$META: Futardio

Thesis

MetaDAO is a compelling liquid VC-style opportunity with limited downside and significant upside potential. It stands out as a category creator, the first ever implementation of futarchy uniquely enabled by crypto.

- ◆First ever implementation of futarchy, a concept that is somewhat niche but has an almost cultlike base of supporters, uniquely enabled by crypto. Hanson, the creator of futarchy theory, calls his idea “the one ring to rule them all.”

- ◆$META is a full-float token with FDV of ~$22M. Valuation seems especially attractive in context of current environment in crypto private markets. The token distribution is already relatively decentralized. Cap table includes Paradigm (invested in July 2024 with a cost basis of ~$550 with a ~15% stake), Colosseum, and a roster of high-quality Solana builders. In the near-term, I expect downside to be relatively protected by Paradigm halo + VC cost basis & narrative + adoption momentum.

- ◆$META has high upside potential due to its pioneering role in futarchy. Historically, projects that create/lead categories tend to trade at a premium given outsized attention and role as “meta leaders”.

- ◆The go-to-market is clear. Immediate addressable market includes “futarchy-as-a-service” for crypto projects, such as Drift (live), Save/Solend (recent partnership), and other Solana DAOs like Jito, Kamino, Tensor, etc. EVM is also on the roadmap.

- ◆Aside from DAOs, there are almost unlimited non-crypto verticals where MetaDAO could expand to, ranging from somewhat realistic (fantasy sports, e-sports) to moonshots (corporate activism, government policy). In an even more ambitious scenarios, AI agents could enhance futarchy by analyzing vast datasets with sophisticated models, improving prediction markets and potentially leading to more accurate, high-quality decision-making in areas like corporate activism and government policy.

- ◆It is important to note that the DAO’s mission is driving $META price appreciation above all else. In fact, they have pivoted product lines multiple times. Therefore, while futarchy-as-a-service (FaaS) is an interesting and promising direction for the DAO, an investment in the token does not necessarily underwrite success of FaaS. Instead, it underwrites the ability of the DAO to adapt and execute whatever opportunities that translate to a higher $META price, via futarchy governance process. The ideal endgame is a tireless, autonomous organization relentlessly pursuing sustainable price appreciation above all else.

- ◆Finally, as I note later below, $META benefits from the tailwind of the growth of prediction markets and event-betting as well as continued growth of Solana’s ecosystem.

Before diving deeper, I acknowledge the several constraints to this pitch for some readers. It’s a small-cap and highly illiquid token, TAM/monetization/business model is anyone’s guess, could be a failed experiment, may take years to realize potential, the list goes on. Nonetheless, I pitch it to readers both to highlight a genuinely innovative crypto experiment that is still relatively under-the-radar and as well as a longer-term liquid VC style investment in an underlooked category that some may be looking for😊

Introduction to MetaDAO

MetaDAO is a project that pushes the boundaries of cryptoeconomics in governance. It is the first practical implementation of futarchy, a governance structure that uses market forces to determine policy implementation. MetaDAO itself is a DAO responsible for developing futarchy markets and uses $META as its reference asset.

MetaDAO raised a $2.2M round in August 2024 led by Paradigm and a roster of angel investors, most of whom are builders in the Solana ecosystem. $META started relatively decentralized, initially bootstrapped via airdrop and capped pre-sale. The token is fully floated, with an estimated 20,198 tokens circulating and 687 tokens in the DAO treasury and multisig.

Historical market cap of $META:

Futarchy Primer

To provide context, let me briefly introduce futarchy. Futarchy, introduced by Robin Hanson in 2000 in his working paper "Shall We Vote on Values, But Bet on Beliefs?", proposes using prediction markets to drive decision-making in organizations. While implementation details can vary, the futarchy process broadly follows these steps:

- ◆Participants first agree on a set of key performance indicators (KPIs) to maximize. For a country, these might include GDP, life expectancy, and environmental quality. For a company, it could be share price or relative share price performance against an index. For DAOs, it could simply be token price.

- ◆A proposal is submitted to address a specific issue or opportunity.

