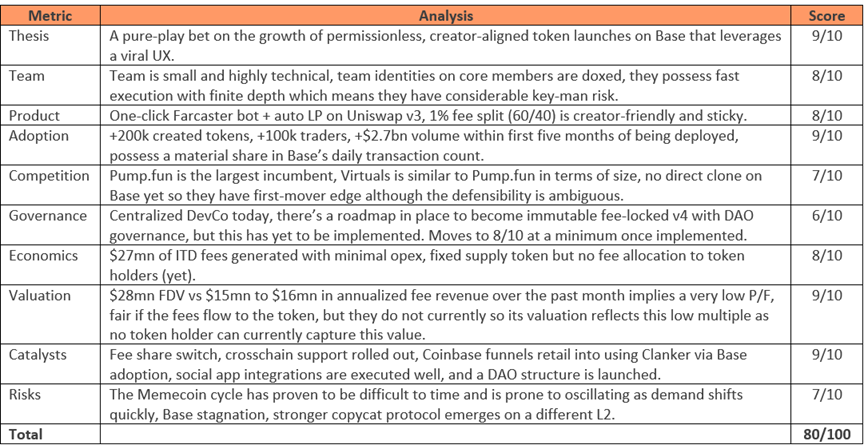

CLANKER: The Ideal Liquid Venture Bet to Base Ecosystem Growth

Investment Overview

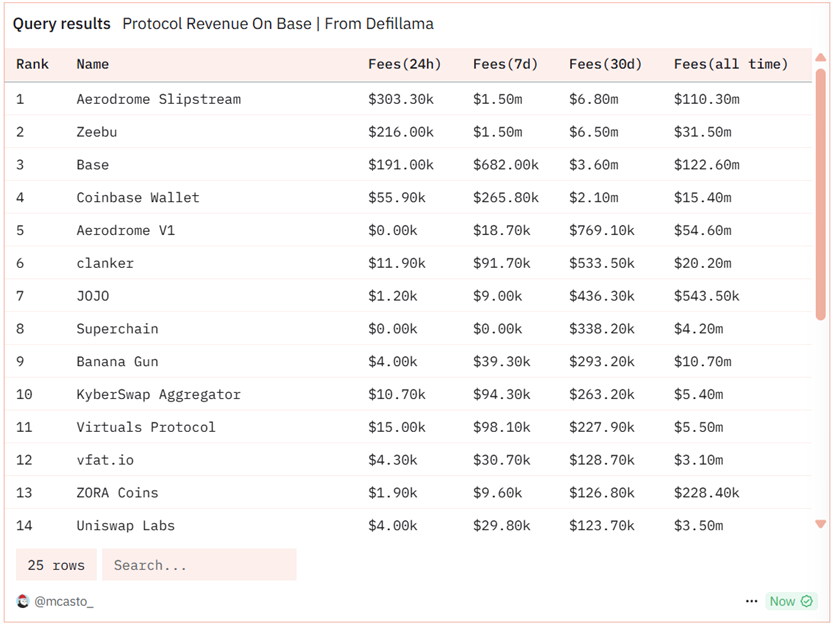

Clanker, at its core, is a Farcaster-native token deployer. Users have the ability to prompt Clanker to deploy an ERC-20 token to Base, through tagging the agent on Farcaster along with the desired token name, symbol, and thumbnail. When Clanker deploys a token, it initiates a single-sided 1% fee pool on Uniswap v3. Currently, 40% of fees go to interfaces, 40% goes to the creator, and 20% is allocated to Clanker. According to their team, Clanker has been profitable since day one, operating with a low headcount and operating expenses. To date, Clanker has generated about $27mn in fees, and since launching in Q4 of last year, the platform has averaged $4.5mn in monthly fees, establishing it as one of the higher fee-generating projects within the Base ecosystem. Within the protocol’s launched tokens, we have seen over $2.7bn in DEX volume. Not only is Clanker an application bet, but it also has the potential to become an infrastructure bet on Base ecosystem growth. However, this is contingent on value flowing back from Clanker-launched tokens to token holders. The CLNKR100K index, excluding CLANKER, is currently valued at about $78mn. At an FDV of $30mn, the discount at which CLANKER trades at relative to its ecosystem presents the attractive opportunity to purchase an infrastructure asset that is fundamentally mispriced versus its ecosystem. However, this discount is understandable given there is no revenue capture for token holders yet.

