The Bull(et)ish Case for ZEX

What is ZEX? What’s the relationship between ZEX and Bullet?

ZEX is the native asset of Zeta Markets. Zeta Markets is a Perp DEX initially launched in 2021. Zeta was among the first to implement an on-chain Central Limit Order Book (CLOB) for options and perpetual futures on Solana.

However, building a CLOB exchange on Solana L1 came with challenges. While Solana is high-throughput, Zeta’s team encountered performance and UX limits during volatile market conditions. For instance, during sudden price swings, Solana’s network often became congested with bots, making it hard for normal users’ orders to get through. Fee spikes and unpredictable priority fees emerged as Solana introduced a fee market – market makers often had to overpay for priority to avoid getting “sniped,” and users paid fees on every order even if unfilled. 400ms block times on Solana, though fast for a blockchain, are still orders of magnitude slower than the sub-20ms latencies of top centralized exchanges, meaning on-chain price discovery lagged and arbitrage bots dominated volatile periods. These pain points – network congestion, fee uncertainty, latency limits, clunky UX, and scaling constraints – motivated Zeta to seek a new technical approach.

Bullet was conceived as the answer to the above challenges – a “DeFi trading layer” that extends Solana with dedicated capacity and advanced tech.

Bullet is a specialized Layer-2 rollup chain that runs a custom high-performance execution environment while relying on Solana’s Layer-1 for consensus, settlement, and data availability. This architecture lets Bullet operate with isolated blockspace and a tailor-made runtime for trading, yet still inherit Solana’s security (1000+ validators) and seamless access to Solana’s assets and ecosystem. The Bullet network is being incubated by the team behind Zeta Markets (a leading Solana perps exchange) in collaboration with Sovereign Labs. Its goal is to deliver an on-chain trading experience rivaling centralized exchanges in speed and throughput, without sacrificing security or transparency.

The team at Bullet has been building since 2021. The team size is about 15, with many engineers for HFT firms. The team raised funds from Jump, Electric Capital, Solana Ventures, DACM, Selini Capital, Anatoly, Mert and others. Tristan the founder said they have about 2 years of runway at the moment. Moreover, there is no equity entity generating revenue. Everything is planned to go toward the token, which is currently ZEX.

What does ZEX have to do with Bullet exactly? Well at the moment, the native asset of Bullet ($BULLET) hasn’t yet launched. This will happen after the Bullet mainnet launch, which is set to happen in early Q3 2025. When this happens, $ZEX will be migrated 1:1 to $BULLET. This means that there will be no additional dilution for users. Each ZEX token (circulating or not) will be migrated into a BULLET token. As a result, it is not widely known but ZEX is currently the native asset of the soon to be launched Bullet network.

If you’re willing to know more about Bullet’s tech, head over to the docs from the team that cover how the team thinks about the sequencer, nodes, wallet abstraction, bridging & more. This report will mainly cover tokenomics, valuation and why we believe ZEX is a good trade as we head into the second half of the year.

