Marinade Finance

This is a discretionary long investment thesis on Mariande Finance. The opinions expressed are my own and not influenced by Outlier Ventures. This investment thesis does not constitute investment advice. Parts of this were written with the help of AI language models to improve clarity and save time. The thesis is written using publicly available, non-material information.

Written: July 22, 2025 | Published: Aug 7, 2025

Executive Summary

Marinade Finance is a non-custodial staking platform on Solana that enables users to earn staking rewards without operating their own validator. It offers three core products: Marinade Liquid, a liquid staking solution for use in DeFi while accruing rewards; Marinade Native, which provides secure, non-smart-contract staking directly from user wallets; and Marinade Select, an institutional-grade solution with compliance features and integrations for custodians and ETFs. Marinade enhances capital efficiency, decentralization, and accessibility for both retail and institutional participants in the Solana ecosystem.

Marinade is evolving into a more sustainable and value-aligned protocol through key proposals (MIP-4 to MIP-12) that embed MNDE into its core economics while driving TVL growth and revenue expansion. The introduction of a fixed 9.5% performance fee on gross staking yield (vs. ~2% under the prior bid-based model) creates predictable cash flows and is projected to generate ~$14.3M annually at current assumptions, a 33% increase over the old model. Revenue distribution (50% DAO Treasury, 40% MNDE buybacks, 10% MNDE-Enhanced Staking) hardwires demand for MNDE and strengthens its value accrual. Together with governance rights, performance-based staking rewards, and deflationary buybacks, this model creates a reinforcing flywheel: higher TVL → more revenue → sustained buy pressure and staking incentives → stronger MNDE utility, aligning protocol growth with tokenholder interests.

Institutional adoption represents a major growth lever for Marinade. Marinade Select offers a compliance-first staking solution tailored for custodians, funds, and ETF providers, combining curated validator sets, KYC onboarding, signed SLAs, and ongoing audits, all while preserving non-custodial control of assets. Its selection as the exclusive staking provider for Canary Capital’s proposed Solana ETF underscores rising institutional confidence and positions Marinade as a key gateway for regulated capital entering Solana. With dual coverage of both liquid staking (mSOL) and native staking, Marinade is strategically positioned to capture the majority of Solana’s staking market, where ~87% of SOL remains natively staked, while benefiting from the faster-growing LST segment projected to expand at 2% monthly. This two-pronged approach provides resilience, diversification, and a clear path to sustained TVL growth.

Valuation analysis reinforces MNDE’s asymmetric upside. Using a DCF model based on projected revenues from performance fees and institutional adoption, we estimate an enterprise value of ~$89M and an implied MNDE price of $0.2583 by 2027. A complementary revenue multiple approach, benchmarked against Solana (36.8x) and Jito (higher beta), supports a 20x FDV/Revenue multiple, yielding a price estimate of $0.2942. Both methods suggest significant appreciation from the current $0.1162 level, implying 122%-153% upside under base-case assumptions. These valuations reflect structural tailwinds, including predictable fee capture, institutional staking growth, and token buybacks driving deflationary pressure-while acknowledging market prices may deviate based on sentiment and liquidity cycles.

The investment thesis on MNDE depends on Marinade executing its growth levers effectively. Failure to scale institutional adoption via Marinade Select, maintain competitive positioning in liquid staking (mSOL), or introduce new utilities could undermine token value capture. Additionally, token buybacks must offset emissions from incentive programs and unlocks; if not, dilution could negate deflationary dynamics. While Marinade’s strong brand, DAO governance, and recent MIP proposals create a solid foundation, a lack of execution on these fronts or continued loss of market share to vertically integrated competitors like Jito would materially weaken the bull case.

Solana and Staking

Solana is a layer-1 blockchain designed to support decentralized applications at scale with very low transaction costs and high throughput. It achieves sub-second block times and can process thousands of transactions per second by combining an innovative consensus mechanism called Proof of History (PoH) with Proof of Stake (PoS).

Proof of Stake (PoS) is a blockchain consensus mechanism used to validate transactions and secure the network without the energy-intensive mining required in Proof of Work (PoW) systems. Instead of miners competing with computing power, PoS uses staked tokens as collateral to determine who produces blocks. This makes the process more energy-efficient and scalable.

Staking is essential for Solana because its security and consensus depend on PoS. Validators, who confirm transactions and produce blocks, must stake SOL tokens to participate. The more SOL a validator stakes, the higher their chances of earning rewards. This system makes it expensive for attackers to compromise the network, reducing the risk of Sybil attacks. Staking also aligns economic incentives: validators and those who delegate to them share in rewards from block production and transaction fees. Additionally, PoS relies on stake-weighted voting to finalize blocks, meaning more staked SOL translates to greater influence in maintaining network integrity.

A validator is a specialized node operator responsible for producing blocks, validating transactions, and maintaining consensus on Solana. Running a validator requires technical expertise, robust hardware, constant uptime, and a significant amount of staked SOL. Because these requirements create barriers for most users, many choose to delegate their SOL to professional validators. Delegation allows token holders to earn a share of staking rewards without operating a node themselves. This delegation model underpins Solana’s staking economy and creates the foundation for solutions like Marinade Finance, which simplify and improve participation.

Marinade Finance

Marinade Finance is a non-custodial staking platform on Solana that offers both native and liquid staking delegation. Instead of running your own validator, you can stake your SOL through Marinade and delegate it to a network of validators who help secure the Solana blockchain. In return, you earn staking rewards. To address different user needs, from DeFi participants to institutions, Marinade offers three core products: Marinade Liquid, Marinade Native, and Marinade Select.

Marinade Liquid: Marinade Liquid is Marinade’s liquid staking solution. Users deposit SOL and receive mSOL, a token representing their staked position. mSOL automatically accrues staking rewards while remaining fully liquid, allowing users to use it in Solana’s DeFi ecosystem for lending, trading, or providing liquidity. This product solves the traditional problem of locked capital in staking by enabling both yield generation and liquidity at the same time.