Clanker's role is beginning to move towards backend infrastructure for a new promising cohort of projects launched by the agent on Base. Some of these projects are closely partnering with Clanker, or act as an extension. While others are simply deploying tokens via Clanker and aligning themselves within the ecosystem of Clanker-launched projects. One recent notable update to Clanker is that interfaces now receive 40% of fees. If someone launches a Clanker token via Clank.fun, Bnkr Bot, or Tiny Labs, the partnered interface receives 40% of fees, while the creator earns 40% and Clanker earns 20%. If a user launches a token directly through Clanker by tagging it on Warpcast, Clanker receives 60% of fees. Clanker v4 should launch soon, which will likely include a retooling of the launch mechanism for compatibility with Uniswap v4. Other applications can leverage Clanker’s smart contracts to issue tokens, such as Native and Tab. This has prompted the team to expand broadly so developers can build on top of Clanker and deploy tokens through its architecture. In the future, there are plans to make the protocol completely permissionless with immutable fees that benefit creators and users.

Token Metrics and Score

Trial by Fire: Addressing the Recent Team Departure

It has recently come to light that a core team member of Clanker, going by the name “Alex”, was previously the pseudonymous person Gabagool.eth. For those who are unfamiliar, Gabagool was a core team member of Velodrome in 2022, a next gen AMM combining aspects of Curve, Convex, and Uniswap, to service liquidity constraints for the Superchain ecosystem. It came to light that an exploit Velodrome suffered that year was in reality Gabagool funneling approximately $350k in company assets into a wallet under his control. He admitted to the theft after overwhelming evidence pointed to his theft, and he was removed from the Velodrome team. His physical footprint would go unnoticed until he was identified at a public event promoting Clanker at Farcon recently. Once identified as the person who stole funds from Velodrome, the Clanker team removed him from the team and ensured there were no assets at risk of control by “Alex.” This event has led to what I believe to be highly asymmetric upside as Clanker currently trades at a $28mn FDV. Additionally, there has been observable flow over the past two weeks from Coinbase to several unfunded Base EOAs, totaling $450k to $550k each in three wallets. The flow, timing, and size of the transfers will likely lead to fund accumulation if they are funded with ETH in wallets that contain paper trails leading to entity identifications. A link to each wallet’s CLANKER positions can be found below:

