VRTX: The Perp DEX Outearning Its Own MC

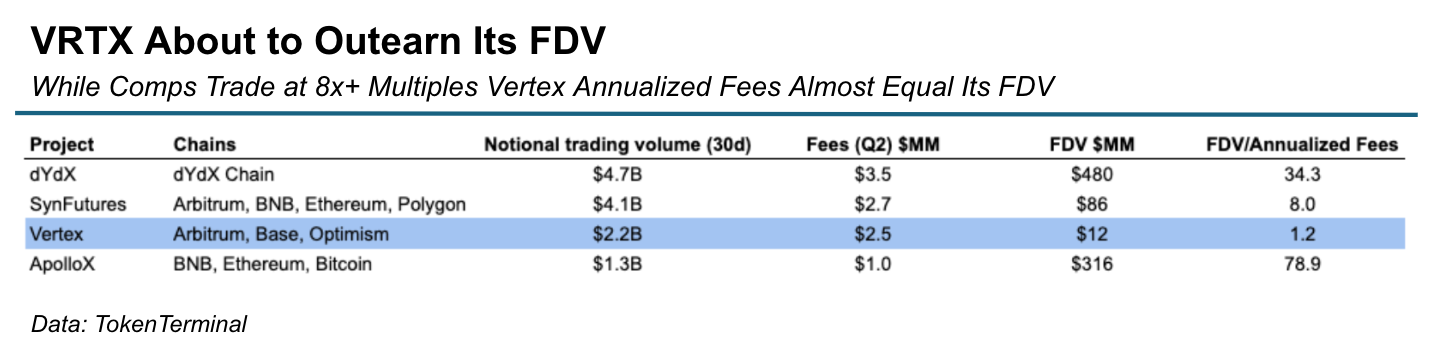

Thesis: Vertex is a top 11 perp DEX with $2.3B monthly volume (June ‘25) and $10MM annualized fees. While comps with similar volume trade at $88MM (Synfutures) and $300MM (ApolloX) FDV Vertex only trades at $11MM FDV ($6M MC). VRTX is outearning its MC!

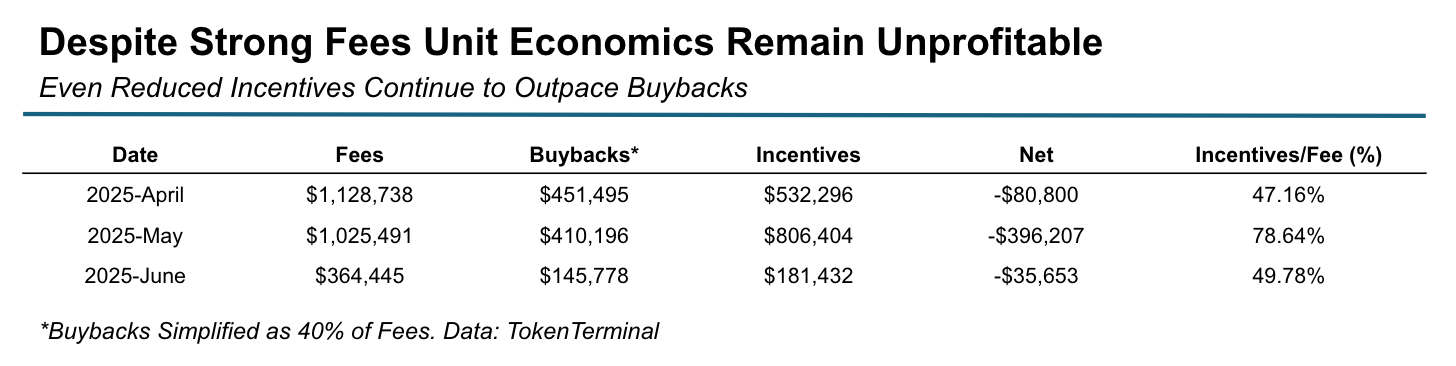

Despite an attractive Fees/FDV ratio, VRTX has been a value trap for months. The primary reason are VRTX’s trading incentives. 75% of the native token incentives accrue to market makers which seem to dump them into the chart. While incentives already got dialed down significantly in Feb ‘25 they continue to outpace buybacks (math below).

Why now? VRTX sits in a compelling category: liquid tokens with real fundamentals trading at sub-seed valuations. Similar to DRV trading at $12M MC in April, VRTX promises venture-style upside derisked by strong traction. The CLOB-wars are on and VRTX boasts a strong team with an edge in overcoming the liquidity cold start problem. Bullet’s $ZEX 320% surge signals market appetite for bidding on underdogs joining the race.