- ◆Two prediction markets are created for the proposal, a pass market and a fail market. Each market trades separately.

- ◆After a certain period of trading, the two markets should provide market information. The proposal passes if market agents believe it would increase the value of the token. Otherwise, it fails.

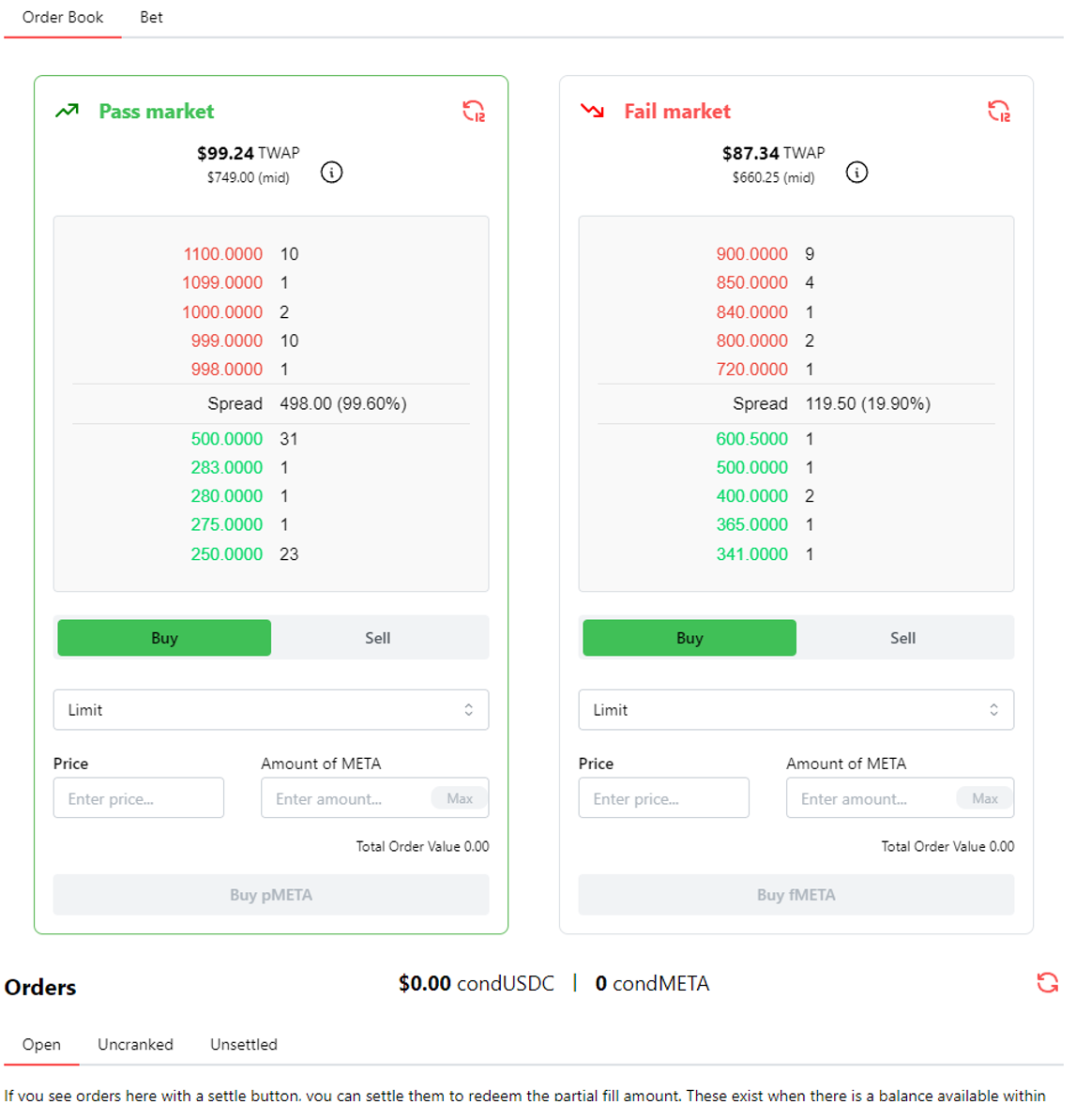

MetaDAO implements futarchy through conditional vaults. Each proposal has a conditional market where trades are settled only if the proposed action is taken. For example, trades in the pass market only clear if the proposal passes and are reverted otherwise. The same applies to fail markets. Each proposal includes Solana Virtual Machine (SVM) instructions that are executed if the proposal passes.