Valuation and Fundamentals

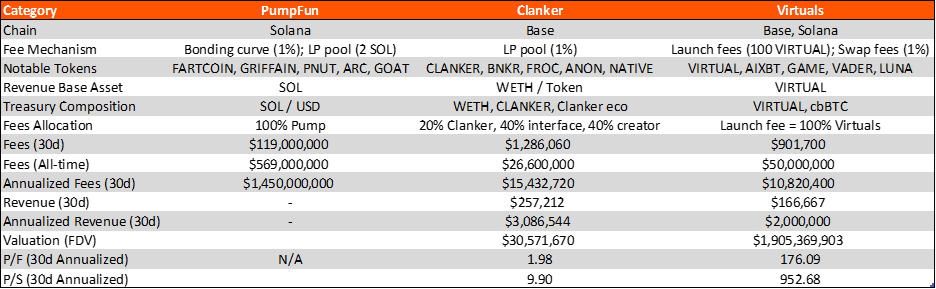

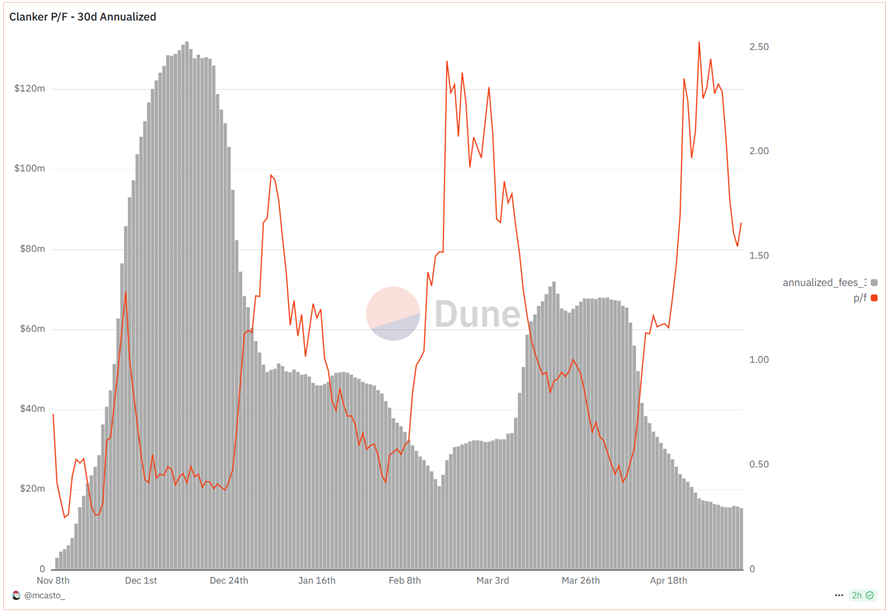

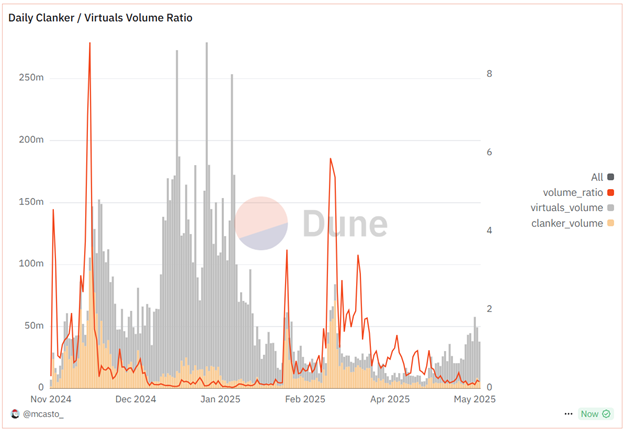

Pump.fun, Virtuals, and Clanker all contain methods to deploy tokens that cater to users wanting to gamble or speculate on highly volatile assets. Currently, Pump dominates the market and demonstrates the true size of the token launcher TAM. Virtuals offers insight into Base's progress versus Solana and are well-positioned to be beneficiaries, should this speculative behavior return to either chain with market demand for launching agents. Back in December, Virtuals and Clanker combined for $18.1mn in fees ($13mn/$5.1mn), roughly equating to a fifth of Pump.fun's $81.5mn total. Clanker stacks up well relative to entrenched incumbents Pump.fun and Virtuals, even with Clanker's post speculative usage decrease, its revenue multiples remain strong. From a revenue multiple perspective, Clanker is attractive as it currently trades at 1.98x P/F using annualized 30d fees. This is significantly lower than Virtuals' P/F of 176x while Clanker's fees are outpacing Virtuals over the past month. At current valuations, Virtuals is 61x higher than Clanker. Possible rationale for the valuation mismatch is provided below:

- ◆The recent announcement that “Alex” has been removed from the team.

- ◆The Clanker ecosystem is still in its infancy stages and is not as closely linked to the AI narrative as VIRTUALS is.

- ◆There is an existing risk premium with regards to their treasury composition of WETH/CLANKER/Clanker ecosystem assets.

- ◆Existing ambiguity to what the endgame of CLANKER's tokenomics entail, for example the fee allocation has had three different instances.

There’s a tradeoff between Virtuals’ diversified fee accrual mechanisms and Clanker’s higher beta, volume-driven fee generation. To provide additional color on Virtuals vs Clanker, as this is likely the most relevant comp given both have a community on Base (albeit Virtuals has launched an instance on Solana), Virtuals has a notably different token economy than Clanker does. The former implemented a 1% swap tax into their launched tokens, and one of their more recent upgrades now routes 70% of tax directly into the agent creator and 30% to the Agent Commerce Protocol (ACP). Agent wallets also earn per-inference and in-app payments that settle in VIRTUAL and feed an onchain buy-back-and-burn mechanism, adding a utility “boost” beyond swap volume. Clanker, by contrast, monetizes through a 1 % Uniswap V3 pool fee applied only in the liquidity pool it deploys. The model’s simplicity has generated lifetime fees of $27mn with current daily fees near $30k, about $20k less Virtuals’ daily fee run-rate. Virtuals thrives on large scale AI-agent launches. When a token is launched that hits a large valuation (e.g. AIXBT),platform activity inherently increases as speculators move to capture upside from other launches. Clanker’s platform is more aligned with everyday token creation, from casual community coins to themed memes, and shares fees generously with creators. Virtuals remains a more single-purpose launcher that is excellent for AI-agent launches, but less flexible for everyday token needs. On the other hand, Clanker has grown an ecosystem of interfaces (Clank.fun, Bankr trading bot, TinyAgents), lowering friction for non-Farcaster users and smoothing out adoption. This network of partner UIs both diversifies its volume sources and makes usage stickier.