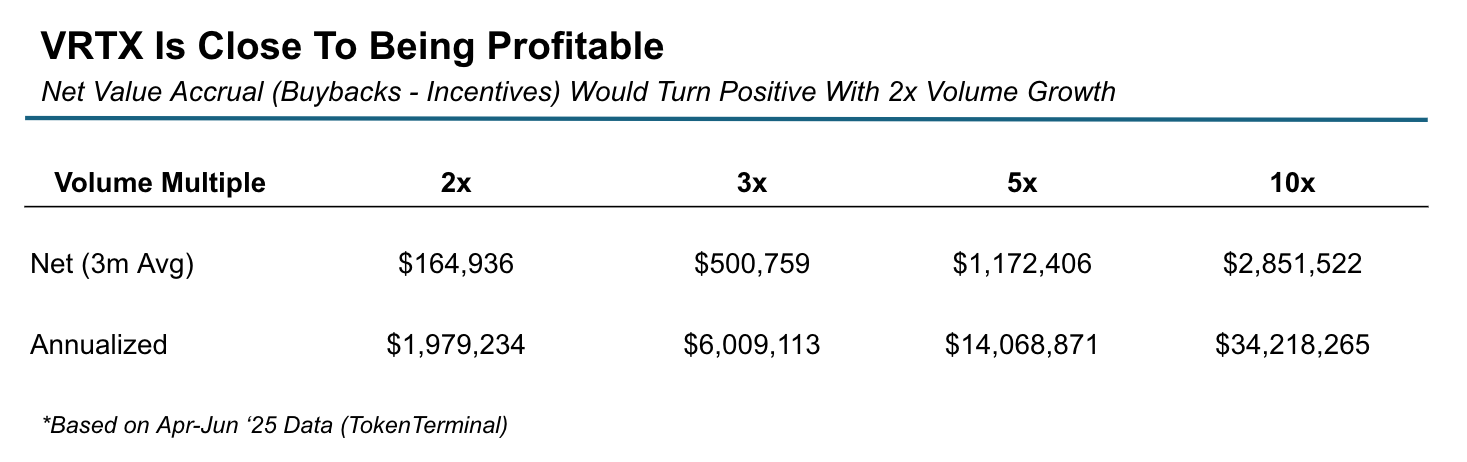

The path to incentive-adjusted profitability is within reach. If volumes double, Vertex flips into net positive value accrual. At 3x current volume, annualized net value to token holders would already exceed the current MC. The product is live, volumes are solid, and the team is shipping. One meaningful catalyst - whether a product launch, revamped incentives, a strategic listing, or a key partnership - could trigger an explosive rerating. For those comfortable operating at the frontier with high risk and limited liquidity, this may be one of the most asymmetric bets in crypto right now.

Of course punting on the frontier is risky. As always, this is not financial advice and DYOR.

Product Overview

Vertex is a vertically integrated DEX that combines spot trading, perpetual futures, and a money market into a single unified platform. It features a hybrid model of a central limit order book (CLOB) and an automated market maker (AMM), enhancing liquidity as positions from LP markets are integrated into the order book.

Key Differentiation: Vertex Edge

The Vertex Trading product described above is a standard perp DEX. Vertex Edge, a custom EVM implementation of an off chain orderbook, functions as a liquidity-as-a-service layer for various chains. Liquidity from Chain A can be used to settle a trade on a Vertex instance of Chain B. Independent orders from one chain are matched against liquidity from multiple chains.

Comps

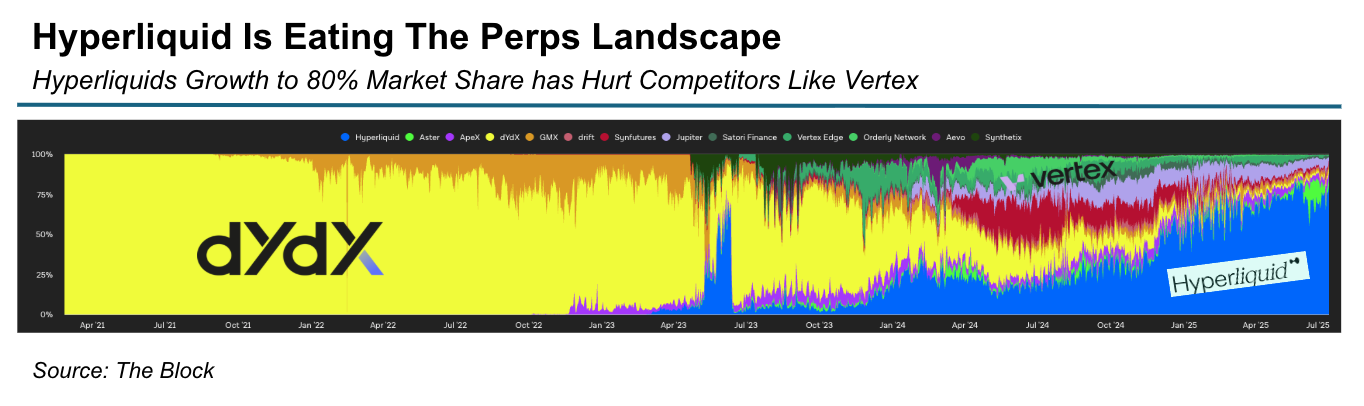

Hyperliquid is rapidly consolidating the perp DEX market, now commanding ~ 80% market share. In late 2023, Vertex held a third of all perp volume - but as Hyperliquid’s rise accelerated, Vertex’s share compressed to just ~1% today.