Marinade Native Staking: Marinade Native Staking allows users to delegate SOL directly to validators without receiving a liquid token. Unlike liquid staking, the staked SOL remains native in the user’s wallet and does not interact with smart contracts, reducing smart-contract risk. Marinade automates validator selection across a diverse set of nodes, ensuring decentralization and optimizing rewards. This option is ideal for users or institutions that prioritize security and simplicity over liquidity.

Marinade Select: Marinade Select is an enterprise-grade staking solution tailored for institutional clients, custodians, and funds. It provides custom validator delegation strategies, enhanced compliance (SOC 2 certification), and integrations with custodians like Fireblocks, BitGo, and Copper. Marinade Select is designed for large-scale staking with operational security, regulatory alignment, and optional integrations for ETFs and TradFi partners.

Marinade’s Stake Auction Marketplace (SAM): A Bond-Backed, Auction-Based Delegation Framework

The Stake Auction Marketplace (SAM) is Marinade’s dynamic delegation system that uses on-chain auctions to allocate stake based on validator performance and bidding. It serves as the primary mechanism for optimizing staker yield while maintaining network decentralization and validator accountability. This auction-based approach applies to both liquid staking (mSOL) and native staking, ensuring that delegation decisions are yield-aware and performance-driven.

SAM transforms Solana staking into a competitive marketplace where validators bid for stake by committing additional yield beyond base staking rewards. These commitments are backed by Protected Staking Rewards (PSR) bonds, which act as collateral to guarantee payment and enforce validator performance. As of SAM 2.0 (August 2024), 100% of Marinade’s TVL, including both mSOL and native stake, is distributed through SAM. This unified system also integrates MNDE-directed stake as a mechanism to influence validator stake caps, aligning governance incentives with the delegation strategy.

Every Solana epoch (approximately 2–3 days), Marinade evaluates validator bids, performance metrics, and decentralization constraints before rebalancing stake. Allocation is determined by a “max_yield” score, which represents the highest APY a validator is willing to offer (base rewards plus bid). However, validators typically pay only the realized_yield, which is the clearing price set by the last validator in the winning set. This means validators rarely pay their full max_yield; they only pay enough to match the realized_yield. For example, if a validator bids a max_yield of 10.6% and the auction clears at 8.12%, the validator pays only enough to reach 8.12%, not the full 10.6%.

Bidding is expressed in CPMPE (Cost Per Mile Per Epoch), a normalized metric that represents the maximum a validator is willing to pay per 1,000 SOL per epoch. This standardization enables fair comparison across validators. To participate, validators must fund a PSR bond large enough to cover one epoch of max_yield exposure, one epoch of bids at max CPMPE, and downtime penalties (calculated as 1 SOL per 10,000 SOL staked). These bond funds count as self-stake and cannot be withdrawn without exiting SAM.

From an economic perspective, validators earn base commission on inflation and MEV rewards, along with any external MEV opportunities. Their costs are primarily the bid payments deducted from their bond or rewards. Marinade also enforces an Auction Reputation system that tracks consistent participation and bid quality, influencing how much stake validators can receive in future epochs. Validators attempting to reduce their bid after receiving stake incur penalties through the Bid-Reduction Penalty mechanism.

For stakers, SAM delivers yield from two sources: base staking rewards (net of validator commission) and 50% of the realized bid amount, which is distributed to users as boosted APY. For instance, if the base yield is 7.5% and the realized bid contributes an additional 1.24%, stakers receive 0.62% from the bid while Marinade captures the remaining 0.62% as protocol revenue. Yield optimization occurs dynamically every epoch as the auction recalibrates allocations.

Under the current model, Marinade’s primary revenue stream comes from taking 50% of the realized bid flow. No fee is applied to base staking rewards or MEV. Revenue outcomes, therefore, depend on the average realized bid rate, total staked SOL allocated via SAM, and the clearing price rather than the highest bids. Additional features include last-price auction logic (which prevents overpayment), PSR bonds (which secure user funds), and stake matching programs (allowing validators to receive up to 30% matched stake for attracting external delegations). Decentralization constraints, such as caps by validator, country, and Autonomous System, further safeguard against stake concentration.

SAM matters because it creates a transparent, yield-maximizing environment for all stakeholders. For stakers, it delivers industry-leading APYs backed by performance guarantees. For validators, it provides a fair, competitive mechanism to attract large delegations without constant bid micromanagement. For Marinade, SAM represents a scalable and auction-driven revenue model that balances economic incentives with network decentralization.

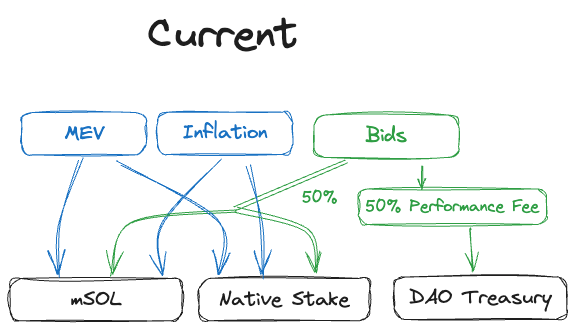

Current Revenue Model

The current flow of rewards under Marinade’s SAM model combines three yield sources, inflation, MEV, and validator bids, with only the bid component monetized for protocol revenue. As shown below, 50% of each validator’s bid is passed to stakers as extra APY, while the remaining 50% flows to the DAO treasury as a performance fee.