Catalysts to Drive Upside:

Potential Transition to DAO Governance Structure : While this catalyst serves to be an inference on what may be implemented, one of the more impactful developments that could catalyze price discovery would be the introduction of a governance structure that includes token holder voting rights and fee sharing. As of now, there is no direct claim on fees, as they are allocated to creators, interfaces, and the treasury. This fee-share could take several forms, namely in the form of buybacks that would be allocated to holders who stake their existing position. v4 of the protocol has been teased by the Clanker team on social media over the past week. While the entirety of this implementation has yet to be revealed, it will be worth noting if this is the protocol change which passes a portion of value to holders, should they opt in to receive utility. As the valuation of CLANKER trades at a low P/F relative to the market, this utility upgrade should in theory be viewed as highly positive. To summarize, evolving Clanker into a governance structure with fee sharing unlocked for token holders would address the value capture gap and unlock a possibly higher valuation for the token. CLANKER currently trades at a discount relative to the $CLNKR100K index, and this discount likely compresses with utility passing through to holders. Additional utility may appear if there’s a future update where more activity on the platform is locked behind a requirement to hold CLANKER to access.

Coinbase Alignment and Integration into the Coinbase Stack: The rise of the Clanker ecosystem has been closely in tandem with the Base ecosystem, including Farcaster. Stepping back briefly, let’s take a look into why I believe what the Base team is building on the consumer side on their L2 should be net beneficial for Clanker’s growth drivers. Cheap transaction fees and CEX synergies have propelled Base to become one of premier EVM-adjacent challengers to Solana. Base has shown strong momentum over the past year, occasionally attracting capital rotations into the Base ecosystem and its tokens. However, these rotations have historically proven to be short-lived and Solana still reigns as the leading chain for consumer-focused applications and retail usage. The L2's most substantive dialogue and strong developer talent likely exists on Farcaster, which has become incrementally more secluded from Twitter-derived crypto content. The identities between Farcaster and Base have become further intertwined, resulting in a degen meets consumer community. After spending time researching the Clanker ecosystem, I strongly believe it's worth considering if it may have the strongest pathway to becoming the Base proxy for token launches going forward. With this stage set, it appears there is an opening for a capital rotation to Base if Coinbase continues to generate positive public perception. This past February was an eventful one for Base and Coinbase with signs displaying increased alignment within Base and Clanker ecosystem. Let’s take a look at a few examples:

- ◆February 4: Coinbase Wallet announced they are integrating a Farcaster feed into the Coinbase Wallet.

- ◆February 14: Coinbase Wallet demonstrated their token metadata MVP by launching Based Froc via Clanker.

- ◆February 19: It was announced that CLANKER will be listed on Coinbase as it was added to the listing roadmap. The same day, Brian Armstrong tweeted out a long post that received criticism shortly after posting. What these responses likely miss if that it came hours after it was announced that CLANKER was added to the listing roadmap and that the post is likely more about foreshadowing changes in Coinbase's operational structure and listing framework instead of an endorsement of the current state of memecoins. Since then, CLANKER was listed as an asset available to be traded on Coinbase.

- ◆February 19: There has a strong history of Coinbase/Base alluding to a partnership with Clanker, as evidenced from Base highlighting on its X account the use case of Clanker to utilize AI to deploy tokens on Base.

Upcoming v4 Launch: Their next version, v4, is on the horizon and is anticipated to include new listing changes and an AMM architecture adds an instance that will be a hook implementation for Uniswap v4. The Clanker team has indicated that their new version will retool the launch mechanism for deploying new tokens, and one concrete possibility is that they will implement custom pool logic to address the limitations of the current 1% pool fee model. Using Uniswap v3 for new token pools, Clanker defaulted pool creations to the 1% fee tier, which maximized fee revenue initially, but has drawbacks. As tokens mature and volatility dampens, liquidity often migrates to lower-fee pools for better trader pricing. To counter this, Clanker v4 may introduce variable fee tiers or adaptive fees using Uniswap v4 hooks. The team has been thinking about a variable fee model where fees adjust based on volatility and token age. This would future-proof Clanker’s token model, ensuring their pools remain the dominant venue for trading. Another potential change in Clanker v4 is taking a separate protocol fee on swaps (e.g. 2% per swap in addition to a lower LP fee), which would be paid in ETH and routed to the protocol treasury. While it may increase total trading costs, it simplifies value capture: Clanker’s protocol fee in ETH could be directly used for the aforementioned buyback/burn without dealing with countless illiquid and high volatility memecoins in the treasury. If executed well, Clanker v4 stands as a catalyst on multiple fronts: it signals a potential boost to fee income, and demonstrates a commitment to decentralization (immutable fee logic and governance as noted). Overall, market participants should be on the lookout for the rollout of Clanker v4 , its feature set with fee changes, governance, etc. will likely determine how quickly the token has the ability to transition toward a value-accrual model.

