Boxed trade: Short $GLXY at 35-40 / share as Helios Upside priced in amidst crypto cycle top. Long $GLXY / short shitcoins or Long $GLXY at $15-18 / share to get >'26 Helios optionality for free

TL;DR

- ◆Set‑up: GLXY is a messy SOTP with two levers: (1) Crypto + IB (volatile, cost‑drag, cyclic) and (2) Helios (AI DC) (scarce power, long‑duration cash flows, execution + financing risk).

- ◆If one wants to be bullish, the base case SOTP (today): ~$39.6/sh effectively bakes in all the upside: Prop book $6.4, IB $10.0, corp drag –$7.5, Helios PV (25× EV/EBITDA, PV’d, equity‑netted) $22.7 → $31.6 total (detail below). (All per‑share math rerun on ~400mm diluted shares.)

- ◆Short‑term short / long‑term long:

- ◆Short zone:$35–$40 (market paying full multiple for 2028 YE Helios; very rich vs a pre‑cash‑flow asset; crypto beta downside can hit IB + prop book simultaneously).

- ◆Long zone:$15–$18 (you’re effectively paying little for Helios beyond 2026: at $15–18 the implied Helios PV is ~$5-6 / share, basically 25x EBITDA on 2026 #’s at 200 MW which is increasingly derisked; the stack looks like $6–7 for prop, $10 for IB, –$5.6 corp drag.

- ◆Key risk to short: incremental permits/tenant/financing or spin signal that quickly re‑rates Helios; Trump‑era policy + cycle strength could also spike IB fees.

- ◆Key risk to long:crypto drawdown (–30%/+ cyclic) compresses IB + prop book while Helios remains pre‑cash‑flow; financing/permits slip; CoreWeave counterparty.

- ◆Recent proof points: $1.4B ring‑fenced Helios Phase‑1 project finance at ~80% LTC; CoreWeave expanded commitments; AllUnity EUR stablecoin green‑lit; Q2 numbers show Global Markets momentum (sources at end). (Galaxy, PR Newswire, investor.galaxy.com, Reuters)

Recent developments (what changed)

- ◆$1.4B Phase‑1 project finance (secured, ring‑fenced): 80% loan‑to‑cost, ~36‑month term; collateral is Helios Phase‑1 assets (minimizes recourse to corporate). Galaxy contributed ~$350m equity for Phase‑1; debt covers the rest. This isolates project execution risk and lowers the probability you get diluted at HoldCo to fund capex. (PR Newswire, Galaxy)

- ◆CoreWeave expansion: Additional Helios capacity options exercised; long‑term lease structure (15‑yr) with cost pass‑through supports very high EBITDA margins (Galaxy cites ~90%). Structure looks closer to NNN‑style with indexed pricing, reducing operating volatility but increasing tenant concentration exposure. (investor.galaxy.com, The Block)

- ◆Digital Assets momentum: Q2’25 adjusted gross profit up QoQ; mgmt indicated July was strongest month to‑date; loan book growing. Mix shift toward recurring AUM/staking + OTC flow keeps optionality alive even if prop trading cools. (PR Newswire)

- ◆AllUnity (EUR stablecoin): BaFin approval and launch of EURAU with DWS and Flow Traders—strategic optionality for custody, staking, tokenization, and euro rails that can cross‑sell back into Galaxy’s stack. (Reuters, Galaxy)

- ◆AI/DC comps: DLR ~18–19× EV/EBITDA; EQIX ~23×; prior DC M&A (QTS) implied mid‑20s multiples. Helios at high‑teens to mid‑20s EV/EBITDA is not unprecedented, but greenfield + single‑tenant risk should still command a PV haircut until cash flows land. (Value Investing, QTS Data Centers)

Long thesis (3–5 bullets that matter)

- ◆Scarce power + large contiguous site → structural alpha: Helios controls 800 MW permitted and 2.7 GW under study in ERCOT; permitting + transmission lead‑times are multi‑year while hyperscaler capex is exploding (black book: $300B+ in 2025, multi‑trillion over 5 yrs). Scale + speed to power = pricing power. The interconnect and substation timelines are the real moat: if you have megawatts ready to energize in 2026–27 while others are still in queue, you win take‑or‑pay leases. (Galaxy, Blackstone, cdn.hl.com)

- ◆Unit economics are elite for “DC 2.0”: Contracted revenue (guide ~$1.1B/yr) with ~90% EBITDA (tenant pays most opex/capex) on 15‑yr terms; cash conversion outclasses legacy colocation (DLR/EQIX) with thousands of small tenants and higher sustaining capex. These are NNN‑ish, high‑visibility cash flows once online, with escalators and change‑order pass‑throughs that preserve margins. (Galaxy)