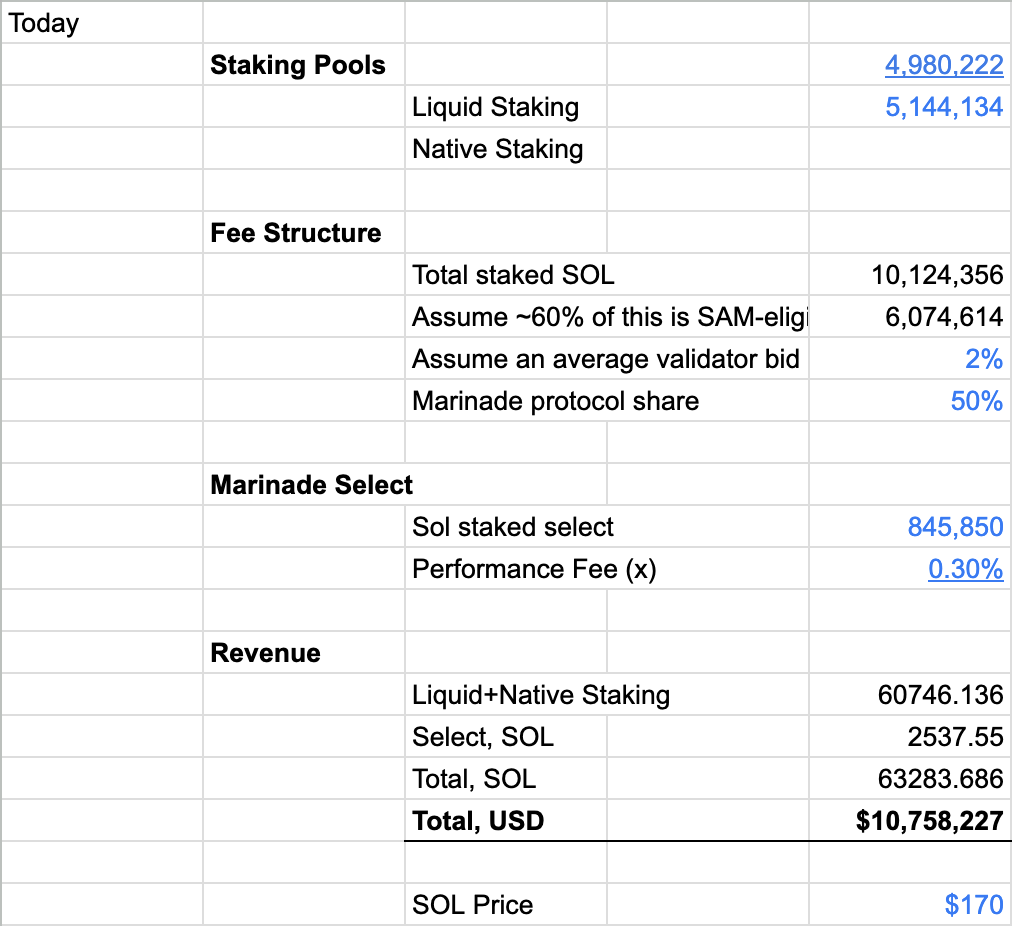

Marinade’s primary source of revenue is its Stake Auction Marketplace (SAM). The protocol’s secondary revenue stream comes from its Select SOL pool, which charges a 0.30% management fee on delegated stake. Unlike SAM, this pool provides a fixed, low-fee option for stakers who prefer predictable costs over auction-based optimization.

The figures above are approximate and intended solely for illustrative purposes. For this model, I’m using a conservative SOL price of $170, even though the current price is around $200, to account for potential volatility and better reflect an average annual price.

As the table shows, SAM generates the majority of Marinade’s revenue, contributing over $9.29M annually at current assumptions, compared to just $431,383 from the Select pool.

Recent developments

The DAO approved several strategic proposals in 2025 to strengthen Marinade’s growth, protocol resilience, and token utility.

MIP-4 (January 2025): Allocated 10.5M MNDE from the DAO treasury to fund research and development for Marinade, focusing on building an advanced unstake system, improving slashing resilience, optimizing stake management, and strengthening protocol security and efficiency to ensure long-term sustainability and growth.

MIP-6 (March 2025): Committed 21M MNDE from the DAO treasury for a 12-month 2025 marketing budget aimed at driving TVL growth, brand awareness, user education, and adoption through partnerships, paid campaigns, KOL engagement, and ecosystem advisory programs.

