one of the largest and most durable markets in crypto. At the end of 2024, DeFi loans = $25B, CeFi = $11Bn, for a total of $35B+ in loans outstanding.

Notably the size of CeFi lending is down significantly, still 3X smaller vs the $35B+ in loans at the peak of last cycle (when Genesis, BlockFi, Celsius dominated the market).

Maple has scaled very rapidly in the past year:

- ◆$1B+ TVL

- ◆$450M+ loans outstanding

- ◆$8M+ annualized protocol revenue

TVL has grown 10X+ YoY from April 2024 to April 2025. Even at this scale, Maple represents <5% share of CeFi lending markets, and ~1% share across all crypto lending. There continues to be significant room for expansion both in Maple's share of the market, and in CeFi loans as a category.

Maple targets scaling to $4B+ in TVL by end of 2025, which would position them to generate $35M in protocol revenue, $20M+ in net earnings and translate to a $500M-1B protocol outcome (vs current $150-200M fully diluted valuation).

Market Opportunity

The institutional lending market in crypto has undergone sharp cycles over the past few years. It peaked at $35B outstanding loans in Q1 2022 before collapsing due to poor underwriting, concentrated counterparty risk, and fraud. Today, the CeFi loan market stands at ~$11B, smaller, but still significant. As trust rebuilds, we’re seeing a shift toward more transparent and compliant lending infrastructure.

Source: Galaxy (https://www.galaxy.com/insights/research/the-state-of-crypto-lending/

In a typical institutional lending flow:

- ◆Lenders are funds, family offices, high net worth individuals (HNWI) looking to earn yield on idle stablecoins (eg USDC, USDT)

- ◆Borrowers are trading firms accessing liquidity for arbitrage, delta-neutral, or directional strategies, willing to collateralize non-stable assets (eg BTC, ETH, SOL)

- ◆Platforms handle underwriting, custody, and collateral management, typically with liquidation rights in the event of default

Most loans are overcollateralized (120–170%), with BTC, ETH, or stablecoins held at custodians like Anchorage, BitGo, or Copper.

While DeFi lending markets like Aave, Morpho, Kamino, Euler, Compound have grown substantially, many institutional borrowers continue to favor CeFi venues. This comes down to a few structural differences:

- ◆Legal Agreements vs Smart Contracts. Most large borrowers operate within a regulated framework. They require enforceability, documentation, and legal recourse. CeFi platforms offer traditional loan agreements governed by real-world jurisdictions. In contrast, DeFi protocols rely entirely on smart contracts, with limited remedies if things go wrong.

- ◆Fixed Rate + Fixed Term Loans. DeFi loans are typically floating rate and open-term. During periods of volatility, borrowing costs can spike without notice. CeFi lenders like Maple offer fixed rate, fixed duration loans (e.g., 30 days at 10% rate) providing borrowers with predictability around funding costs and maturity.

- ◆KYC/AML Compliance. Many market makers and hedge funds are restricted to transacting with KYC’d counterparties and must avoid exposure to sanctioned entities or high-risk jurisdictions. This prevents them from borrowing via DeFi protocols like Aave, where counterparties are anonymous and no KYC is enforced.

Maple Finance Overview

Maple Finance was founded in 2019 by Sidney Powell and Joe Flanaganas a digital asset lending platform focused on institutional borrowers. The product initially launched with a marketplace model, but over the past 2 years (since 2023) has evolved into a vertically integrated lender via Maple Institutional. Under this model, Maple itself directly underwrites and originates loans.

Source: Maple Website (https://maple.finance/)

All borrowers on Maple Institutional are fully KYC’ed and must pass a multi-step credit underwriting process. This can include:

- ◆Financial diligence: review of historical income statement, balance sheet strength (particularly liquid assets), and leverage metrics

- ◆Qualitative diligence: interviews with management, assessment of risk controls, use-of-proceeds, and trading strategy alignment

- ◆Operational assessment: ability to meet margin calls, real-time collateral tracking, integration with custodians

Maple extends fixed-rate, fixed-duration loans typically backed by 120-170% overcollateralization, with assets such as BTC, ETH, and stablecoins. Collateral is held in custody through institutional partners like Anchorage, BitGo, and Copper. Tri-party agreements sit in place between borrower, custodian, and Maple Institutional.

Upon loan origination, Maple’s operations team monitors real-time collateral levels through custodian APIs and on-chain dashboards. Margin call thresholds are explicitly set: if collateral drops below the “margin call value,” borrowers are given 24 hours to top up. If the collateral reaches the “liquidation value,” Maple has unilateral rights to liquidate assets to protect principal.