- ◆Corporate optionality (AllUnity / custody / market structure): If policy stays friendly, IB + AM + staking scale with treasuries, ETFs, listings, and tokenization; Galaxy’s full‑stack platform is unusually well positioned to monetize the “pipes” (fiat on/off ramps, OTC, derivatives, custody). EURAU gives a regulatory beachhead in the EU to onboard treasurers. (PR Newswire, Galaxy)

- ◆Potential 2026 spin: A Helios carve‑out once Phase‑1 is live could collapse the conglomerate discount and surface the DC multiple directly, while letting HoldCo rationalize cost and re‑rate on “pure‑play” narratives. Management has hinted they’ll consider structure if the market refuses to pay for Helios in SOTP. Inference aligned with mgmt commentary + spin chatter.

- ◆Balance sheet alignment: Novo is a majority owner; 2022–23 buybacks demonstrated willingness to lean in cyclically (behavioral positive). Expect opportunistic capital markets (minority sale/JV at project level) before tapping HoldCo if crypto is soft.

Short thesis (why it can work tactically)

- ◆Crypto beta underperformance + cost drag: Since 2018, Galaxy’s prop book/IB did not keep up with BTC; IB requires ~$500m of BV to run and might make ~$100m EBIT mid‑cycle—a decent Moelis‑style valuation in bulls (high P/B / high P/E), but it evaporates in bears (fees halve, inventory losses, comp stickiness). The operating‑leverage math is brutal on the way down, and the Street will toggle from 6–8× P/B to 1–3× quickly if prints soften. (Macrotrends, CompaniesMarketCap)

- ◆Timeline mismatch:AI story (2–3 yrs) must bridge a potential 2025 crypto cycle top (historically 12–18 months post‑halving), a window where IB + prop book can get hit while Helios is still capex‑heavy and pre‑FCF. This creates a clean gap where multiple can compress even with good execution. (members.delphidigital.io, insights.glassnode.com)

- ◆Execution/financing risks not fully priced: Permits, construction, interconnects, supply chain, and tenant concentration (CoreWeave). Any slippage pushes PVs down; if power gear/transformers slip, you lose a quarter and re‑rate from low‑20s to high‑teens EV/EBITDA on PV math. (The Block)

