$AERO: The Base Liquidity Layer That Shouldn't Be This Cheap

Executive Summary

TL;DR: Aerodrome dominates Base with 10%+ TVL share, generates ~$190M annualized revenue at 100% fee distribution to veAERO holders, yet trades at a 2.1x revenue multiple while peers command 5-15x. With Coinbase backing, cross-chain expansion imminent and deflationary buybacks offsetting emissions, AERO offers asymmetric upside as Base's essential infra play.

Introduction

Many on CT love to claim they're "long infra" while aping into the latest L2 governance token with zero revenue share. With $AERO, you literally own the casino, or more precisely, the liquidity layer that every protocol on Base must use to function. Unlike the typical yield farms that pay you in their own inflationary shitcoin, Aerodrome returns 100% of trading fees to veAERO holders while programmatically buying back and burning tokens.

When it comes to PMF, Just look at the TVL explosion, from $120M to $2B+ on Base, with Aerodrome maintaining dominant market share throughout. Forget the FUD calling Base a mere Coinbase test run. Right after launch, cbBTC's volume on Aerodrome flipped WBTC's entire Ethereum mainnet volume in under a week. Protocol traction doesn't get much clearer.

Revenue & Value Accrual

Unlike many crypto projects where analyzing protocol revenue is meaningless because nothing flows to tokenholders, Aerodrome stands out by returning 100% of trading fees directly to veAERO holders. No equity backers extracting value. No opaque fee switches. No "figuring out tokenomics later”.

Current Metrics (January 2026):

- ◆Daily Trading Volume: $810M average (4-week rolling)

- ◆Annualized Revenue: ~$190M ($550K/day)

- ◆Market Cap: $380M

- ◆FDV: $760M

- ◆Revenue Multiple (MC): 2.1x

- ◆Revenue Multiple (FDV): 4.2x

As of recent data, Aerodrome generates approximately $3.7M in weekly fees, outpacing both Curve Finance and PancakeSwap despite operating with less than one-third of their TVL.

How Value Accrues to $AERO Holders

The ve(3,3) model creates a self-reinforcing flywheel where:

- ◆Trading fees (100%) go to veAERO holders

- ◆Protocols bribe veAERO voters to direct emissions to their pools

- ◆Emissions reward LPs, deepening liquidity

- ◆More liquidity = tighter spreads = more volume = more fees

In recent epochs, AERO token locks exceeded emissions by 7M+ tokens across five consecutive weeks, creating effective supply reduction despite the protocol's 11% annualized inflation. The Public Goods Fund has locked 1.84M AERO with total buybacks exceeding 150M tokens (~8% of supply).

Competitive Landscape

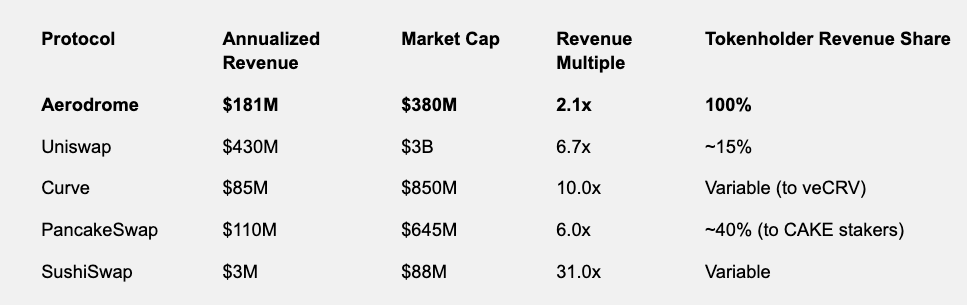

Perhaps most telling is what happens with revenue from the tokenholder perspective. Some projects like Uniswap used to pass fees only to LPs but not governance token holders until the fee switch. Others have dual equity/token structures where VCs capture most value. Aerodrome stands out and aligns value by returning the entire fee stream to participants who lock tokens for up to four years.

Here's how AERO stacks up against other Dexes:

Note: Revenue figures based on 30-day annualized data on DeFiLlama; multiples calculated against current market cap. (Data as of Jan 28, 2026)

At 2.1x trailing revenue, AERO trades at a discount to every major DEX competitor despite:

- ◆Its dominant ecosystem position on Base

- ◆100% fee distribution vs competitors' partial sharing

- ◆Superior capital efficiency

- ◆Institutional backing from Coinbase

The Monopoly on Base

Aerodrome launched August 2023 as Base's first native DEX and never looked back. Key dominance metrics:

Base Market Share:

- ◆15% of Base TVL ($600M+ of $4.9B total)

- ◆70%+ of Base DEX volume on peak days

- ◆Primary liquidity venue for all major Base pairs

Volume Achievements:

- ◆$340B cumulative volume since launch

- ◆When cbBTC launched, Aerodrome surpassed Ethereum mainnet WBTC volume in one week

- ◆Consistently processes $400-600M daily

Capital Efficiency:

- ◆Generated $4.6M in weekly fees with $600M TVL

- ◆Uniswap's largest pool does similar volume with 2x the TVL

- ◆Nearly 2x capital efficiency vs. established competitors

This isn't some temporary advantage. The first-mover moat on a new L2 is incredibly powerful. Uniswap’s advantage on Ethereum is a testament to that. Every new protocol on Base must bootstrap liquidity, and they all come to Aerodrome first because that's where the capital sits, the bribe market is liquid, and veAERO voters can make or break your TVL.