Despite this shift, the perp DEX market remains active and lucrative. CLOB wars are heating up, with new entrants vying for attention - but existing players still generate substantial fees. Among peers with comparable trading volume, Vertex stands out as a deep value play.

Competitors like ApolloX and SynFutures trade at 8–79x fee multiples, while Vertex is on the verge of outearning its entire FDV.

Tokenomics

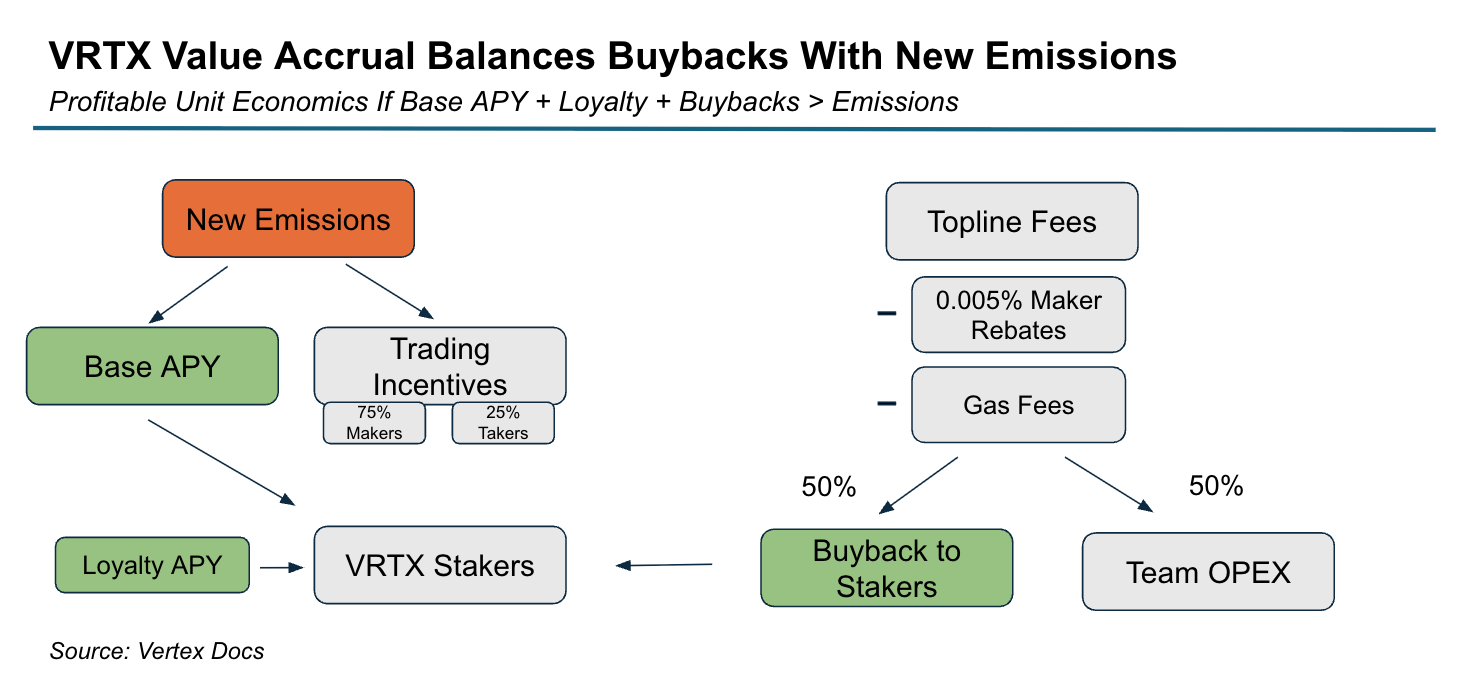

Vertex runs on a competitive 2bps taker fee across all markets, paired with a -0.005% maker rebate.