Example of pass/fail market on MetaDAO:

A Theoretical Example

Imagine Lido DAO is considering a decision to distribute 80% of revenues to tokenholders. All $LDO tokenholders have three days to vote on this proposal. If the proposal passes, distribution is automatically activated.

As a $LDO tokenholder, you might believe that if the rev share is turned on, the value of $LDO will rise to $2. But if not, you think $LDO will only be worth $0.50. To take advantage of this, you could buy $LDO in a market that assumes the proposal will pass, betting that the price will go up to $2. At the same time, you might sell $LDO in a market that assumes the proposal will fail, betting that the price will drop to $0.50. If the proposal passes, you’ll profit from your bet that the price will go up. If it fails, you’ll profit from your bet that the price will go down.

However, other $LDO holders might disagree with you. They might think it’s too risky to turn on the rev share right now, fearing it could attract negative attention from regulators. If most people believe this, they might sell their $LDO in the market where the proposal is expected to pass and buy in the market where it is expected to fail. This collective action will influence whether the proposal passes or fails. Overall, market forces should elicit the correct response.

Practical Examples

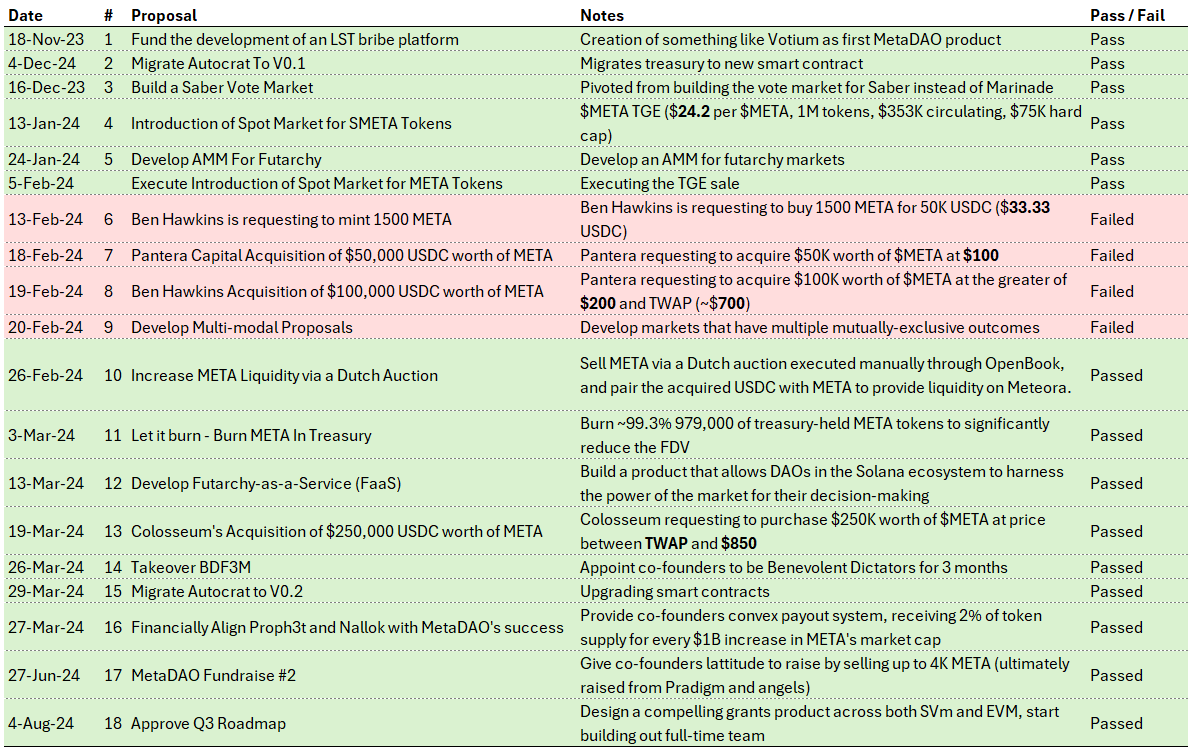

Now consider real examples from MetaDAO’s track record. The DAO once had 99K tokens in its treasury for future expenditures. However, the low-float, high-FDV dynamic deterred market participants from buying $META and participating in the DAO. And, as some members noted, it could also encourage the use of $META for expenses, increasing potential selling pressure.

Therefore, a proposal went up to vote on burning all the treasury-held $META, which voted through. In retrospect, this decision likely value-accretive. Yet, the co-founders themselves admittedly did not want this proposal to pass. And its hard to imagine any other DAO to push a vote like this through.

Current Traction

A table of prior proposals and outcomes are presented below. Interestingly, DAO has repeatedly rejected unfavorable dilution of the token price while approving initiatives that have likely drove recent price appreciation – such as token burning, bringing in Colosseum and Paradigm, aligning co-founder incentives, etc.

High-quality team and community. Due to the bootstrapped nature of $META, along with financialized governance, the DAO has cultivated a highly engaged community. Contentious proposals like Proposal #7 (Pantera acquiring $50K of $META) will have community members ape 6-7 figs into “Fail” market to express their opinions. Founders proph3t and Kollan House are cryptonative with a strong network within the Solana community. Their incentives are also aligned due to Proposal #16. A $5B+ valuation outcome for $META results in a $500M payout.