Key Risks to Consider:

Farcaster reliance: This probably the largest risk for Clanker and its ecosystem, Farcaster is currently secluded from Twitter and the Clanker ecosystem to varying extents is beholden to the emergence of a prolonged Base/Farcaster narrative for attention and capital flows. There are some tailwinds that exist for Farcaster in the near future, including a revamped Frames v2 and an ideal landing place for the AI agent meta with an underlying social graph. Potential issue alleviant here is that Clanker is actively expanded beyond Farcaster as backend infrastructure from ecosystem projects. This has been observed with Bankr and Streamm integrating with Twitter, while Clanker.fun and TinyLabs offer traditional web applications.

Execution risk: Is there too much execution risk with the quantity of ecosystem projects that have launched through Clanker with too few community members to move Clanker from 0-1 in a reasonable amount of time? Said differently, does Clanker have a cold-start problem that takes a heavier lift than what their current community has the bandwidth and capacity to engage?

Value accrual ambiguity: There is now a multitude of tokens that have been launched via Clanker, and there isn't a strong sense of having clarity around their utility and value accrual. The token structure of Virtuals played in key role in the asset running up to be prices at $4bn at its high point.

Volume competition on maturing tokens: Clanker launches are effectively one-dimensional in the way they launch and deploy liquidity, as they are deployed into a 1% fee tier pool on Uniswap v3. The issue here is that historically, the 1% fee tier pools do not attract long term volume, as higher market cap tokens attract sharper LPs in lower fee tiers. This isn't currently an issue as CLANKER and LLM are the only tokens that have meaningful volume outside of the Clanker pool. However, it is being observed that Aerodrome and a 0.3% pool on Uniswap is stealing more than half of CLANKER's volume. With v4 of Uniswap launching recently, and the inevitable maturation of tokens, Clanker will likely need to make adjustments to future-proof its token launching model. This issue has been addressed by the team and is on their radar to solve in a sustainable and value-accretive manner.

Conclusion

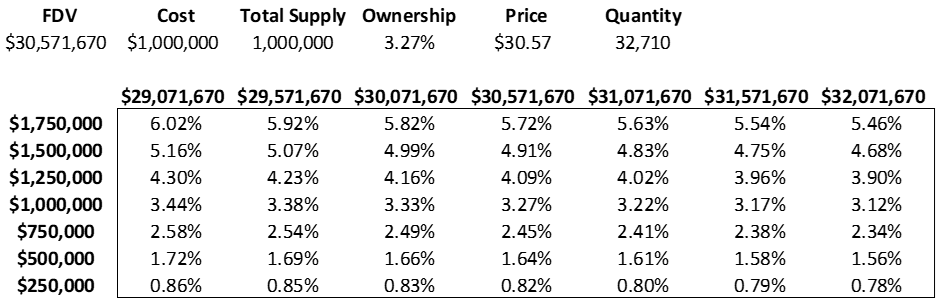

The valuation market participants are paying for currently reflect growth prospects that have yet to materialize to value that token holders receive. There is no concrete publicly known plan to implement a fee switch, but at a $30mn FDV, the growth story can be easily underwritten to venture upside. The capital needed to acquire significant ownership is quite low, At a $1mn investment, total ownership in the network is 3.27%, as evidenced by the below matrix. With every $250k change, your ownership increases by 25%. While annualized fees and deployment metrics have been on a downtrend, the current price reflects these onchain KPIs, and the market is flashing a sign here that there is potential upside for those willing to deploy at what is historically a low valuation. The removal of the toxic team member has opened up the pathway for the remainder of the team to double down and focus on shipping a product that will solidify itself as a proxy bet for Base activity going forward. The platform demonstrates strong growth fundamentals and a material contribution to Base’s onchain activity. However, CLANKER today trades at a discount to its ecosystem projects, likely due to no fees flowing to token holders or used drive exogenous demand. This presents a potentiallyasymmetric upside opportunity, the downside of no value capture is arguably priced in, while the upside of future value capture is yet to be factored. If at any point the token begins to generate revenue through a fee switch or buyback, there is justification for a higher valuation. In effect, the market today can pay a low multiple for Clanker’s fee generating ability, with a call option on multiple catalysts playing out over the upcoming 6-12 months.

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.