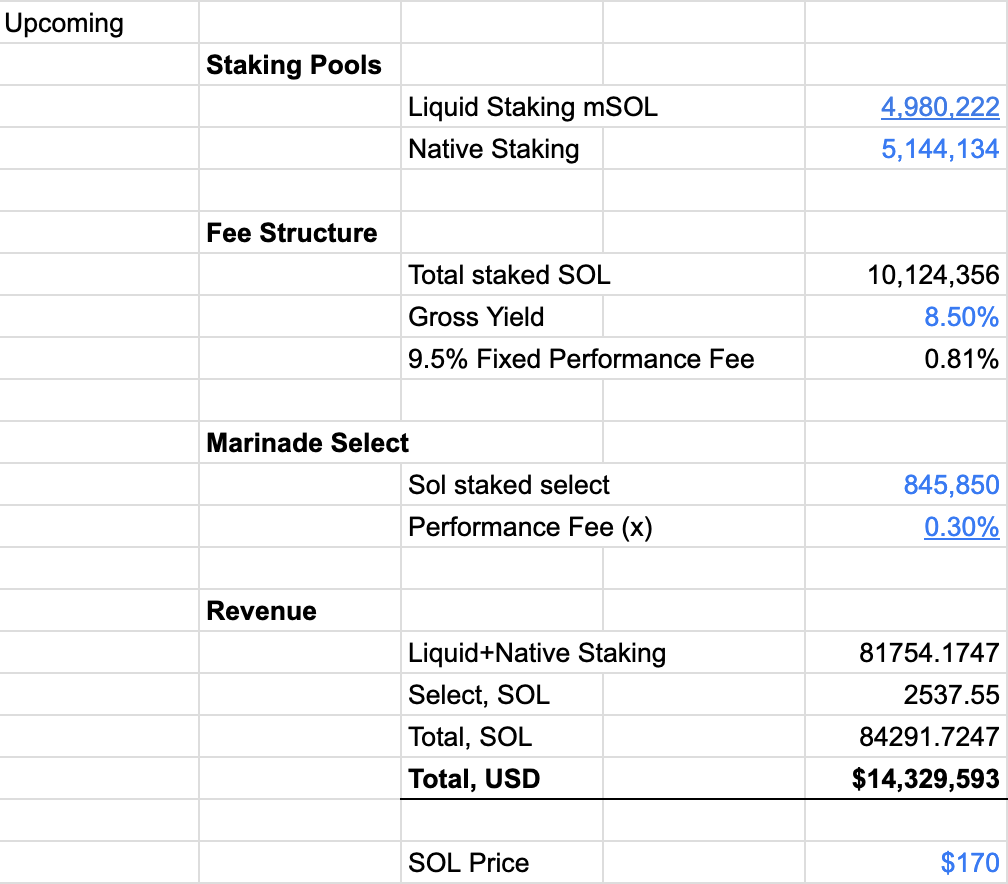

MIP-5 (January 2025): This proposal introduces a 9.5% global performance fee on staking yield (inflation, MEV, and bids) and allocates 10% of this fee to MNDE-Enhanced Staking participants, rewarding MNDE holders who stake and direct support to eligible validators in the SAM winning set. This creates tangible utility for MNDE and incentives for governance participation, while the remaining fee strengthens DAO resources.

MIP-7 (January 2025): 12.5M MNDE plus 10.7M unspent MNDE for Marinade Earn Season 4 to fund liquidity incentives for mSOL across DEXs, lending platforms, and DeFi integrations, reinforcing mSOL’s liquidity and competitiveness within Solana’s ecosystem.

MIP-11 (April 2025): This proposal redirects 40% of SAM performance fees to buy MNDE tokens from the open market, adding sustained buy pressure and strengthening MNDE’s utility alongside MNDE-Enhanced Staking.

MIP-12 (June 2025): This proposal requests 25M MNDE to incentivize migration of SOL stake to Marinade Native, targeting 2.5M SOL TVL growth. The budget is fully allocated as user rewards at 1 SOL = 10 MNDE, distributed after a minimum staking period (3 months for retail, 6 months for institutions) to ensure performance-based spending, with unused MNDE returned to the treasury.

The campaign includes:

- ◆Institutional Track (10M MNDE) leveraging partnerships like BitGo and ETF initiatives.

- ◆Retail Track (10M MNDE) for self-service migration with automated tools.

- ◆Custom Deals (5M MNDE) for large strategic prospects.

Given these recent proposals, Marinade is making meaningful progress toward aligning its business model with long-term sustainability and token value accrual. The protocol has introduced structural changes that not only diversify revenue streams but also hardwire MNDE utility into the core economics of staking on Solana. At the same time, growth-focused initiatives like MIP-6 and MIP-12 signal a strategy to expand TVL through institutional and retail channels, while maintaining competitiveness via liquidity programs (MIP-7). If executed effectively, these measures could create a self-reinforcing cycle: higher TVL drives revenue, revenue strengthens MNDE utility, and stronger MNDE economics incentivize deeper ecosystem participation.

MNDE Token

Marinade has a fixed supply cap of 1 billion MNDE. As of the end of Q1 2025, 430.4 million MNDE were in circulation, up from 386.4 million at the end of Q4 2024, marking a +11.4% QoQ increase.

MNDE is Marinade’s governance token, launched in October 2021 as a fair-launch asset with no ICO and a fixed supply cap of 1 billion tokens. On-chain DAO governance went live in April 2022 and migrated to Realms in July 2023, allowing MNDE holders to exercise direct control over treasury allocations, protocol upgrades, validator inclusion, and other critical decisions. MNDE minting is permanently disabled, ensuring a fixed supply, and token distribution is determined by DAO votes rather than a preset schedule.

The MNDE token plays a central role in Marinade’s ecosystem and governance. Following the passage of MIP-5 and MIP-11, MNDE now has three key utilities:

Governance & Protocol Control: The treasury tokens are under DAO control and allocated through governance proposals for initiatives such as R&D, marketing, TVL growth campaigns, and performance-based incentives. MNDE’s distribution strategy has shifted toward performance-based mechanisms tied to TVL growth and protocol contribution. For example, MIP-12 introduced migration incentives where users earn MNDE by moving SOL stake to Marinade Native. Core contributors do not receive time-based unlocks but instead follow milestone-based distributions linked to TVL objectives, reinforcing alignment between the team and protocol growth.

Staking Rewards via MNDE-Enhanced Staking: MNDE offers yield through MNDE-Enhanced Staking (MIP-5), where holders can stake tokens and direct support to validators participating in Marinade’s Stake Auction Marketplace (SAM). If their selected validators win auction slots, MNDE stakers earn a share of protocol revenue, specifically 10% of SAM performance fees.

Buybacks from Protocol Revenue: Under MIP-11, 40% of SAM performance fees are allocated to on-chain MNDE buybacks, reducing circulating supply, creating sustained buy pressure, and accumulating tokens into the DAO treasury.

Future Revenue

To illustrate the impact of the new fee structure:

If Marinade’s gross yield averages 8.5%, applying a 9.5% performance fee translates to approximately $14.329M annually at $170 per SOL, a 33% increase over the current ~$10.76M projection under the bid-based model.

This shift offers several advantages: greater predictability, a higher revenue base tied to aggregate yield, and improved alignment between protocol sustainability and staker incentives. It also reduces reliance on variable validator bids.

Risks remain as Marinade’s 9.5% performance fee under MIP-5 slightly reduces user net yields compared to pre-MIP-5 levels. This could create competitive pressure if other protocols promote higher nominal returns. However, Marinade’s yields remain strong relative to the broader market, typically in the 7.4%-7.6% range, because validators must bid more aggressively (often 8.5%+) to secure delegation through SAM. These dynamics ensure that users still receive competitive APYs despite the new fee structure. On the upside, SOL price appreciation, overall TVL growth, and increased validator competition in SAM can further amplify protocol revenue.