The Coinbase Advantage

Being Base's liquidity layer while Coinbase has 120M+ retail users and institutional clients is about as good as ecosystem alignment gets in crypto.

Strategic Positioning:

- ◆Coinbase Ventures owns substantial veAERO and actively votes

- ◆Direct voting on cbBTC emissions shows active governance participation

- ◆Base Ecosystem Fund acquired AERO specifically to guide protocol direction

- ◆Coinbase One membership rewards integrate AERO

- ◆Listed on both Coinbase and Robinhood (rare feat for defi tokens)

When institutional money eventually flows into Base defi (and it will with BlackRock’s BUIDL), they'll need liquidity infrastructure. Aerodrome is the pick-and-shovel play.

The regulatory angle matters too. While other DEX tokens can't get major exchange listings due to fee-sharing concerns, AERO sits on Coinbase and Robinhood. This is structural advantage from being aligned with the ecosystem that can navigate regulatory waters.

Technical Infra & Catalysts

Slipstream (Concentrated Liquidity):

- ◆10x faster execution vs. legacy AMMs

- ◆Tighter pricing and improved capital efficiency

- ◆Competitive with Uniswap v3 while maintaining ve(3,3) benefits

MetaDEX03 Upgrade (Q2 2026):

- ◆Target 3x increase in voter earnings

- ◆Dynamic yield optimization

- ◆Cross-chain swap functionality

- ◆Could significantly boost veAERO APRs

Cross-Chain Expansion:

- ◆Aerodrome + Velodrome merged under "Aero" umbrella

- ◆AERO holders receive 94.5% of new token supply

- ◆2026 roadmap includes deploying on Ethereum mainnet

- ◆Potential to bridge $80B+ in liquidity

Deflationary Mechanics:

- ◆150M+ tokens bought back and locked (~8% of supply)

- ◆Recent epochs: 7M+ net reduction in circulating supply

- ◆11% annual inflation offset by buybacks and organic locking

- ◆Compare to competitors with 15-30% perpetual inflation

The Bear Case

Concentrated Risk: If L2 narrative and Base fades, AERO fades as well. This is binary exposure to Coinbase's L2 strategy in line with INK by Kraken.

Price Action: Despite strong fundamentals, AERO is down 55% YoY like most defi tokens. The market clearly doesn't care about revenue multiples in current macro uncertainity.

Token Lock: Maximum value accrual requires 4 yr locks. That's an eternity in crypto. Opportunity cost is real, especially if alt season comes and you're stuck locked.

Competitive Threats: New forks launch weekly. The moat is network effects and first-mover advantage, not technological impossibility to replicate.

Smart Contract Risk: 2025 DNS hijacking showed infrastructure vulnerabilities. While token price held, it's a reminder that centralized components exist.

Valuation Scenarios

Bear Case (0.5x-1x): Base stalls, competing L2s win, Aerodrome loses market share → $0.25-$0.50

Base Case (2x-3x): Base maintains trajectory, Aerodrome holds market share, DeFi & broader altcoin sentiment normalizes → $1.20-$1.80

Bull Case (5x-8x): MetaDEX03 drives 3x earnings boost, cross-chain success, Base becomes the top L2 → $3.00-$4.80

Moon Case (10x+): Ethereum mainnet integration captures significant liquidity, Institutional defi adoption accelerates → $6.00+

Current price ($0.41 at the time of writing) implies market is pricing in something between bear and base case despite strong fundamentals. Either the market is cold cause of underperformance of altcoins or there's significant alpha in the base-to-bull scenario and smart money is accumulating.

Position Sizing & Risk Management

Conviction Level: High on fundamentals and timing

Recommended Allocation: 1-3% of crypto portfolio for risk-tolerant investors

Time Horizon: 6-12 months

Entry/Exit Strategy: DCA on weakness and partial exits during uptrend

Lock Strategy: Consider 4-year locks for revenue share

Red Flags to Exit:

- ◆Base TVL declining for 3+ consecutive months

- ◆Aerodrome Base DEX market share drops below 40%

- ◆Coinbase reduces veAERO holdings

- ◆Smart contract exploit or governance attack

Conclusion

At 2.1x revenue with 100% fee distribution to token holders, AERO is objectively cheap relative to crypto peers commanding 5-15x multiples. The protocol generates real cashflow, returns it to lockers, and maintains monopolistic market share on the fastest-growing L2 ecosystem backed by Coinbase.

The bet rests on Base's success, which creates concentrated risk but also concentrated upside. If you believe Base dominating L2 landscape (and Coinbase's distribution + institutional adoption suggests this is likely), then owning the liquidity layer at 2.1x revenue while competitors trade at 10x is a pennies on the dollar.

Ecosystem concentration, regulatory limitations and broader DeFi/altcoin skepticism reflects legitimate concerns. But for investors looking to accumulate long-term and can stomach volatility, the risk-reward skews heavily toward upside as the sentiment around altcoins is at all-time low.

My Take: This is buyside research, the combination of monopoly positioning, Coinbase alignment and valuation discount makes this one of the cleaner infrastructure plays in defi today.

Disclosure: Author holds AERO and may be biased. DYOR, NFA.

Price Target: $0.8-1.0 within 3 months (as market sentiment improves and altcoins perform)

$1.50-$3.00 within 18-24 months (base to bull case, Provided BTC crosses ATH)

Conviction: 7/10

Risk Level: High

Recommended Action: Accumulate on dips, lock for governance participation

Affiliate Disclosures

- •The author and/or others the author advises currently hold or plan to initiate an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

5

0