Importantly, all Maple Institutional lenders must undergo KYC, including crypto funds, family offices, and other allocators. This is a key regulatory safeguard for borrowers, who are often required to prove compliance with AML/KYC obligations when sourcing capital.

Maple Institutional is structured around a few lending pools, allowing lenders to select risk exposure. This segmentation creates clear boundaries for underwriting and gives depositors control over their risk/return profile.

- ◆Blue Chip Secured: lends only against BTC and ETH collateral, targets 10-12% APY

- ◆High Yield Secured: allows a broader set of assets (e.g., SOL, XRP) as collateral, targets 15-20% APY

Since launch, Maple Institutional has grown steadily to ~$400M in TVL, with consistent demand from both sides of the marketplace. In March 2025, Maple onboard Bitwise ($12B+ asset manager), a demonstration that larger, more traditional allocators are beginning to engage with on-chain lending products that offer institutional level risk management.

Source: https://maple.finance/news/bitwise-maple-allocation

Syrup Finance

In May 2024, Maple launchedSyrup, a permissionless lending protocol designed to sit alongside Maple Institutional. Syrup retains the same credit standards and collateral protections as its institutional counterpart. However it allows the lender side of the marketplace to open up non-KYC participants.

This structure preserves borrower quality (as institutions must still pass full KYC and underwriting) while broadening capital access through on-chain liquidity. By opening up the source of capital to a broader permissionless pool, this enables lower cost of borrow.

Source: Syrup Loans (https://syrup.fi/details)

For example, Syrup recently received a $50M allocation from Spark(formerly Maker) - one of the largest single deposits, and an example of allocations not possible via Maple Institutional.

Source: Maple Website (https://maple.finance/news/spark-integrates-with-maple-and-allocates-initial-50m)

As of April 2025, Syrup has scaled to $550M+ in TVL. This surpasses Maple Institutional (1.5x higher TVL) and is the fastest growth driver for Maple.

Source: Syrup Home Page (https://syrup.fi/)

Lenders deposit USDC into Syrup and receive back syrupUSDC, a liquid receipt token that represents their share of principal and accrued interest. This creates several benefits for on-chain users:

- ◆Instant Liquidity: Maple seededa $10M Uniswap pool in February 2025, enabling USDC <> syrupUSDC swaps. This allows depositors to exit positions without waiting for repayment cycles or redemption queues. The pool covered ~9% of syrupUSDC supply at launch, offering reasonable depth for smaller withdrawals.

- ◆Composable Yield: syrupUSDC integrates with protocols like Pendle, allowing users to lock in fixed yields or trade future yield streams. This makes Syrup attractive to more yield-sensitive or duration-aware capital, especially in flat or declining rate environments.

- ◆Lending Protocol Support: syrupUSDC is supported as collateral on lending platforms such as Morpho, unlocking additional utility for holders. This adds capital efficiency to the product, allowing users to borrow against yield-bearing assets or layer additional strategies on top. The Morpho pool for syrupUSDC currently has $30M+ USDC deposits with $27M+ in borrow.

Source: Morpho syrupUSDC pool (https://app.morpho.org/ethereum/market/0x729badf297ee9f2f6b3f717b96fd355fc6ec00422284ce1968e76647b258cf44/syrupusdc-usdc)

The key distinction with Syrup lies in its permissionless design. Anyone can deposit USDC and earn yield, while borrowers remain gated through Maple’s institutional onboarding. This structure combines the strengths of DeFi for capital formation, and CeFi for credit underwriting and risk controls.

All loans remain overcollateralized, executed on-chain, and custodied with trusted partners like Anchorage and BitGo.

Syrup has emerged as a core growth driver for Maple. With no onboarding friction, high net yields, and the ability to plug into DeFi primitives, syrupUSDC is becoming a default stablecoin vault for on-chain capital seeking institutional credit exposure. All without the compliance overhead of direct participation in Maple Institutional.

BTC Yield

In February 2025, Maple expanded beyond lending with the launch of BTC Yield, a product designed to generate BTC-denominated yield for institutional and accredited investors. The product was built in partnership with Core Foundation, leveraging its dual-staking mechanism to stake BTC alongside CORE tokens and secure the Core blockchain.

Unlike most yield offerings in crypto, BTC Yield is structured to minimize platform risk and denominate returns in BTC (eg not points, other tokens). Most importantly, BTC is custodied with institutional-grade providers (BitGo, Copper, and Hex Trust) under time-locked wallet structures using Bitcoin-native CLTV (Check Lock Time Verify) functionality. BTC is never moved out of custodian vaults. CORE tokens are received as rewards, and Maple manages the conversion of CORE rewards back into BTC to pass yield to depositors.