Catalysts

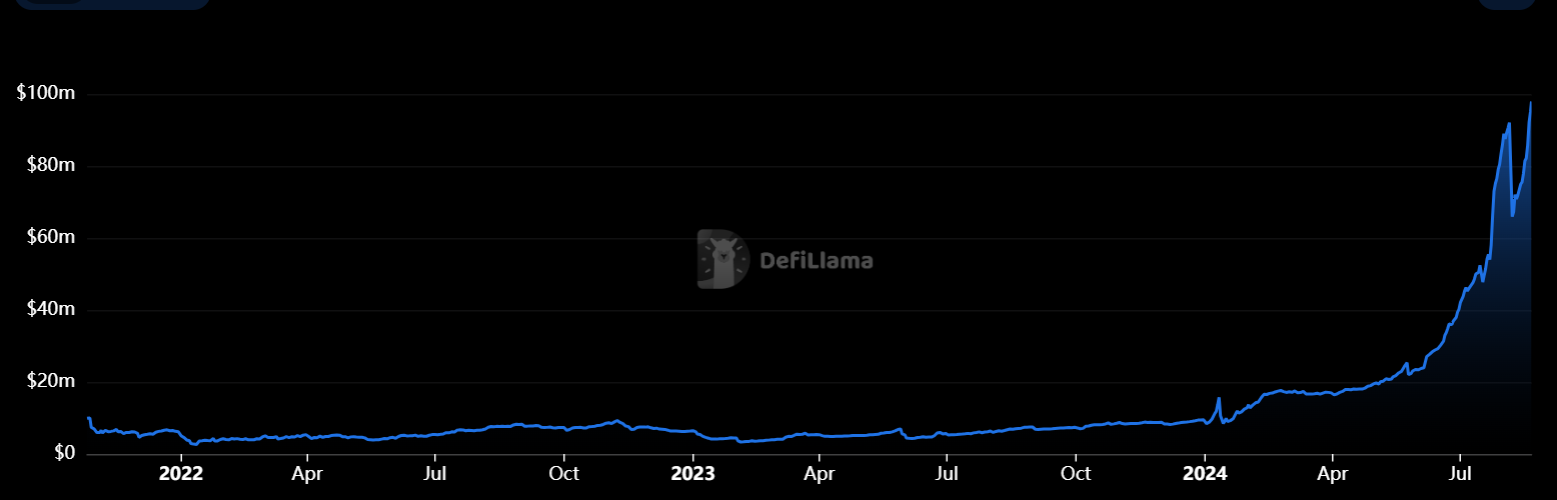

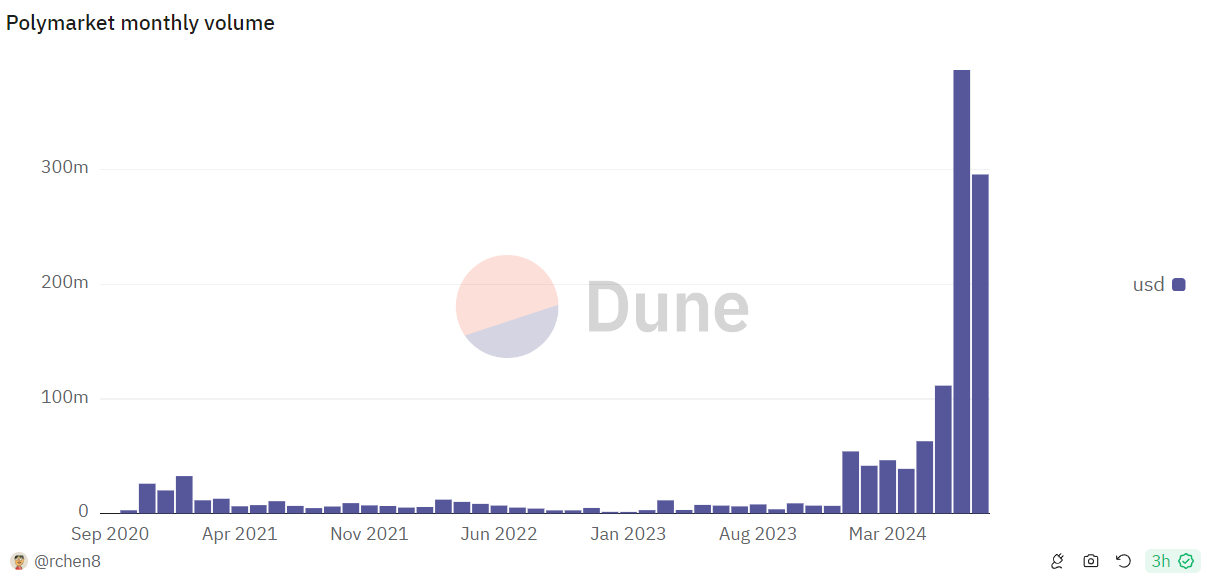

Tailwind of prediction markets and event-betting. MetaDAO benefits from the growth of prediction markets. Proph3t, MetaDAO’s co-founder, shared that Polymarket’s increasing adoption in mainstream circles gave them a boost during fundraising conversations. "If we see Polymarket as a machine, then it made sense to me that we’d want to use a truth machine to make decisions."

Polymarket TVL

Even after the U.S. election, prediction markets will likely continue to grow through the cycle. Adjacent verticals, online gambling and sports betting, are also secular growers. While MetaDAO is not directly a prediction market, it nonetheless benefits from the increasing awareness of the utility of prediction markets and financialization of events/decisions.

Next wave of Solana protocols. We’re seeing a wave of Solana protocols decentralizing, most recently with Jito, Drift, Jupiter, and Kamino, and in future with a whole spate of new Solana projects. These are all immediate addressable markets for MetaDAO, and also helps give $META “Solana beta.”

Risks

- ◆Futarchy is unproven, and multiple unforeseen issues could arise:

- ◆Market manipulation

- ◆Inactive governance

- ◆Entity or group of entities buy votes or corner the $META token

- ◆Exploited / outmanuevered via game theory

- ◆As with all liquid VC type bets, you’re betting on the power law here where small chance very high upside is compelling enough to risk the investment going to zero.

- ◆Token price could go sideways while FaaS does not take off and the DAO takes some time to pivot to a new direction, incurring capital costs.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.

0

0