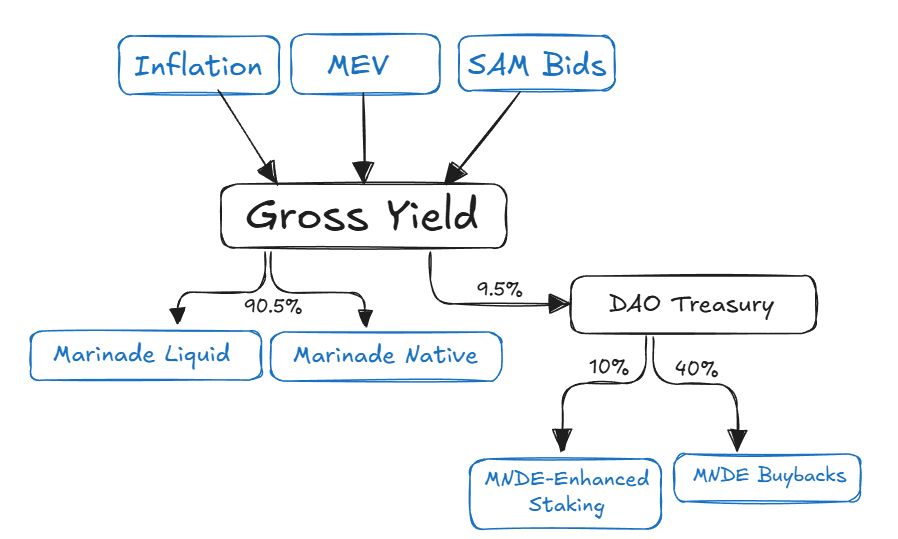

Following the new revenue model for Marinade Liquid and Native, the 9.5% performance fee will be extracted from gross yield, which includes all staking rewards generated from inflation, MEV, and validator bids.

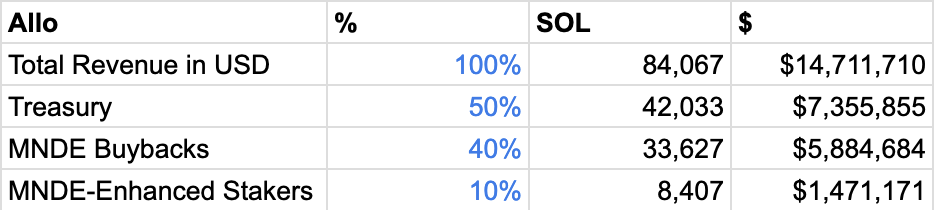

At the new revenue estimate of $14.329M annually:

- ◆50% ($7.35M) remains in the DAO Treasury for operations, growth, and reserves.

- ◆40% ($5.88M) of funds MNDE buybacks, creating sustained demand and reducing circulating supply.

- ◆10% ($1.47M) flows to MNDE-Enhanced Staking rewards, incentivizing governance participation and validator alignment.

This structure transforms MNDE from a governance-only token into a revenue-linked asset with built-in value capture and deflationary dynamics. Under the new model, 50% of Marinade’s performance fees are allocated to MNDE holders, 40% for token buybacks, and 10% for MNDE-Enhanced Staking rewards. At current projections, annual buybacks of $5.8M represent more than 10% of MNDE’s $50M market cap, creating recurring buy pressure while staking further reduces circulating supply.

These mechanisms create a reinforcing flywheel: higher Marinade TVL and SOL price → increased performance fees → larger buybacks and staking rewards → stronger MNDE demand and utility → deeper alignment between token holders and protocol growth.

The result is a token model where governance, economic participation, and protocol incentives converge, positioning MNDE as a governance token backed by protocol cash flows and designed to compound value as Marinade scales.

Institutional Focus

With regulatory frameworks maturing and staking gaining traction in mainstream finance, including its integration into ETF products, the stage is set for institutional capital to flow into Solana at scale.

Marinade Select offers a curated validator set that has undergone structured onboarding, KYC checks, signed agreements on uptime and security, and ongoing compliance reviews. This ensures that treasury managers, custodians, and institutional investors can stake with full transparency while maintaining non-custodial control of their assets. Funds remain in the user’s wallet at all times, staking rewards remain competitive, and validator quality is measurable and enforceable.

This approach is already gaining validation. Marinade Select has been named the exclusive staking provider for Canary Capital’s proposed Solana ETF, a milestone that signals growing institutional confidence in Marinade’s compliance and infrastructure standards.

Leadership reinforces this strategy. Marinade’s Chief Commercial Officer, Hadley Stern, brings deep expertise from traditional finance, having served as Managing Director and Global Head of Digital Asset Custody at BNY Mellon and previously founding Fidelity Digital Assets. This strengthens Marinade’s ability to align with institutional expectations, navigate regulatory landscapes.

As ETFs and custodians normalize staking in financial products, Marinade Select represents a growth avenue for TVL and revenue. Marinade is well-positioned to dominate institutional staking on Solana.