The product targets 5%+ APY with 90-day lockups, with yield sourced entirely from Core’s native staking incentives. As of April 2025, BTC Yield has scaled to $100M+ in TVL, making it one of the fastest-growing product lines in the Maple ecosystem.

Maple plans to issue lstBTC, a liquid staking token that represents positions in BTC Yield. This will unlock composability for BTC deposits, allowing users to use lstBTC as collateral in DeFi (eg Morpho, Pendle) or trade it on secondary markets (eg Uniswap), mirroring what syrupUSDC enabled for Syrup as a key growth driver.

BTC Yield marks Maple’s first step outside of pure lending, and a proof point for how Maple can extend its credit, treasury and custody infrastructure into adjacent categories.

Growth Roadmap

Maple has grown significantly across all its product lines over the past 12 months. As of April 2025, Maple has surpassed $1B+ in total TVL, with $550M+ from Syrup, ~$400M from Maple Institutional, and $100M+ from BTC Yield.

On the borrower side, Maple has scaled its active institutional borrower base from 4 to 28 counterparties over 2024. On the lender side, the number of institutional allocators has grown 15x to ~800.

Importantly, the platform has had no loan defaults across more than $600M in cumulative originations (through end of 2024) across Maple Institutional and Syrup.

Source: Dune Dashboard (https://dune.com/maple-finance/maple-finance)

Maple’s growth has been driven by the highly risk-adjusted yields it offers depositors. For 2024 this was net APY of 16.8% for High Yield Secured, 10.2% for Blue Chip Secured, and 21.3% for Syrup. Importantly, pool collateralization levels remain very conservative, averaging 160%+ across all its product categories.

Source: Maple Yield Performance 2024 Recap (https://maple.finance/news/maple-yield-performance-2024)

Competitive yields have driven much of Maple’s organic growth, especially during a period of declining rates and muted crypto market activity. Syrup, in particular, has benefited from a combination of permissionless access and real-time liquidity through syrupUSDC.

Average withdrawal performance has been strong:

- ◆Syrup withdrawals settle in <24 hours

- ◆Maple Institutional withdrawals settle in 2–3 days

syrupUSDC holders can also exit instantly via secondary liquidity on Uniswap at prevailing market rates.

Maple’s revenue model is straightforward:

- ◆Lending: The protocol takes 15–20% of total borrower interest as revenue. At current loan rates (~8–9%) and a $450M+ loan book, this equates to a ~150bps net interest margin, or ~$7M in run-rate revenue.

- ◆BTC Yield: Maple earns a 0.4% management fee and takes 20% of staking yield from CORE rewards. At $100M TVL and ~5% gross yield, this contributes ~140bps net, or ~$1.4M in run-rate revenue.

As of April 2025, Maple is currently generating $8M+ in annual protocol revenue, with material upside from TVL growth, new borrowers, and a higher yield environment.

Looking Ahead

Maple targets $4B in TVL by year-end 2025, with growth expected to come from both business categories:

- ◆Maple Institutional + Syrup: $2.5B (3x current TVL)

- ◆BTC Yield: $1.5B (from ~$100M today)

At this scale, Maple could support:

- ◆$1B active loans @ 1.5% net interest margin = $15M in lending revenue

- ◆$1.5B BTC deposits @ 1.0-1.5% fee = $15-22M in BTC Yield revenue

Together, this would imply ~$35M in annual protocol revenue, with significant operating leverage as fixed costs remain relatively stable.

Importantly in a higher yield environment, Maple could earn closer to ~200bp on its loan book resulting in $20M lending revenue on $1B loans outstanding.

Source: Maple Q1'25 Update Call

Token Value Accrual

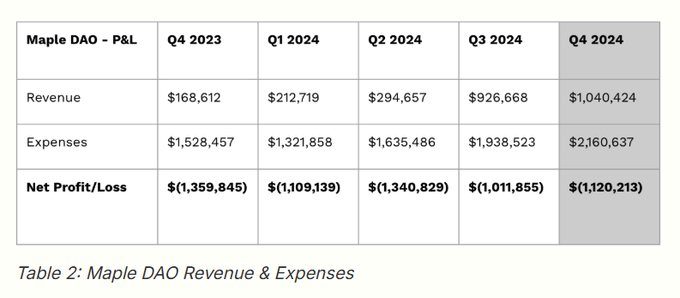

Maple is a token-only protocol, with SYRUP token serving as the primary mechanism for value accrual. As of April 2025, the protocol generates $8M+ in annual revenue, compared to ~$8M in annualized expenses (~$2M per quarter), putting it just at/over breakeven.