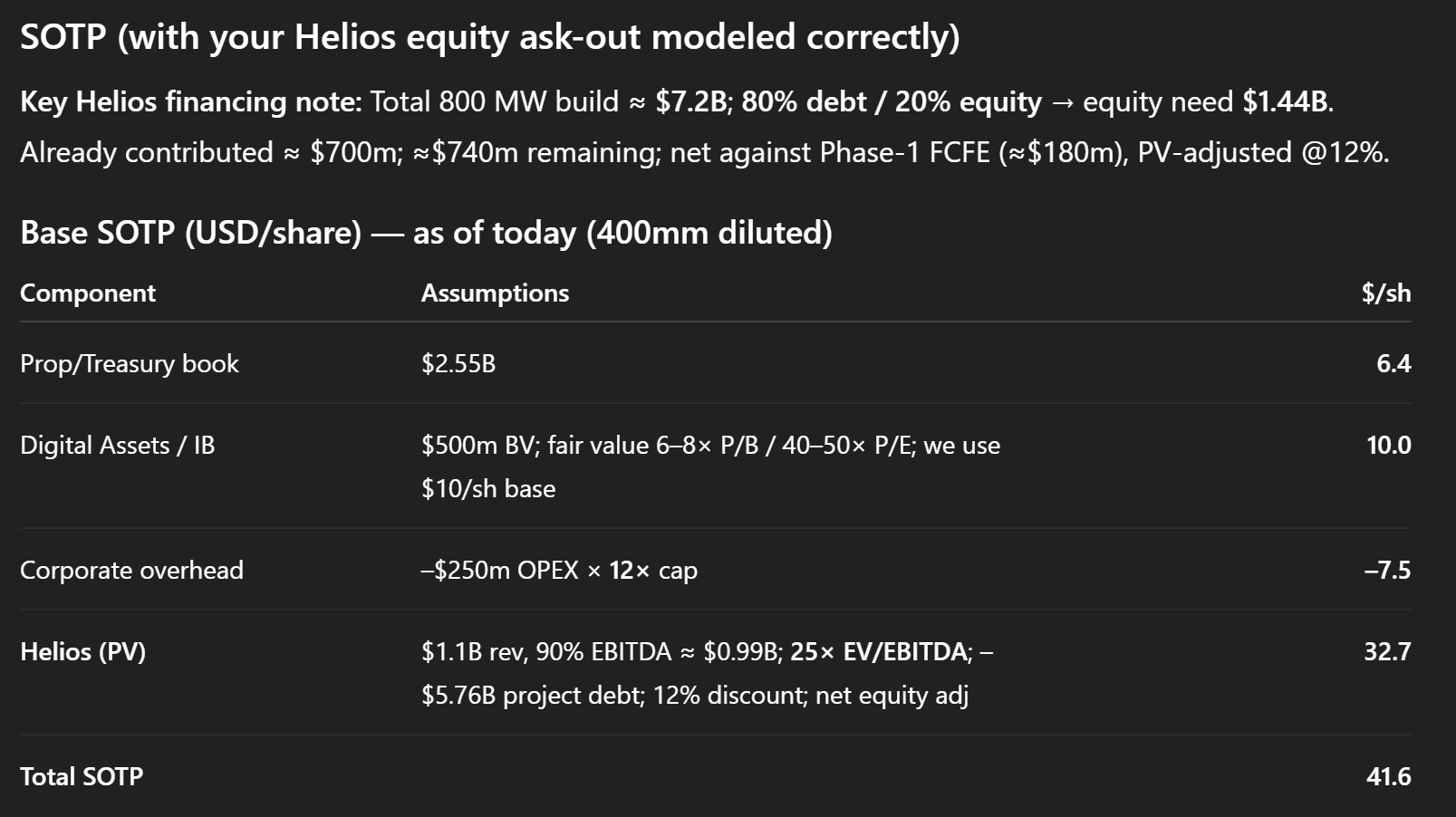

SOTP (with your Helios equity ask‑out modeled correctly)

Key Helios financing note (per your instruction): Total 800 MW build ≈ $7.2B; 80% debt / 20% equity → equity need $1.44B.

- ◆Already contributed:~$700m equity in the “box”.

- ◆Remaining equity to fund:~$740m; net this against Phase‑1 FCFE before principal (est. ~$90m/yr from 2026–27, ~$180m total). PV the net at 12% → subtract ~$0.48B from Helios equity value today.

- ◆

Base SOTP (USD/share) — as of today (400mm diluted)

The Helios line explicitly nets PV(remaining equity ≈ $0.64B) against PV(interim FCFE ≈ $0.16B) before discounting final equity—i.e., your extra ~$800m equity ask is in.