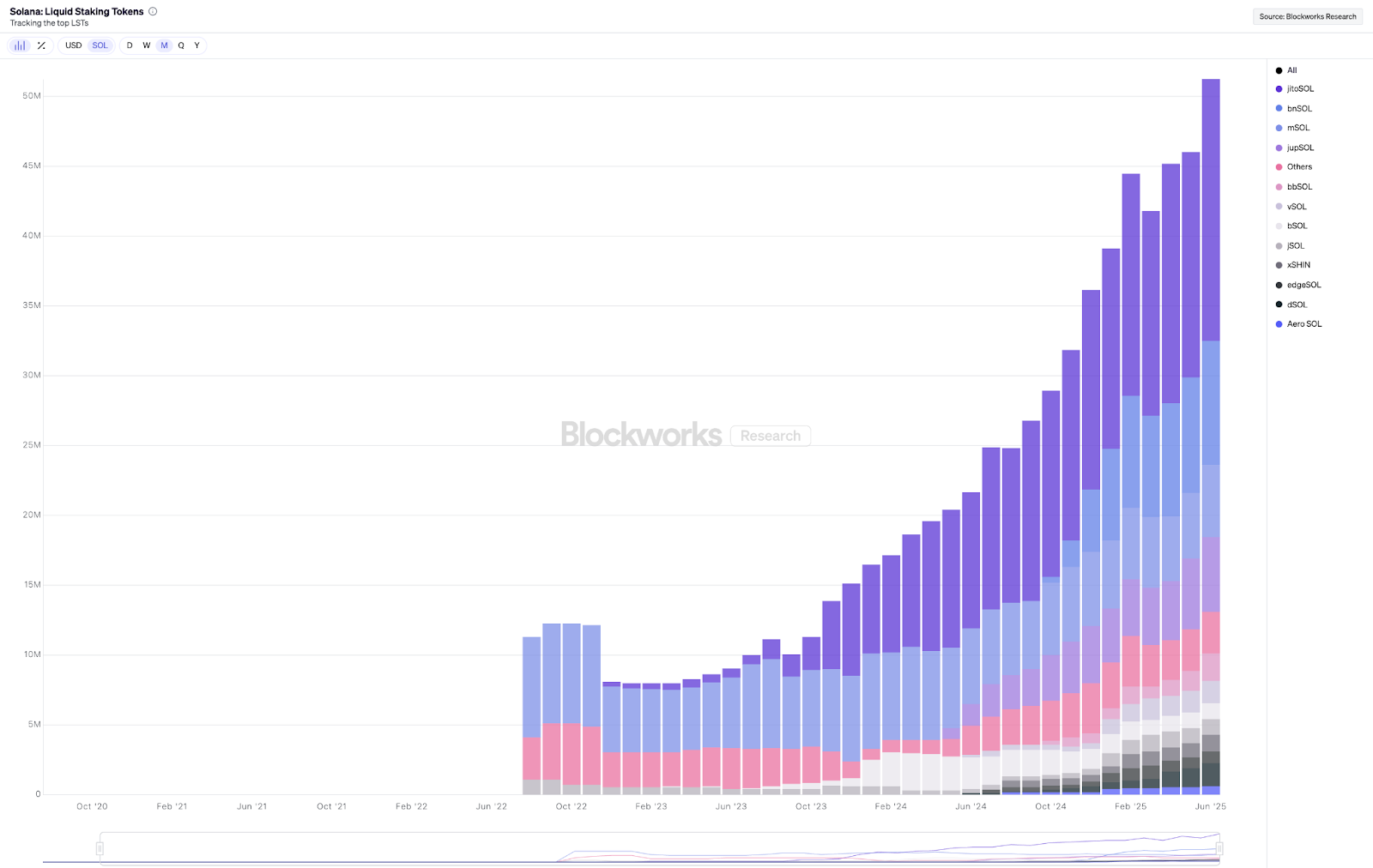

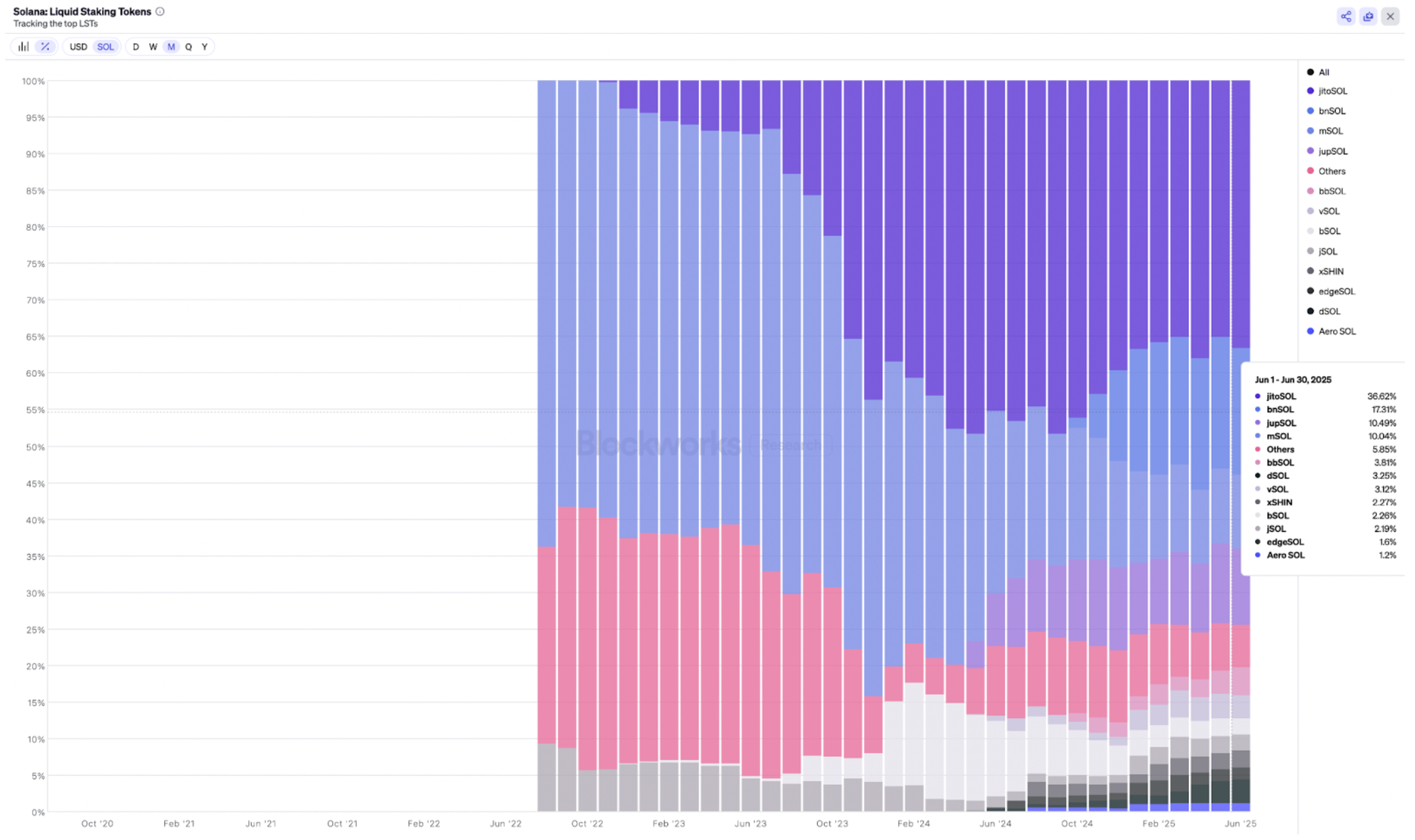

Another advantage for Marinade is its dual focus on native staking and liquid staking, which means it doesn’t rely solely on LST adoption to capture Solana’s staking upside. Out of the current 402.4M SOL staked on Solana, about 51.2M SOL (~12.7%) is staked via liquid staking tokens (LSTs), while the remaining 351.2M SOL (~87.3%) is staked natively. This highlights a massive opportunity for Marinade to grow across both segments: maintaining leadership in LSTs through mSOL and capturing a share of the much larger native staking market with Marinade Native.

Even though the liquid staking market has grown significantly over the past months, native staking still represents the vast majority of staked SOL. This makes Marinade’s strategy of serving both markets through mSOL for liquid staking and Marinade Native for custodial and institutional needs a logical and resilient approach.

The average monthly growth rate for liquid staking on Solana has been approximately 4.5%. For modeling purposes, we’ll apply a more conservative assumption of 2% monthly growth for liquid staking. Currently, native staking sits at 351.2M SOL. In