ZEX / BULLET Tokenomics

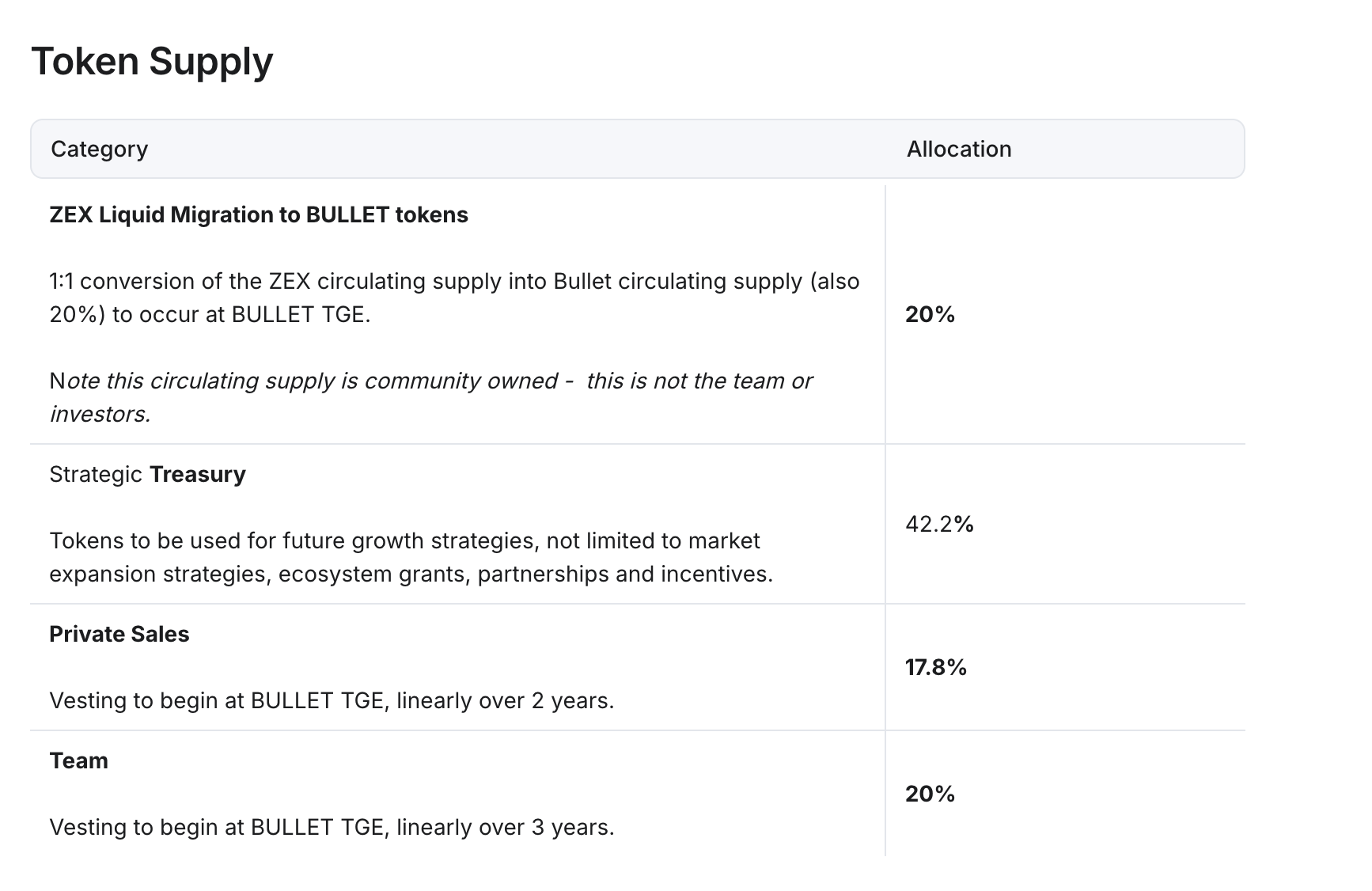

At the moment, only 20% of the total ZEX supply is circulating. The current marketcap is around $35mm, with the FDV sitting at $175mm.

About 42.2% of the supply is in a strategic treasury, which will be used for incentives. The team & investors own the other 37.8%, which will vest over respectfully 3 & 2 years starting at Bullet TGE. This was initially supposed to start vesting this week but the team & private investors agree to push back.

Given the team has 2 years runway, and they seem very much aligned with the Hyperliquid ethos, it’s hard to see them start selling aggressively as soon as their vesting starts. It’s hard to say what investors would do. The inflation on circulating supply from investors vesting would be about 44.5% in the first year (with 20% supply circulating, and a linear vesting of 17.8% of the supply over 2 years) and about 30% in the second year post TGE.

Nevertheless, there are reasons to believe this new sell pressure could be counterbalanced by a few dynamics:

- ◆Increased token sink. With the transition to its own network, and the migration from $ZEX to $BULLET, there is a lot more utility planned for the native token. This includes using $BULLET to pay for Gas Fees on the L2, for staking (nodes & users), as well as mechanisms similar to $BNB like trading fees discount.

- ◆Initial airdrop recipients gone and reduced sell pressure. $ZEX already went through 9 months of trading, hitting a low of sub 5mm mcap. Non-believers are likely out and the token is "only" sitting at $35mm marketcap at the moment.

- ◆Information asymmetry. As it stands I believe few people are aware of the fact that it has a native asset that is trading, and many see the Mcap / FDV as a no-go. This will become increasingly clear as we approach the Bullet TGE and on TGE.

- ◆Fee switch & buybacks. In his recent BidClub podcast Tristan the founder hinted at pushing for a fee switch in the same vein as Hyperliquid’s aggressive 97% buybacks (pending the insurance fund being capitalized enough). This will be voted on by ZEX token holders before the BULLET TGE. Needless to say that there is almost no doubt this will be accepted by the community.