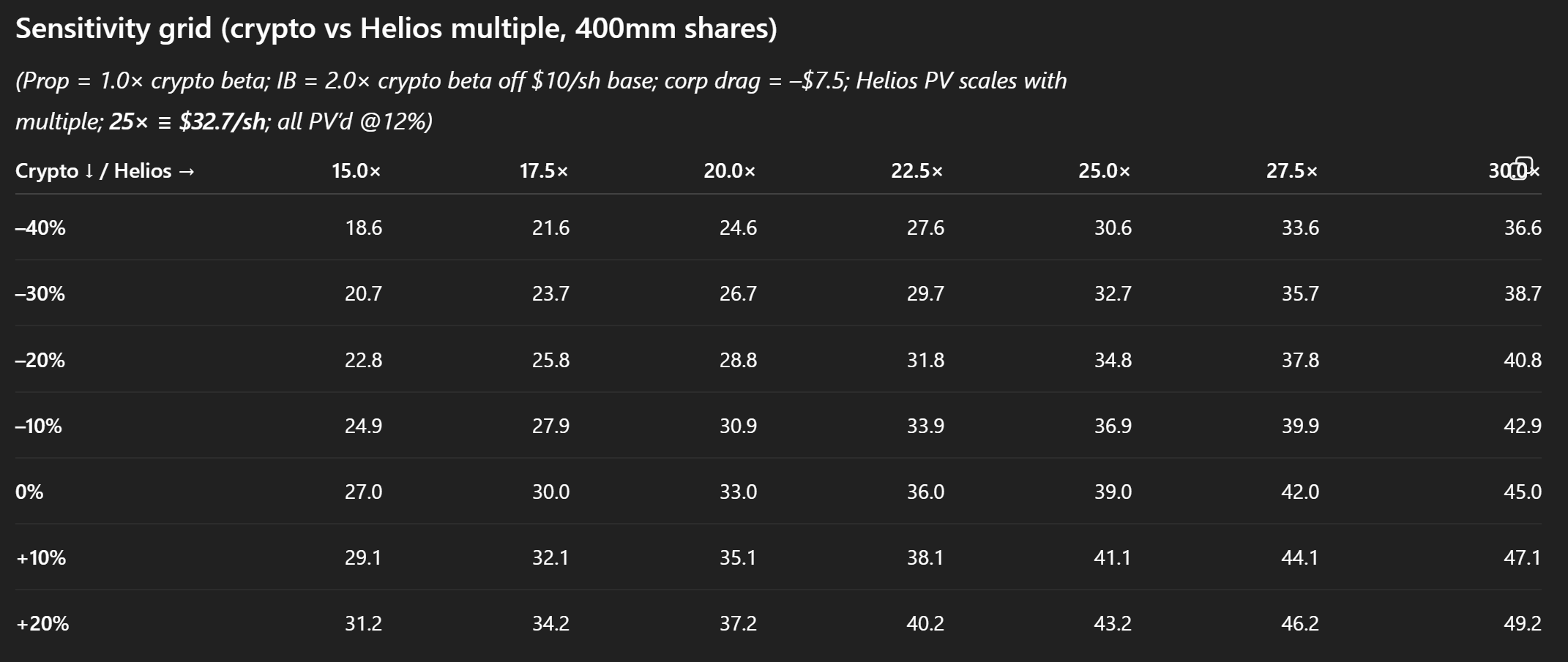

Scenario table (per share; 400mm shares)

Sensitivity (your requested grid): Crypto delta vs Helios EV/EBITDA multiple

In a scenario where the market is willing to give GLXY credit for the full 800 MW (into 2028), here’s the sensitivity table — i.e. in a bull market:

We suspect that the sensitivity table will become the following as the market moves towards a bearish condition — i.e. when it starts projecting the capital market being close and Galaxy not being able to fund the Helios build out, as it only bakes in the 200 MW into YE26:

Where is it a short vs a long (precision + catalyst risk)

Short the rips: $35–$40

- ◆Implied Helios PV at $35–$40 (holding base ex‑Helios at $10.8/sh): $25–$30/sh → ~20×–25× EV/EBITDA PV.

- ◆Why it works: needs low‑20s multiplesand no missteps; crypto beta drawdown compresses IB + prop book; permit/financing slippage derates to high‑teens EV/EBITDA on PV math.

- ◆Catalyst risks to the short:

- ◆New approvals/second tenant + financing for Phase‑2 (de‑risking path).

- ◆Spin signal (S‑1 filing, JV, minority sale) that isolates Helios at a DC multiple.

- ◆Policy impulse (market structure bill, Treasury adoption) that spikes IB fees. (Galaxy, PR Newswire)

- ◆Risk control: hard stop if tape begins to pay ~30× for Helios PV (≈ >$42/sh given current inputs), or if CoreWeave/another hyperscaler inks >+200 MW incremental on similar economics.

- ◆

Buy panic: $15–$18

- ◆What you’re paying: at $16, implied Helios PV ≈ $5/sh ≈ ~4.0× EV/EBITDA on FY28 full-buildout, or basically only the 200 MW EBITDA by year-end 2026 that’s rapidly derisking. You are basically getting Helios for free.

- ◆Why it works: protects downside via asset scarcity + take‑out appeal, while providing convexity to approvals + Phase‑1 revenue in Q1’26.

- ◆Catalyst risks to the long:

- ◆Crypto –30% (history says plausible into a late‑’25 top); IB fees halve, prop book falls, and equity raises get punitive.

- ◆Build delays/overruns or CoreWeave credit stress that force repricing to mid‑teens EV/EBITDA. (members.delphidigital.io, The Block)

Key debate points (what really drives the outcome)

- ◆Helios multiple:High‑teens through mid‑20s is the credible band vs DLR/EQIX today (18–23×); low‑20s fair until Phase‑1 cash flows and a second tenant are visible. (Value Investing)

- ◆Funding path: Remaining ~$740m equity need is manageable if Phase‑1 FCFE (~$90m/yr) starts in ’26, plus options (project‑level refi, minority sale, JV). But liquidity window matters if crypto sells off. (PR Newswire)

- ◆IB valuation toggle: In bulls, Moelis‑like (6–8× P/B; 40–50× P/E) is arguable; in bears, fees halve and the “digital asset one‑stop shop” narrative fades—this is the swing factor on SOTP tails. (Macrotrends, CompaniesMarketCap)

- ◆Tenant concentration & residual value: 15‑yr bespoke build lowers residual certainty; renewal/retrofit economics are unknown—hence conservatism on terminal multiples vs legacy colo (thousands of tenants).

- ◆2026 spin: Cleans up the story; if not pursued post Phase‑1 ramp, a persistent conglomerate discount is likely.

“What’s the trade?”