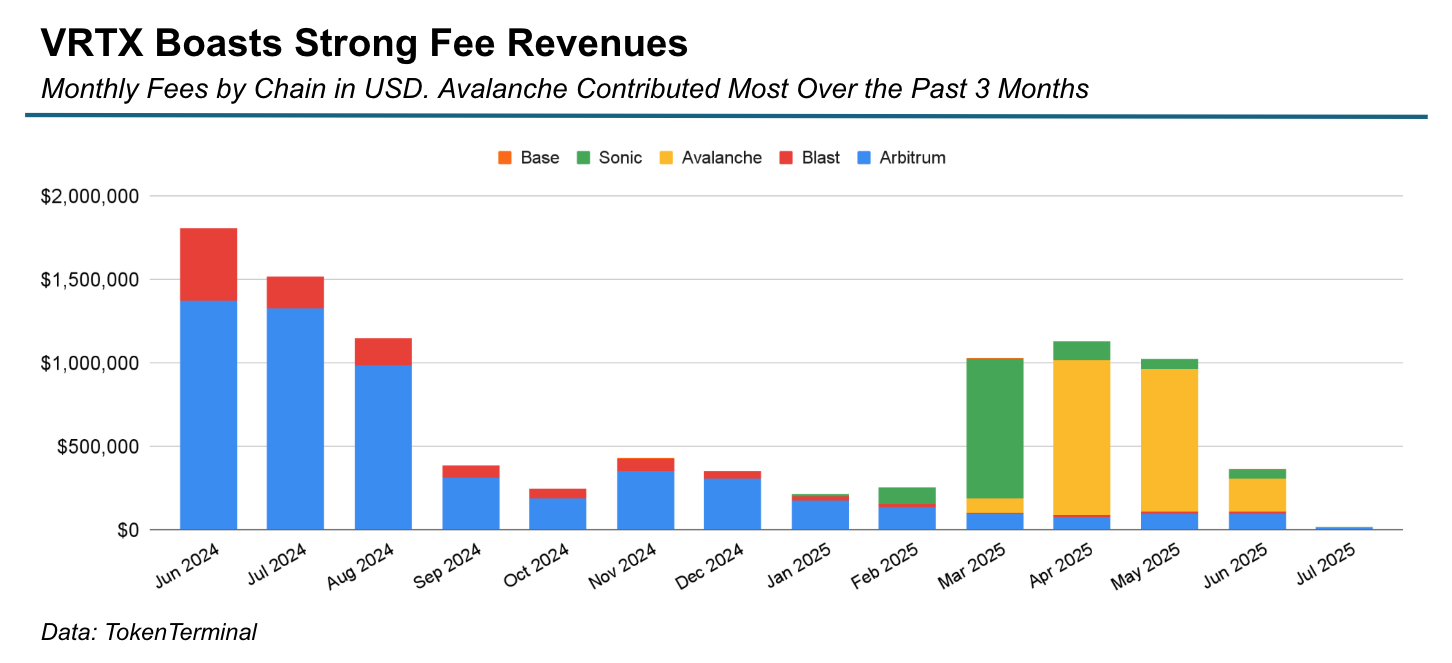

Net fees - after accounting for rebates and gas costs - are split 50/50 between protocol buybacks (to stakers) and the team. This creates a solid base for value accrual as buybacks scale with topline fees.

However, emissions - in the form of trading incentives - continue to weigh heavily on token performance. These incentives, while critical for attracting market makers and bootstrapping liquidity, have become a structural source of sell pressure. In effect, VRTX emissions are subsidizing volume at the expense of price - a dynamic that’s likely contributed to the token's 90%+ drawdown over the past year.

Reductions of emissions in Feb ‘25 were meaningful - but not enough. Under a simplified model where buybacks equal 40% of gross fees, incentives still outpace value returned to holders in recent months. Notably, this does not include Base APY (≈15%) and Loyalty APY (funded via early unstaking penalties), which add some value back to stakers, but are unlikely to materially change the unprofitable structure under current conditions.

Risk Reward

While emissions continue to exert structural sell pressure, the path to profitability is in sight. If volumes double, Vertex flips into net positive value accrual. At 3x current volume, annualized net value to token holders would already exceed the current MC. [Note: Figures are USD denominated based on historical data; Incentives increase with token price]

A single meaningful catalyst - whether it’s a product launch, new incentive structure, key partnership or a strategic listing - could trigger a significant market rerating.

This upside has its price tag. If token price continues to grind lower, the protocol risks hitting a breaking point. Market makers may abandon VRTX, sparking a vicious cycle of worsening liquidity and declining volume. At valuations around $10M, however, the token becomes increasingly attractive to long-term, venture-style investors who can absorb MM sell pressure and bet on a turnaround. The VRTX team has demonstrated its ability to ship and the pressure is on to deliver again.

The recent $ZEX rally showed how fast the market can rotate into fundamentally solid, overlooked perp DEXs. VRTX offers similar, if not higher, upside potential - but at the edge of the risk curve, with real execution dependency and liquidity constraints. For those comfortable operating at the frontier, this may be one of the most asymmetric bets in crypto right now.

(Any views expressed here are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions. Maelstrom Fund and associated individuals may hold positions in the assets discussed in this article.)

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.