Revenue projections, buybacks & valuation - The Value Trade

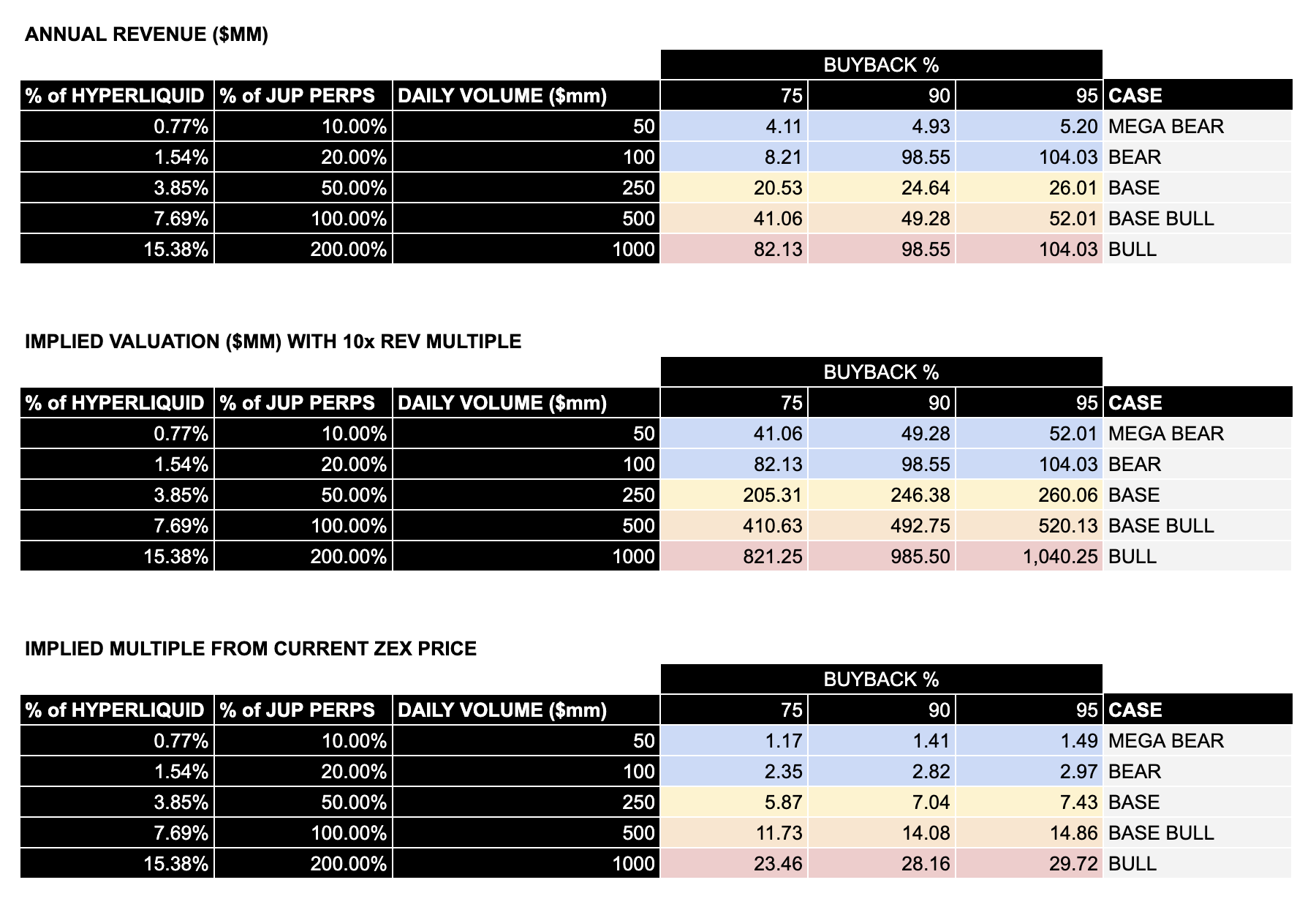

With the presence of a future fee switch, we can model some revenue projections and what it would mean for ZEX / BULLET valuation.

We take three main parameters:

- ◆Daily Volume, expressed in millions and as a % of Hyperliquid & Jupiter Perps average daily volume ($6.5bn and around $500mm respectively). This parameter ranges from $50mm (bear case) to $1bn (bull case).

- ◆% Buyback, ranging between 75% & 95%, given Tristan’s stance on being aggressive with it.

- ◆MCAP / REVENUE multiple. HYPE is currently around 15-20 but for $ZEX we will take a lower multiple of 10 only as it doesn’t have the statue of leader like HYPE + there is more supply overhand due to the investors’ portion.

- ◆Fees %. We use a 3 basis point (0.03%) fee parameter which is about below average for an exchange business.

Note that our revenue calculation & valuation multiple only focuses on the perps part of the product. Bullet will also launch with Spot trading & lending, but this is not accounted for in these calculations. These are the resulting calculations:

What can we see? $ZEX seems currently undervalued, even in the mega bear case (50mm daily volume & 75% buyback). In our base / base bull cases, we can see that the implied valuation of $ZEX should be between $250mm & $500mm marketcap which is about a 10x from current prices.

Of course, it’s very hard to predict what the volume will look like on Bullet’s mainnet. That being said, Tristan has mentioned that the team was in contact with the largest market makers on Solana and Binance, as well as large liquid funds looking to deploy more of their capital into a Solana ecosystem product versus Hyperliquid. Given Jup Perps volume, and the advertised efficiency of Bullet’s product, it wouldn’t be surprising to see the product have these types of volume if market conditions are good.