- ◆Base case: wait for extremes. Short $35–$40 with defined stop on de‑risking headlines; accumulate $15–$18 with patience for 2026 cash‑flow proofs.

- ◆Pairs (optional):

- ◆Short GLXY vs long DLR/EQIX on AI/DC multiple mean‑reversion if Helios hype runs ahead of permits. (Value Investing)

- ◆Long GLXY vs short high‑beta miners if you want AI/DC convexity but less halving‑cycle bleed.

- ◆Long GLXY vs. short altcoins, where altcoins would get creamed in the drawdown roughly having the same vol with the cost-load of GLXY

- ◆Catalyst map:

- ◆Tactical bear: BTC chop/air‑pocket into late‑’25 + soft IB prints → revisit mid‑teens. (members.delphidigital.io)

- ◆Tactical bull: Phase‑1 EPC milestones, interconnect dates, 2nd tenant signing, or spin news → re‑rate Helios to mid‑20s multiple.

Source notes & links (primary > sell‑side; plus best research reads)

Primary / company

- ◆$1.4B Helios project finance (ring‑fenced, 80% LTC): Galaxy newsroom & PR. (Galaxy, PR Newswire)

- ◆CoreWeave lease expansions: Galaxy IR updates on additional MW. (investor.galaxy.com)

- ◆Q2’25 results (segment detail): PR. (PR Newswire)

- ◆AllUnity (EURAU) launch + BaFin approval: Galaxy post; Reuters. (Galaxy, Reuters)

- ◆Follow‑ups: The Block coverage of financing terms. (The Block)

Comparables / industry

- ◆DLR EV/EBITDA (18–19×); EQIX (≈23×). (Value Investing)

- ◆QTS take‑private (Blackstone) context for DC multiples. (QTS Data Centers)

- ◆Digital infra demand & capex trajectory (Blackstone pattern recognition; Houlihan Lokey DI update). (Blackstone, cdn.hl.com)

Sell‑side / market color

- ◆Goldman Sachs initiation on GLXY (Neutral, ~$30 PT): coverage note summaries. (MarketBeat)

- ◆Morgan Stanley DC/thematics (AI spend, data‑center demand), and broader outlooks. (Morgan Stanley)

Cycle framing (Delphi / Glassnode)

- ◆BTC cycle timing (12–18 months post‑halving)—frameworks used for the short‑term short thesis. (members.delphidigital.io, insights.glassnode.com)

- ◆

Voices you should read/follow

- ◆Rittenhouse Research (coverage + on-the-ground Helios tracking).

X (formerly Twitter), CoinDesk - ◆Flood Capital (Duncan) interviews & threads.

Blockworks, YouTube, X (formerly Twitter) - ◆Blockworks Empire episodes discussing GLXY and Helios.

Blockworks

Notes on modeling choices (so you can audit)

- ◆Shares:400mm diluted for per‑share math.

- ◆IB block: assumes $500m BV supports the desk; $100m EBIT mid‑cycle; fair value 6–8× P/B (=$3.0–$4.0B) and 40–50× P/E on $75m NI; we use $10/sh base and scale IB at 2× crypto delta in scenarios. (Macrotrends, CompaniesMarketCap)

- ◆Corporate drag: capitalized at 12× on $250m OPEX → –$7.5/sh on 400mm shares.

- ◆Helios PV:25× ≡ $28.8/sh anchor; 12% discount to 2028 run‑rate; subtract PV(remaining equity) and add PV(Phase‑1 FCFE)before discounting terminal equity—per your request.

Bottom line

- ◆Tactical:Short $35–$40 if the tape pays >~22× Helios PV before Phase‑1 cash is live or Phase‑2 is financed/leased; cover on real permitting or spin signals.

- ◆Strategic:Accumulate $15–$18 if a crypto drawdown forces capitulation; you’re buying scarce DC optionality at ~4–6× EV/EBITDA PV with identifiable 2026 catalysts.

This article is being AI-generated based on the August 19th, 2025 BidCast Episode on $GLXY and may contain mistakes. It does not constitute as investment or any advice and does not represent the view of the BidClub.io platform.

Generated by o5 ofchatgpt.com

BidCast Source: https://www.bidclub.io/posts/cmd8prrbw0001mjcd3a7vn7hh

Affiliate Disclosures

- •The author and/or others the author advises do not currently hold, or plan to initiate, an investment position in target.

- •The author does not hold an affiliated position with the target such as employment, directorship, or consultancy.

- •The author is not being compensated in any form by target in relation to this research.

- •To the best of the author's knowledge, the information provided here contains no material, non-public information. The accuracy of the information is the responsibility of the reader.