total, approximately 75% of Solana’s circulating supply (538.04M SOL) is currently staked, which is a substantial share of the network. Given that the adoption curve for native staking is largely mature compared to the newer liquid staking segment, its growth potential is more limited. Therefore, we assume a modest 0.5% monthly growth rate for native staking when we run our Discounted Cash Flow model

Valuation Methods

To assess MNDE’s intrinsic value, we apply two complementary approaches designed to capture both cash flow potential and relative market positioning:

1. Discounted Cash Flow (DCF)

2. Revenue Multiple Valuation

Discounted Cash Flow - Valuation Method 1

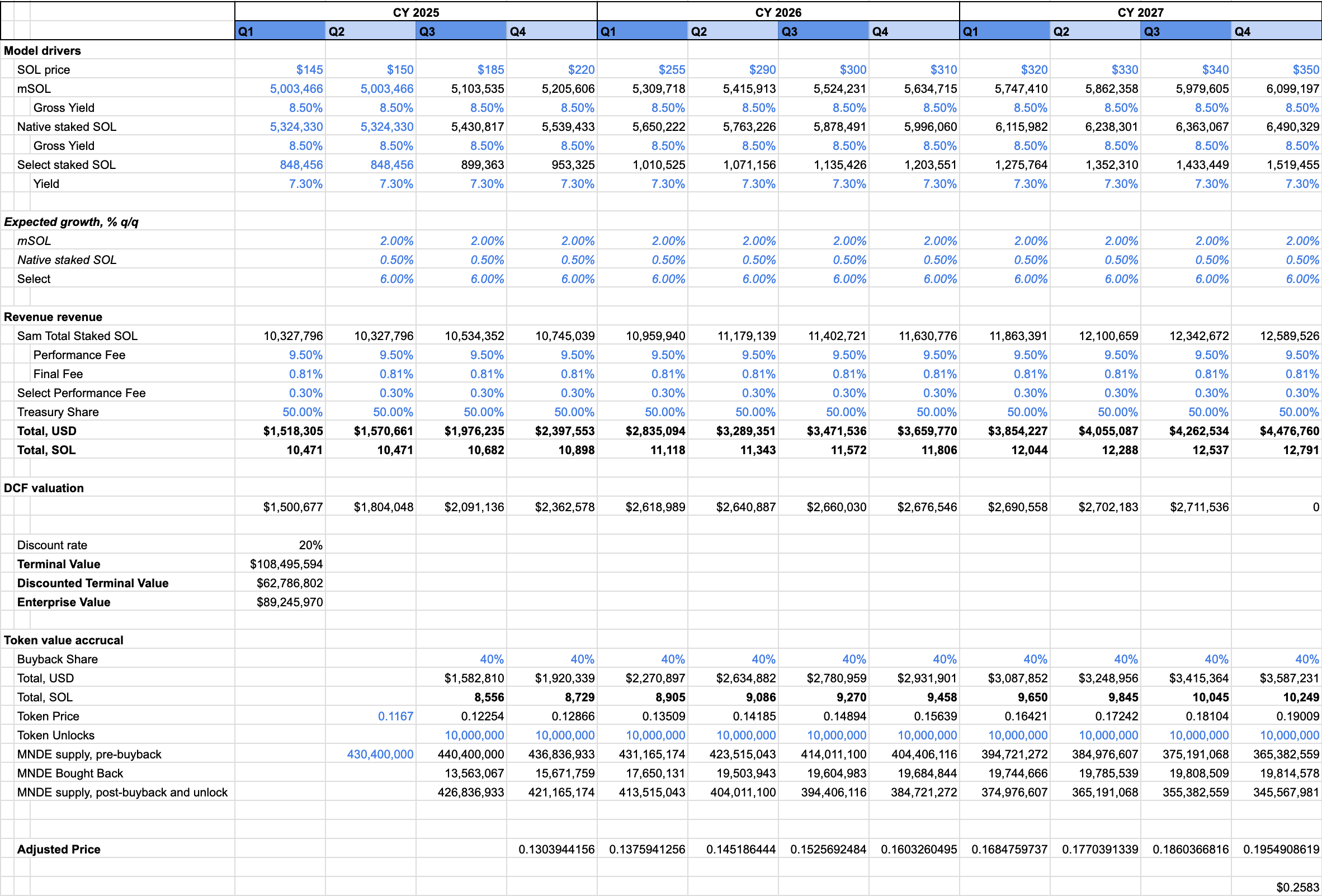

To estimate the intrinsic value of Marinade and its impact on MNDE, we modeled projected protocol revenues over a three-year horizon, applying a 20% discount rate and a terminal value assumption beyond 2027. Our base case assumes steady growth in mSOL adoption (2% QoQ), modest growth in native staking (0.5% QoQ), and 6% growth in Marinade Select due to institutional adoption. We incorporated Marinade’s 9.5% performance fee, 0.3% Select fee, and allocated 40% of revenues toward MNDE buybacks.