Maple has already shown signs of significant operating leverage. From Q4 2023 to Q4 2024:

- ◆Revenue scaled 6x (from $170K to $1.04M)

- ◆Expenses increased just 41% (from $1.5M to $2.2M)

This decoupling between revenue growth and cost structure is a key driver of long-term tokenholder value. As TVL and loan volume scale, most incremental revenue drops to the bottom line.

Source: Maple Treasury Report Q4'24 (https://maple.finance/news/q4-2024-treasury-report)

In January 2025, Maple passed a proposal to direct 20% of protocol revenue toward SYRUP buybacks and staking rewards. Under the new model:

- ◆SYRUP holders who stake their tokens (no lockup required) receive pro-rata distributions from the buyback pool

- ◆The remaining 80% of revenue continues to fund operations and reinvestment

Unlike many token projects where value accrual is speculative or deferred, Maple has already begun aligning revenue and tokenholder rewards in a tangible way while balancing continued growth investments.

Conclusion

Maple has validated a model that combines the risk controls of CeFi with the transparency and composability of DeFi. With three distinct and growing product lines, $1B+ in TVL, and a credible path to $35M+ in revenue (at 30x revenue = $1B fully diluted valuation), we see Maple as one of the most durable DeFi and credit primitives in crypto.

As capital continues to seek yield in a post CeFi world, we believe Maple is well-positioned to become the default infrastructure for institutional lending and treasury management.

LEGAL DISCLAIMERS

THIS POST IS FOR INFORMATIONAL PURPOSES ONLY AND SHOULD NOT BE RELIED UPON AS INVESTMENT ADVICE. This post has been prepared by Modular Capital Investments, LLC (“Modular Capital”) and is not intended to be (and may not be relied on in any manner as) legal, tax, investment, accounting or other advice or as an offer to sell or a solicitation of an offer to buy any securities of any investment product or any investment advisory service. The information contained in this post is superseded by, and is qualified in its entirety by, such offering materials.

THIS POST IS NOT A RECOMMENDATION FOR ANY SECURITY OR INVESTMENT. References to any portfolio investment are intended to illustrate the application of Modular Capital’s investment process only and should not be used as the basis for making any decision about purchasing, holding or selling any securities. Nothing herein should be interpreted or used in any manner as investment advice. The information provided about these portfolio investments is intended to be illustrative and it is not intended to be used as an indication of the current or future performance of Modular Capital’s portfolio investments.

AN INVESTMENT IN A FUND ENTAILS A HIGH DEGREE OF RISK, INCLUDING THE RISK OF LOSS. There is no assurance that a Fund’s investment objective will be achieved or that investors will receive a return on their capital. Investors must read and understand all the risks described in a Fund’s final confidential private placement memorandum and/or the related subscription posts before making a commitment. The recipient also must consult its own legal, accounting and tax advisors as to the legal, business, tax and related matters concerning the information contained in this post to make an independent determination and consequences of a potential investment in a Fund, including US federal, state, local and non-US tax consequences.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS OR A GUARANTEE OF FUTURE RETURNS. The performance of any portfolio investments discussed in this post is not necessarily indicative of future performance, and you should not assume that investments in the future will be profitable or will equal the performance of past portfolio investments. Investors should consider the content of this post in conjunction with investment fund quarterly reports, financial statements and other disclosures regarding the valuations and performance of the specific investments discussed herein. Unless otherwise noted, performance is unaudited.

DO NOT RELY ON ANY OPINIONS, PREDICTIONS, PROJECTIONS OR FORWARD-LOOKING STATEMENTS CONTAINED HEREIN. Certain information contained in this post constitutes “forward-looking statements” that are inherently unreliable and actual events or results may differ materially from those reflected or contemplated herein. Modular Capital does not make any assurance as to the accuracy of those predictions or forward-looking statements. Modular Capital expressly disclaims any obligation or undertaking to update or revise any such forward-looking statements. The views and opinions expressed herein are those of Modular Capital as of the date hereof and are subject to change based on prevailing market and economic conditions and will not be updated or supplemented. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in this blog are subject to change without notice and may differ or be contrary to opinions expressed by others.

EXTERNAL SOURCES. Certain information contained herein has been obtained from third-party sources. Although Modular Capital believes the information from such sources to be reliable, Modular Capital makes no representation as to its accuracy or completeness. This post may contain links to third-party websites (“External Sites”). The existence of any such link does not constitute an endorsement of such websites, the content of the websites, or the operators of the websites. These links are provided solely as a convenience to you and not as an endorsement by us of the content on such External Sites.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.