With the current renewed focus on Revenue generating protocols, and given the fact that there is no equity attached to the Bullet product (the token is the sole planned beneficiary here), we believe there is a value trade right there.

Relative Valuation - The Alt Trade

In crypto, relative valuation trades often happen. For example in 2020-2021 we witnessed how many DEXs got rerated following UNI’s airdrop and performance. CAKE, SUSHI, DODO & others all experienced 1000%+ increases in the span of a few months. Similarly, the ALT L1 played out later in the year with SOL, AVAX, ADA, NEAR & others.

Currently this hasn’t happened following HYPE’s TGE & run. This can likely be explained by hyperliquid’s current dominance. Nevertheless, we believe this has yet to happen with the launch of many alternative solutions in the coming quarters:

- @valhalla_defi

- @GTE_XYZ

- @nitro_dex

- @MonacoOnSei

- @hibachi_xyz

- @_bulktrade

- @FogoChain

Are all set to launch soon. With more liquid tokens and solutions, the competition will be greater for BULLET but this also means more attention, and potentially a re-rating to come similarly to how other sectors behaved in the past.

Moreover, even compared to current DEXs & L2s, the ZEX token feels relatively “cheap”. If we take back our previous revenue estimates, BULLET could potentially be among the top 3 L2 by revenue.

Yet, at its current $35mm marketcap, it would only be the 40th Layer 2 by valuation, far behind general purpose L2s like Blast, Polygon or SVM L2s like Sonic SVM or even app specific L2s like Aevo.

Compared to other DEXs, it still trades below Loopring, DODO, 0x, Bancor, Balancer and others.

To conclude this section, there seems to be a lot of ways to see the ZEX trade as a relative trade as well. ZEX still seems relatively cheap when compared to other Perp DEXs, other DEXs, or other L2s, especially given its revenue potential.

The Rebrand / Token Migration Trade

Yes, the transition from Zeta Market to Bullet and from ZEX to Bullet is more than a simple rebrand / 1:1 token migration, as the team rebuilt the entire product from the grounds up and switch from being an application on Solana to being a dedicated network extension with its own fees, nodes, staking and all. That being said, rebranding / token migration events often act as good enough trades in crypto.

The most fierce example, which also happens to be the closest from ZEX / BULLET, would be the Ribbon Finance rebrand into AEVO in early 2024.

Although this was widely communicated by the Ribbon team in its docs, similarly to the ZEX / BULLET trade, this took a long time to play out and the top wasn’t reached before after the migration happened. The RBN token proceeded to 10x in the meantime.

This is because attention hit an ATH on the day of the TGE & migration. Market participants were indeed not pricing in the event correctly and were minimizing the impact of exchanges supporting the migration, how many people had not anticipated / understood how the migration would happen, and the general hype around AEVO at the time.

Given ZEX current valuation, and the difference in following / attention between BulletXYZ and the ZEX token, this seems to be happening again. The migration will also only happen after Mainnet is live and stable. This should provide more time to refine the revenue expectation, multiples and what it means for ZEX & BULLET valuation.

The Risks

While ZEX seems like a good trade on many aspects, this is of course not a risk free trade:

- ◆Perps businesses are very sensitive to market conditions. Even more when they are novel untested products. If the market slows down significantly, all revenue expectations would be brought down.

- ◆Bullet’s strategy is to go head first into the Solana ecosystem and build around it, with prioritized listings for Solana assets for example. This could be detrimental if the SOL eco slows down in the future as the Hyper EVM / Mega ETH eco ramp up.

- ◆There are also many serious CLOB competitors looking to enter the market. TBD how Bullet will rank against solutions like GTE & others. There is also more competition from CEXs, and Hyperliquid itself will look to capture more market shares with things like HIP-3 and novel distribution from 3rd party apps (mobile apps, private trading etc…)

- ◆Sell pressure from Investors or miscalibrated incentives. The private investors allocation remains quite high compared to the current circulating supply. If there is not enough dynamics like buybacks or natural buy pressure from the market, the sell pressure could impact BULLET price negatively after TGE. Moreover, the team has not yet decided how they will distribute incentives. Tristan said he will want to go slowly there to attract real non mercenary users, but if the team does distribute too many incentives, the dilution could prove too high to sustain the price.

- ◆Execution risks. With mainnet launch + token migration + bridging etc… The team has been building with no exploit for 4 years, but given the amount of novelty implied with the launch of a dedicated network extension, execution risks remain high.

Despite the risks, we believe this is still a good trade as one of the only liquid exposure to bet on the CLOBs vertical (outside of $HYPE), with the potential for real revenue-generation and major catalysts (mainnet launch + fee switch + token migration) in the near future.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.