This model discounts quarterly cash flows and includes a terminal value to reflect long-term sustainability, resulting in an estimated enterprise value of $89.2M. Based on circulating supply dynamics, token buybacks, and a conservative 5% quarterly price appreciation, our analysis projects an adjusted MNDE price of $0.2583 by the end of the modeled period.

Revenue Multiple Valuation

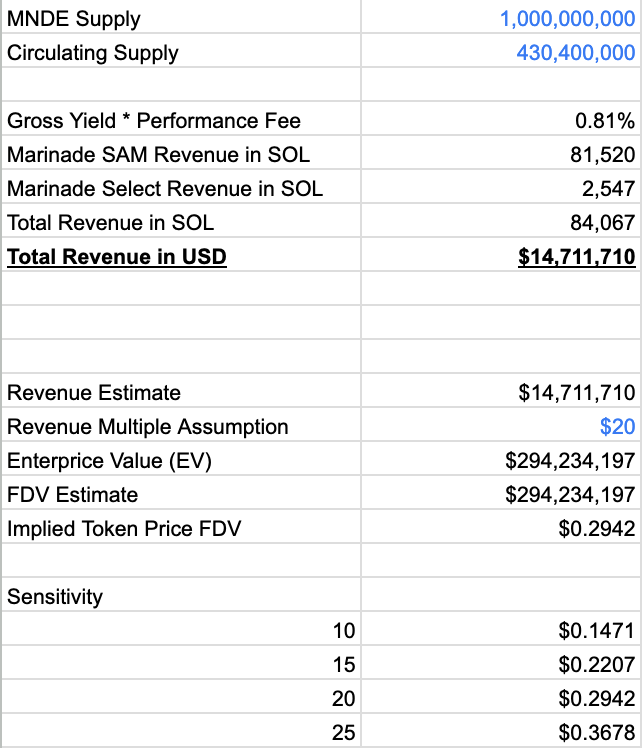

Taking inspiration from Multicoin Capital’s Jito Asset Report in evaluating Jito, this valuation follows a similar approach, but adapted to Marinade’s new revenue model. The goal is to estimate an implied MNDE token price using projected protocol revenues and applying a multiple reflective of high-growth staking infrastructure projects.

Marinade is currently trading at an 11.0x FDV/Revenue multiple, based on projected annual revenue of $10,758,227 and an FDV of $118M. For my valuation, I will use a 20x multiple, taking reference from Multicoin Capital’s estimates, according to their JTO Asset Report, “Solana currently trades at an FDV/Revenue ratio of 36.8x, and Jito, as a smaller, higher-beta asset, is likely to be ascribed an even higher multiple on LST-related revenues.”.

This model assumes Marinade sustains its TVL and benefits from structural tailwinds in staking:

- ◆Institutional adoption is driven by Marinade Select and custodial partnerships.

- ◆Growth in staking demand as staking becomes mainstream and integrated into ETFs.

- ◆Performance fee hardwiring post-MIP-5 ensures predictable revenue capture.

- ◆MNDE buybacks (MIP-11) and staking incentives create deflationary pressure and strengthen token utility to incentivize the usage of the platform.

- ◆Appreciation in SOL price enhances protocol revenue.

Under these conditions, MNDE’s value accrual mechanisms (buybacks + staking rewards) form a strong flywheel where protocol growth directly translates into token demand. I believe a conservative estimate for MNDE is a 20 multiple, which translates into a token price estimate between $0.2942 based on the model above.

While both models provide an intrinsic valuation framework, it’s important to acknowledge that token prices are rarely driven by fundamentals alone, especially in this market. Market sentiment, liquidity flows, and broader ecosystem narratives often amplify or suppress valuations significantly. Under our assumptions, both approaches converge within a similar range: the DCF model suggests $0.2583, while the revenue multiple method indicates $0.2942, excluding sensitivity scenarios. Compared to the current price of $0.1162, this implies an intrinsic upside of approximately 122%-153%. That said, actual market prices may diverge meaningfully, either higher or lower, depending on prevailing sentiment and tail risk.

When Will I Be Wrong About MNDE?

mSOL has lost market share in recent months, partly because I believe Marinade lacks the vertically integrated advantages of competitors like Jito (validator client and MEV layer) or Binance (exchange-driven network effects). To stay competitive, Marinade must evolve toward a self-reinforcing model where innovations across staking, validator relationships, and complementary products compound value. Combined with token buybacks, growing revenue, SOL ecosystem expansion, rising TVL, and institutional adoption, these levers can create a powerful feedback loop that drives long-term price appreciation.

My thesis breaks if Marinade fails to achieve meaningful growth in its institutional strategy through Marinade Select, or if token buybacks are insufficient to offset emissions from campaigns, token unlocks, and other dilution pressures. Additionally, if Marinade cannot drive further adoption of mSOL or introduce new utility and innovations, the token may fail to capture value despite broader ecosystem growth. While I believe Marinade’s established presence, strategic positioning, and recent MIP proposals set a strong foundation, the absence of these reinforcing mechanisms would invalidate my conviction.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.